DisruptionBanking recently examined why Old China’s domestic stock-market benchmarks, the CSI 300 and FTSE China A50, the nearest equivalents to the Dow Jones, remain dominated by state-owned banks, energy giants, and insurers. ICBC, PetroChina, Sinopec, and China Construction Bank still anchor the mainland economy and its credit system. But ask a global fund manager what “China” means to their portfolio, and the answer rarely starts with state-linked benchmarks. It starts with Tencent, Alibaba, BYD, and CATL: the companies of “New China.”

The Offshore China Trade: Why Tencent and Alibaba Dominate Global Portfolios Unlike the U.S. Dow Jones

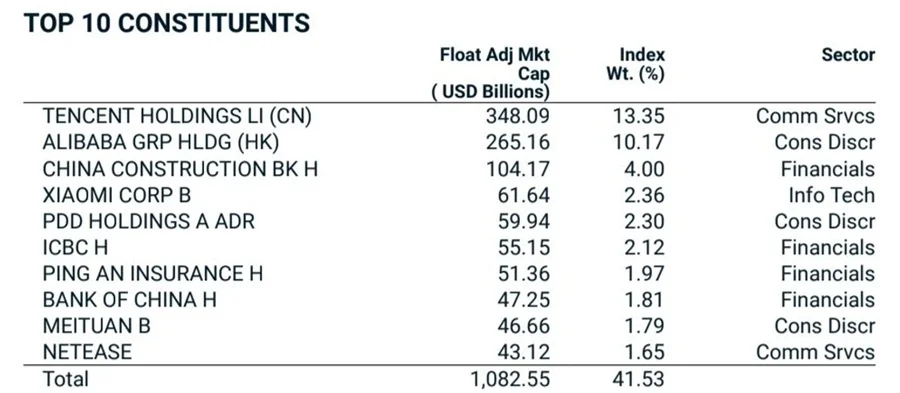

The divide between Old and New China is structural. A-shares trade in Shanghai and Shenzhen in renminbi, while H-shares, red chips, and ADRs trade in Hong Kong and New York. Tencent and Alibaba sit outside the CSI 300 and FTSE China A50, mainland China’s closest equivalents to the U.S. Dow Jones Industrial Average (DJIA). Instead, they dominate the MSCI China Index, which blends onshore and offshore listings.

The MSCI China Index (USD) late-May 2026 factsheet puts Tencent’s weight at roughly 13.4% and Alibaba’s at around 10.2%, which are almost three times the combined weight of ICBC, China Construction Bank (CCB), and Bank of China (BoC). For most offshore investors, New China is not a sliver of the opportunity set; it is the opportunity set.

Tencent’s $500 Billion Grip on New China: WeChat, Gaming, AI, and Ads

WeChat‘s ecosystem of messaging, payments, and mini-programs remains central to the daily lives of hundreds of millions of users.

Tencent’s first-quarter 2026 results showed strength in gaming and AI-driven advertising. The company reported non-IFRS profit attributable to equity holders of RMB 69.8 billion (over $10 billion), up 11% year-on-year, even as it ramps up AI spending across its cloud and agent initiatives. With a market value of over $500 billion, Tencent remains China’s single most important listed company to global portfolios.

Alibaba’s $260 Billion Reinvention: E-Commerce, Cloud, and the AI Pivot

Years of regulatory pressure pushed Alibaba to refocus on e-commerce, cloud, and AI. Chairman Joe Tsai has staked the company’s future on that pivot, telling the VivaTech conference in Paris in June that AI represents a $50 trillion addressable market tied to global productivity: “that’s why we’re all in” on AI.

Morgan Stanley named Alibaba a Top Pick, citing its integrated position across chips, cloud, and foundation models. With a market value near $260 billion, Alibaba trades well below its historic peak but still anchors China’s AI infrastructure story.

China’s EV Power Pair: CATL Controls Batteries, BYD Chases Global Auto Scale

Contemporary Amperex Technology Co., Limited (CATL), a top Chinese battery manufacturer and tech company, controlled 40.7% of the global electric vehicles (EV) battery market in early 2026, more than three times BYD’s 13.7% share in second place. Together the two Chinese firms supply over half the batteries in EVs worldwide.

