Invesco’s newest digital-asset move is not a speculative token or an exchange play. The $2.45 trillion asset manager has filed to launch a money market fund built to sit behind dollar-pegged stablecoins, the cash-like reserves that keep those tokens worth a dollar. That puts Invesco into a contest Wall Street already knows how to win: managing short-duration Treasury cash, now wrapped in blockchain rails.

Inside Invesco’s Filing: A $1 NAV Money Market Fund Built for Stablecoin Reserves

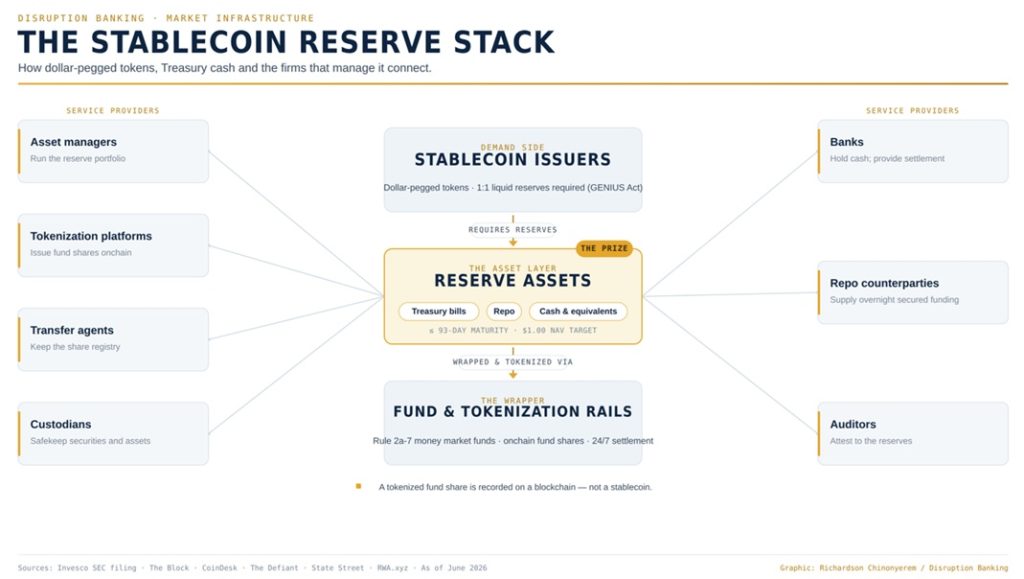

On June 24, 2026, Invesco submitted a post-effective amendment to the U.S. Securities and Exchange Commission (SEC) to add the Invesco Stablecoin Reserves Onchain Fund to its Short-Term Investments Trust, a long-standing Delaware money market structure. The fund would invest in cash, short-term U.S. Treasuries, and repurchase agreements (short-term secured loans backed by Treasuries) while holding a steady $1.00 net asset value. It is built as a Rule 2a-7 government money market fund, with a conservative 93-day maturity limit to align directly with GENIUS Act eligible reserve assets.

The shares themselves would be tokenized. Superstate Services LLC, the transfer agent founded by Compound creator Robert Leshner, would act as sub-transfer agent and run a blockchain-integrated registry, with onchain tokens standing in for fund ownership. The arrangement extends a March 2026 deal in which Invesco took over Superstate’s tokenized Treasury fund, USTB. Leshner described that earlier partnership as “the blueprint for how funds and ETFs will come onchain.” The current filing is marked “subject to completion”: no ticker, no named blockchain, and effectiveness only around late August if the SEC does not step in. This is a proposal, not a live product.

The $300 Billion Prize: Why Stablecoin Reserves Are Becoming Wall Street’s New Cash Pool

Fiat-backed stablecoins need safe, liquid assets behind every coin. As issuance grows, so does the pool of Treasuries and cash that has to be managed somewhere. Stablecoin supply stands near $300 billion to $315 billion today, and Citigroup projects it could reach $4 trillion by 2030. Running those reserves is a recurring, fee-generating business that expands as more dollars move on-chain.

The GENIUS Act, signed in July 2025, created a federal framework that allows registered money market funds to back stablecoin issuance, turning a back-office function into a regulated product line.

The Hedge-Fund Angle: Why Tokenized Money Market Funds Could Become 24/7 Collateral

The reach extends past issuers. Tokenized money market funds can work as collateral, settlement assets and cash-parking tools for hedge funds, market makers and trading desks moving between traditional and crypto markets. BlackRock’s BUIDL already serves as accepted collateral across crypto trading venues, where a yield-bearing dollar instrument that settles outside banking hours suits margin, repo-style workflows and treasury management. Collateral here means assets pledged to support trading, borrowing or settlement obligations.

No issuer or fund has been named as a user of Invesco’s proposed fund, so for now the case stays potential rather than confirmed.

The Tokenized Money Market Fund Race

Invesco joins a crowded field. BlackRock’s BUIDL, run with Securitize, holds more than $2 billion and ranks as the largest tokenized Treasury fund. State Street and Galaxy launched SWEEP in May, a tokenized liquidity fund on Solana that uses PayPal’s PYUSD, while State Street separately rolled out a stablecoin-reserve money market fund with Anchorage Digital.

Franklin Templeton runs its BENJI fund, and JPMorgan placed a tokenized money market fund on public Ethereum. Tokenized Treasuries and money market funds now top $15 billion on-chain, per RWA.xyz, the largest real-world-asset category.

The Risks: SEC Approval, GENIUS Act Rules + Liquidity Stress

The risks are concrete. Invesco’s stablecoin reserve fund still needs the SEC to let it take effect, and several GENIUS Act rules from the Office of the Comptroller of the Currency (OCC), Federal Deposit Insurance Corporation (FDIC), and Treasury remain unfinalized, which the filing warns could force changes to its holdings. Under stress, a reserve fund can meet redemption pressure and liquidity mismatch if issuers pull cash at once.

Tokenizing shares adds smart-contract, cybersecurity, and blockchain-dependence risk that off-chain funds avoid. Tokenization is also not the same as liquidity: an onchain share trades appropriately only if active market makers stand behind it. Proof-of-reserve transparency has limits too, shaped by what the registry actually discloses.

The Bigger Disruption: Wall Street Is Moving to Control the Safest Layer of Crypto

Banks, asset managers, stablecoin issuers and payment firms are converging on one asset: cash-like digital settlement instruments backed by Treasuries. Tokenized reserve funds blur the line between money market funds, settlement rails, collateral management and digital-asset treasury operations.

The headline disruption may not be any single stablecoin. It may be the institutional reserve architecture forming beneath them, and traditional finance is moving to control that safest layer.

Author: Richardson Chinonyerem

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organisations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

How the Dow Jones Performs During Wars: Lessons from Iraq, Gulf War & Iran | Disruption Banking