Boeing (ticker: BA) entered 2025 as a convicted corporate felon. In July 2024, it pleaded guilty to criminal fraud charges linked to the two fatal 737 MAX crashes that killed 346 people. The fine was $243.6 million, which critics called a slap on the wrist. The stock had shed 32.1% of its value in 2024, closing the year at $177. Nobody expected a standout year from BA. Yet, by December 31, 2025, Boeing had climbed to approximately $217, booking a +22.6% gain on the Dow Jones Industrial Average (DJIA), according to Macrotrends, nearly doubling the DJIA’s own 13% advance, which saw the index close at 48,063.29 from an opening of 42,660.

As Disruption Banking noted in its wrap of Dow Jones 2025 performance, Boeing ranked among the index’s solid gainers, outpacing the broader benchmark by roughly nine percentage points.

Boeing Stock Surge 2025: From $177 to $217 and Outperforming the Dow Jones

Boeing closed 2024 at $177, the bottom of a brutal two-year slide. Going into 2025, sentiment was awful. The company was still navigating the fallout from a machinists’ strike, production chaos, and potential criminal liability. Yet it gained 22.67% against a Dow that itself advanced 13%. Context matters.

The Dow’s gain was driven by a narrow group of mega-caps, AI-infrastructure plays like Caterpillar (+59.5%) and Goldman Sachs (+55.8%). Boeing’s gain was different in character, a recovery trade on an industrial giant with a record backlog and a new CEO trying to stabilise operations.

As Disruption Banking‘s Boeing deep-dive noted, the stock was already sitting near $235 by mid-year, signalling that the market began pricing in a credible turnaround well before year-end confirmed it.

Boeing Revenue Hits $89.5 Billion in 2025: Key Highlights from Q4 Earnings

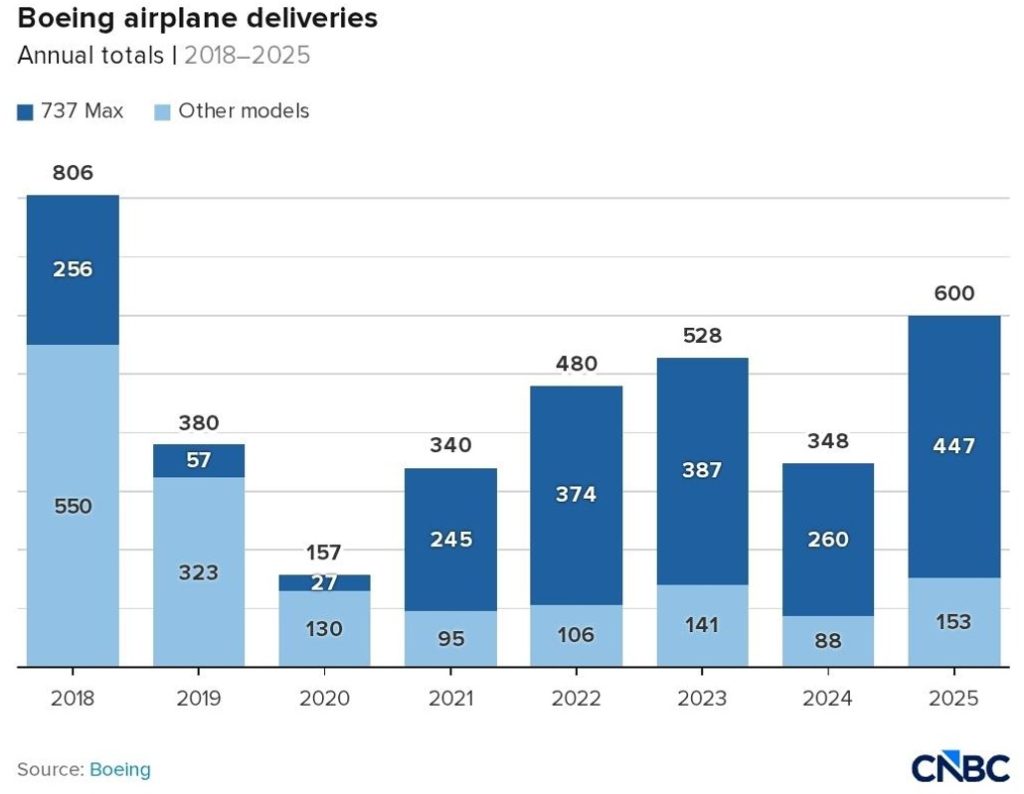

The headline number from Boeing’s January 27, 2026, Q4 earnings release is hard to dismiss. Full-year 2025 revenue hit $89.5 billion, a 34% jump year-over-year and the company’s best top-line result since 2018. Q4 alone delivered $23.9 billion, up 57% versus Q4 2024, beating analyst expectations. Boeing delivered 600 commercial airplanes in 2025, nearly double the 348 planes delivered in 2024 and the highest delivery count since 2018.

Total company backlog reached a record $682 billion, with all three segments (Commercial Airplanes, Defense, and Global Services) hitting record levels. On net orders, Boeing outsold Airbus in 2025: 1,173 commercial net orders versus Airbus’s 889. That’s a meaningful reversal in a rivalry where Boeing had been losing ground.

CEO Kelly Ortberg told CNBC that the company expects positive free cash flow of between $1 billion and $3 billion in 2026, a significant improvement from the negative $1.9 billion registered for full-year 2025. “We’re marching to this $10 billion free cash flow number and it’s going to take us a little bit of time but we’ve got a methodical plan to get there,” Ortberg said.

