Tokenized money market funds are reshaping finance. They blend the security of traditional investments with the speed of blockchain. Asset managers like abrdn and Franklin Templeton are leading the innovation. They have worked with blockchain experts to create funds that offer better liquidity, faster settlements, and broader access.

A new Digital Opportunities (or DigOpp) report reveals that 41% of these funds remain off-limits to U.S. investors. Regulatory hurdles are stifling progress in the world’s largest market. Can using blockchain help to cut through the red tape?

Tokenized funds could redefine our money markets, including bonds, gilds, and debt securities. But first, it’s key to understand the basics before we explore solutions. Let’s begin with what tokenized money market funds are and how they work.

What Are Tokenized Money Market Funds (MMFs), and How Do They Work?

Money market funds, sometimes called real-world asset (RWA) tokenized funds, were introduced in the 1970s. They offer low-risk investment options focused on short-term debt instruments like treasury bonds. They provide liquidity and stability, making them popular. Traditional models, however, come with delays in settlement and high operational costs. Something that is known as T+1, T+2, and often T+3, referring to the business days required to settle the payment.

Tokenization solves these issues by digitizing fund ownership, allowing near-instant transactions, greater transparency, and fractional ownership.

Why Are Big Players Like abrdn and Franklin Templeton Getting In?

Major financial institutions see tokenization as a breakthrough that can significantly cut settlement times. Early last year, a Disruption Banking story highlighted that central bank digital currencies (CBDCs), leveraging blockchain technology, could eliminate intermediaries in international trade transactions. In turn reducing processing times from days to seconds. This shift has drawn interest from firms seeking faster, more cost-effective financial operations.

In early 2023, abrdn took a step toward this transformation by tokenizing its money market fund on the Hedera blockchain. The firm partnered with Archax to launch institutional-grade tokenized investments, exceeding initial market expectations.

The company chose Hedera because of its ability to process high transaction volumes quickly and ensure that fund settlements happen almost instantly.

Meanwhile, Franklin Templeton, which manages $1.4 trillion in assets, has expanded its Franklin OnChain U.S. Government Money Fund (FOBXX) to Aptos, adding to its existing integrations with Stellar, Polygon, Avalanche, Arbitrum, Base, Ethereum and more recently, Solana. The company aims to make its tokenized funds available across multiple blockchain networks to increase accessibility.

Are Tokenized Money Market Funds a Success?

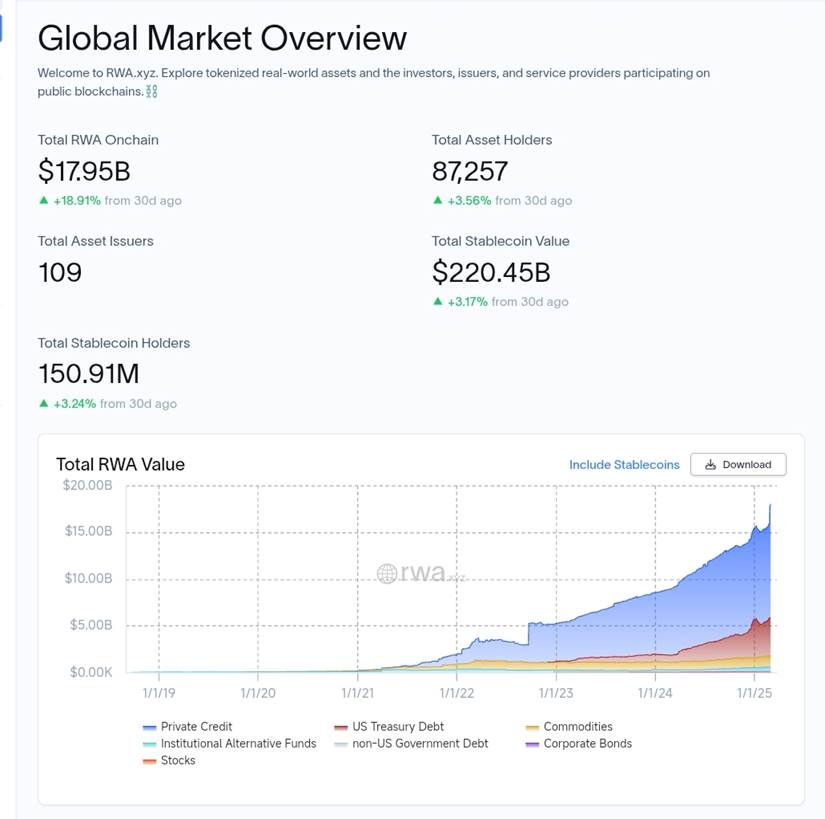

In a 2025 Disruption Banking story, Franklin Templeton CEO Jenny Johnson described tokenization as “securitization on steroids,” emphasizing its potential to redefine finance. The report noted, “FOBXX has been a harbinger of things to come for the tokenization of Real World Assets (RWAs),” which currently sits at nearly $18 billion, according to data from tokenized real-world assets tracker, RWA.xyz.

It’s strategy is paying off — Franklin Templeton’s tokenized fund now holds over $500 million in assets. The firm’s ability to operate across multiple blockchains has set a new standard in the industry, making tokenized money market funds a more viable investment option worldwide.

RWA value across segments. Source: RWA.xyz

The DigOpp Report: Why Are 41% of Funds Off-Limits to U.S. Investors?

DigOpp — a specialized financial firm that designs investment products and manages digital asset funds — released a report in January 2025. The report provides an in-depth look at the state of tokenized money market funds. Analyzing 37 different products, the study compares their underlying assets, blockchain platforms, and investment structures. Most of these funds invest in fixed-income securities, primarily with bonds less than one-year in maturity, including reverse repos, corporate paper, and t-bills.