BYD, the world’s top-selling EV maker by volume in 2025, is chasing a bigger prize. Founder and chairman Wang Chuanfu told shareholders in June that BYD aims to become “the No. 1 automaker globally in terms of scale” within five years, as overseas deliveries push toward 1.5 million vehicles in 2026.

China’s Consumer Internet Still Has Teeth, Even After the Regulatory Crackdown

Beyond Tencent and Alibaba, China’s consumer internet produced Meituan (local services and delivery), PDD Holdings (Pinduoduo’s deep-discount model, with a market cap exceeding $110 billion), Xiaomi (smartphones turned EVs), and NetEase (gaming).

Xiaomi’s pivot illustrates the pattern: the company delivered over 410,000 EVs in 2025 and targets 550,000 in 2026, with CEO Lei Jun telling customers that “safety and transparency matter more than marketing gimmicks.” These platforms built their scale on China’s hyper-competitive, mobile-first consumer base, not state direction like in Old China benchmarks.

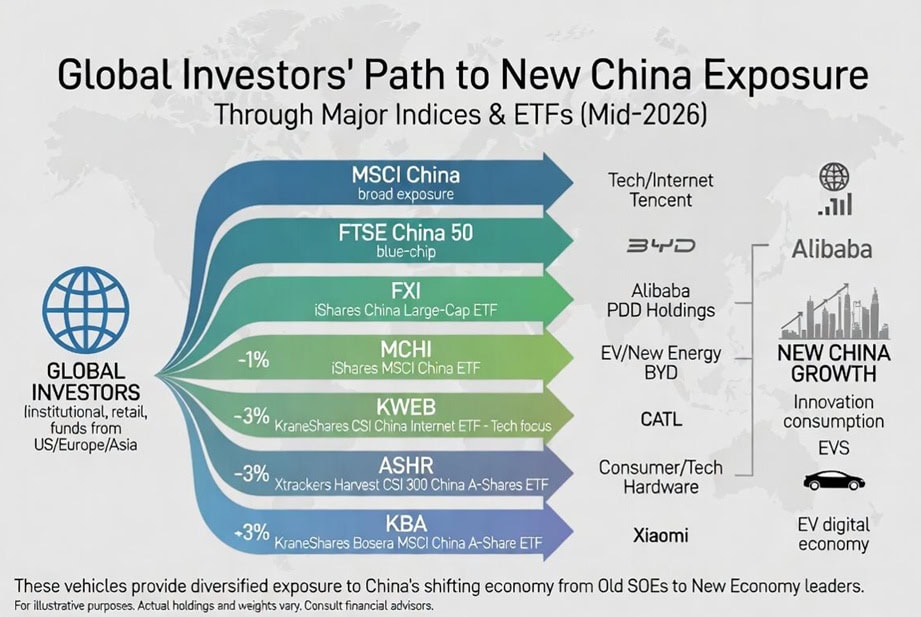

How Investors Actually Buy New China: MCHI, FXI, KWEB, ASHR, and KBA

MCHI (iShares MSCI China) offers the broadest reach, holding 600-plus stocks across the full MSCI China universe. FXI (iShares China Large-Cap) tracks the FTSE China 50, concentrated in Hong Kong-listed H-shares, red chips, and P-chips. KWEB isolates internet platforms through overseas listings only, giving it no exposure to state-owned enterprises. ASHR and KBA run the other way, tracking mainland A-shares via the CSI 300 and the MSCI China A 50 Connect Index, the route into Old China names like Kweichow Moutai.

As Allianz Global Investors notes, “many internet giants – such as Alibaba and Tencent – are only listed in offshore markets,” which is why fund choice, not just country choice, decides which China an investor actually owns.

Is New China Becoming More Important Than Old China?

Not by every measure. UBS estimates that innovation-driven “new economy” sectors made up only 15–20% of GDP and 10–15% of investment in 2024, though they contributed roughly a quarter of growth between 2020 and 2024. The IMF, projecting 2026 growth near 4.5%, said China’s economy “has proved resilient in the face of multiple shocks” in recent years while urging a shift toward consumption-led growth.

As Morgan Stanley put it in its 2026 outlook, “the market is not the economy and the economy is not the market.” Old China still employs more people, lends more capital, and pays larger dividends. New China commands the valuation premium, the growth narrative, and increasingly, the world’s attention.

Author: Richardson Chinonyerem

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organisations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.