The 737 programme hit a production rate of 42 per month by Q4 2025, with a target of 47 ahead. The 787 programme, based in Charleston, saw a 30% reduction in average rework hours and is transitioning to eight planes per month.

Boeing 737 MAX Guilty Plea: Lingering Risks from the 2024 Criminal Conviction

The July 2024 guilty plea over the MAX crashes, $243.6 million in criminal fines plus over $1.7 billion in victim compensation, made Boeing a convicted felon in U.S. legal terms. That status could still complicate future U.S. government contracts.

In December 2025, Boeing completed the $4.7 billion acquisition of Spirit AeroSystems (equity value; enterprise value ≈ $8.3 billion including debt) following Federal Trade Commission (FTC) approval, a supply chain move that makes strategic sense but adds near-term integration costs. Management acknowledged Spirit’s impact was a $1 billion negative on 2025 results.

Meanwhile, Boeing’s long-standing environmental obligations for the Lower Duwamish Waterway in Seattle, where the U.S. Environmental Protection Agency (EPA) identified 41 hazardous substances linked to decades of industrial activity, continue to weigh on the company’s legal and reputational balance sheet. On March 4, 2026, the EPA, Department of Justice, and the State of Washington announced a proposed $668 million settlement with over 100 parties, including Boeing, the City of Seattle, and King County (the ”Lower Duwamish Waterway Group”), to fund the long-term cleanup, with work expected to take at least 10 years.

These are not trivial obligations. Yet investors absorbed all of it and still bid the stock higher. That speaks to how much upside the market believes remains in the recovery story.

Boeing Defense Backlog Reaches Record $85 Billion: PAC-3 and Key 2025 Wins

Boeing’s Defense, Space & Security division posted $7.4 billion in Q4 2025 revenue, up 37% versus Q4 2024, and its backlog grew to a record $85 billion, with 26% representing international orders. During Q4, the division secured a contract from the U.S. Air Force for 15 KC-46A Tankers, an order for 96 AH-64E Apache helicopters from the U.S. Army, and delivered the first operational T-7A Red Hawk to the Air Force at Joint Base San Antonio-Randolph.

On the missiles front, Boeing’s earnings call transcript by Motley Fool directly confirmed that the Patriot Advanced Capability-3 (PAC-3) missile seeker program increased output by 33% over the course of 2025, ”enabled by prior investments in capacity and a focus on lean to drive more efficient production.” A multiyear PAC-3 contract is expected in 2026.

In a year where the Commercial Airplanes division was still running a negative 5.6% operating margin in Q4, defence kept the floor from collapsing entirely. Boeing is, in reality, a dual-purpose aerospace and defence company. That duality is exactly what kept investors engaged during the worst of the commercial recovery pain.

Boeing 2026 Outlook: China Mega-Order Talks, Analyst Buy Ratings, and Geopolitical Risks

Boeing’s stock was trading at approximately $214 (TradingView) at the time of writing, close to a 52-week high of $252 hit in January 2026. The catalysts are stacking up fast.

A report from Bloomberg indicates Boeing is in active talks with China for a potential order of 500 737 MAX aircraft. The China opportunity is significant: Boeing’s own 2024 Commercial Market Outlook projects demand for 8,830 new aircraft in China specifically between 2024 and 2043. China’s fleet alone is projected to grow 4.1% annually, from 4,345 to 9,740 planes by 2043.

Jefferies reiterated a Buy rating on Boeing in early March 2026 with a $295 target. Based on 28 analysts tracked by LSEG, the consensus remains Buy, though average targets have moved higher than the earlier $251.91 level (with bullish calls now reaching $300).

The China deal, though, is a two-sided coin. While potentially transformative for Boeing’s order book, trade tensions under the Trump administration are real. China imposed a 34% tariff on all U.S. imports in 2025. If that friction worsens, Boeing risks losing access to a market that underpins a substantial portion of its long-term order thesis. The geopolitical dimension here is not background noise, it is a central risk for BA’s medium-term trajectory.

Boeing 2026 Challenges: Free Cash Flow Goals, FAA Certification, and 777X Timeline

Boeing’s full-year 2025 free cash flow remained negative at $1.9 billion. The 777X widebody’s first delivery remains targeted for 2027. The Dow Jones Industrial Average (DJIA) component still needs FAA approval to push 737 MAX production beyond 42 per month, a requirement the regulator imposed after the January 2024 Alaska Airlines mid-flight panel blowout.

The 737-10 and 737-7 variants entered FAA final certification testing in Q4 2025, but certification timelines at the agency have a habit of slipping. Over 1,500 aircraft in the backlog are waiting on those approvals.

Boeing burned through roughly $40 billion in cash from Q1 2019 through Q3 2025. Management’s long-term target of $10 billion in annual free cash flow is described by CFO Jay Malave as “very attainable”, per Motley Fool’s report. But it requires certification timelines holding, production ramp-up executing, and the BDS division swinging to profit. None of those are guaranteed.

Trefis analysis notes that Boeing has delivered 30%+ gains in under two months on 14 separate occasions historically, indicating explosive upside potential when catalysts align. The question is whether execution in 2026 finally matches the narrative.

Author: Richardson Chinonyerem

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organizations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

Boeing in the Dow Jones: Jets on Wall Street | Disruption Banking

Dow 30 C-Suite: 1 Woman CEO, 5 Female CFOs, and a Glass Ceiling | Disruption Banking