The report suggests that many of these products are more accurately described as “tokenized cash alternatives” rather than traditional money market funds.

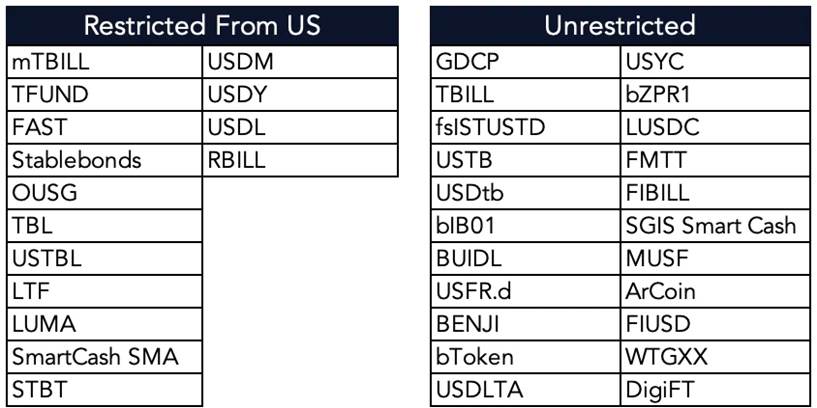

One of the most significant findings in the report is that 41% of these funds remain restricted to US investors. This is a significant regulatory hurdle. The report states how “US regulators are a problem for operating in digital assets. It is not uncommon for a crypto product to be restricted from US investors.”

Source: DigOpp

This restriction is particularly relevant for US-based investors, the report notes. The primary reason is regulatory uncertainty, as authorities remain undecided on whether these assets should be classified as securities or commodities. These regulatory barriers have led many issuers to block access for American investors, limiting participation in the growing tokenized finance market.

A list of funds Restricted and Unrestricted from US investors. Source: DigOpp

What Else Should you Consider with Money Market Funds?

Regarding how value accrues to the token (Value Accrual Mechanism), DigOpp’s analysis notes how “price accrual is the obvious favorite, with 67% of tokens using this mechanism.” Offering tax efficiency and simplicity in DeFi applications like automated market makers (AMMs) and lending pools. For example, if a token starts at $1 and accrues a 3% yield, its value becomes $1.03, avoiding the complexity of distributing additional tokens.

On the other hand, rebasing and distributions maintain a $1 peg, which is advantageous for stability, with rebasing distributing 0.03 more tokens for a 3% yield, totaling 1.03 tokens.

The report also examines the permissioned vs. non-permissioned structures of these funds. Permissioned tokens require KYC/AML verification, making them ideal for institutional investors. Non-permissioned tokens, on the other hand, are designed for DeFi use, offering greater liquidity and accessibility for decentralized finance platforms.

DigOpp describes its report as a starting framework for investors looking to integrate tokenized money market funds into their portfolios. The report states, “Our objective is to provide you with a simple starting framework for thinking about what is important in these products as you consider integrating them into your operation and conducting further due diligence.” This framework is part of DigOpp’s Counterparty Catalogue, a due diligence and market discovery tool for digital asset investors.

What’s Next for Tokenized Money Market Funds?

Despite the hurdles, adoption is growing fast. The DigOpp report found that most funds are backed by fixed-income assets like reverse repos, corporate debt, and Treasury bills. Investors are drawn to the idea of adding tokenized money market funds to their portfolios.

But how much progress has been made? This table summarizes some key players, their chosen blockchains, reported assets, and primary benefits, providing a snapshot of the sector’s progress so far.

Table: Summary of Key Players and Metrics

| Entity | Blockchain Platform | Reported Assets (Early 2025) | Key Benefit |

| abrdn | Hedera, Algorand and XRP Ledger (XRPL). | ~$3.8 billion (US dollar Liquidity Fund (Lux) fund) | Improved liquidity and democratized access to investors. |

| Franklin Templeton | Aptos, Stellar, etc. | Over $580 million (BENJI, U.S.-registered version of the fund) | Interoperability, high yields. |

| Ondo Finance | Ethereum, others | $434 million (Ondo’s Short-Term US Government Treasuries Fund (OUSG) TVL) | 24/7 trading, competitive yields, and integration with traditional financial systems through partnerships like Mastercard’s Multi-Token Network. |

There are further challenges to consider. Smart contract risks, for example, especially for third-party service providers, which some reports claim were the access point of the nearly $1.5 billion Bybit hack, are a major concern. Disruption Banking covered the hack last week, highlighting how the infamous North Korean ‘Lazarus Group’ was likely behind the largest ever web3 heist.

Further challenges include blockchain scalability, and the need for regulatory clarity. Firms like abrdn and Franklin Templeton believe these issues are solvable.

Tokenized financial products will become mainstream, but their success will depend on how quickly regulatory frameworks adapt to this new model.

For now, tokenized money market funds are carving out their place in the financial system. But U.S. investors might have to wait a little longer to join the party.

Author: Ayanfe Fakunle

#TokenizedFinance #MoneyMarketFunds #Blockchain #DigitalAssets #TokenizedMMFs #USRegulations #FinancialInnovation #Crypto #BlockchainTechnology

See Also:

Why are abrdn’s money market fund investments being tokenized using Hedera

Wall Street’s Crypto Makeover: How Franklin Templeton is Cashing in on Tokenization

FRANKLIN TEMPLETON LAUNCHES FRANKLIN ONCHAIN U.S. GOVERNMENT MONEY FUND | Disruption Banking