- The Irish economy has remained resilient in the face of consecutive external shocks.

- Growth is projected to slow but remain healthy amid trade and geopolitical tensions and elevated global uncertainty. Risks to the growth outlook are on the downside and to inflation on the upside.

- While the war in the Middle East demands near-term policy attention, the current strong economic position provides a window to future-proof the economy.

Washington, DC – June 29, 2026: The Executive Board of the International Monetary Fund (IMF) completed the Article IV Consultation[1] with Ireland, considered and endorsed the staff appraisal without a meeting on a lapse-of-time basis.

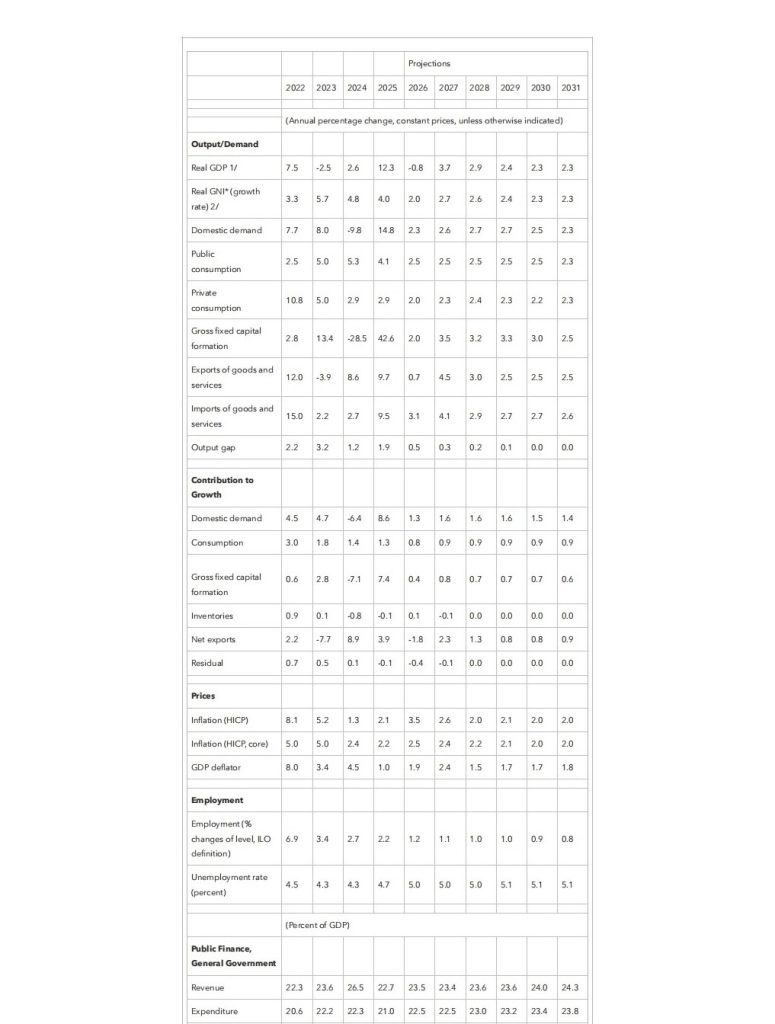

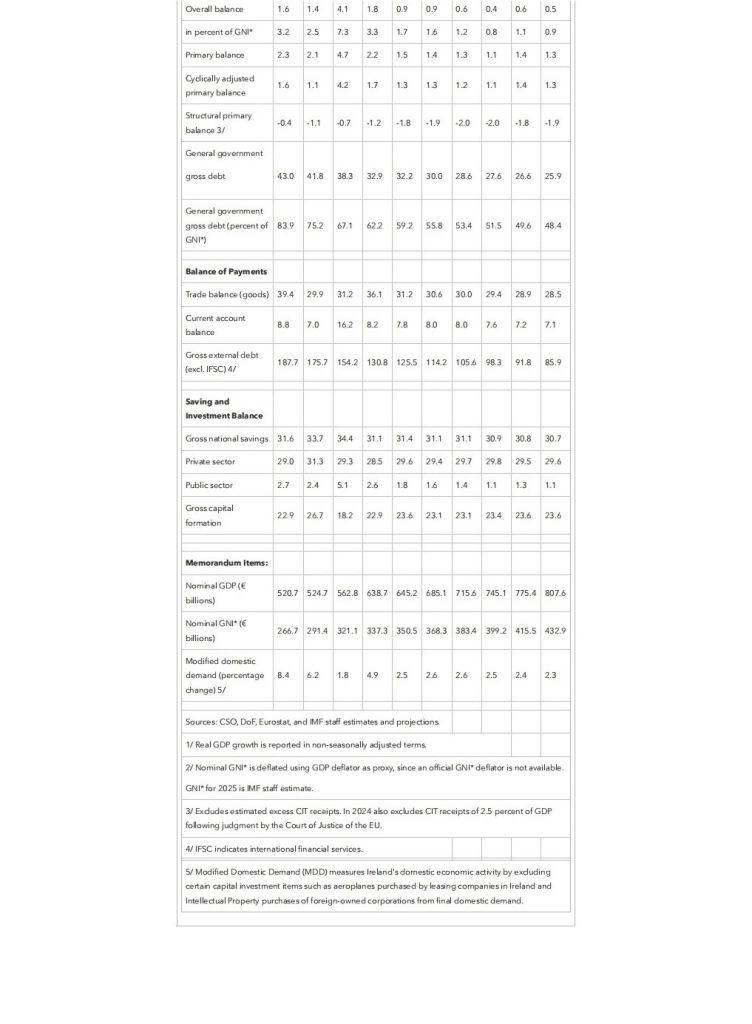

The Irish economy has remained resilient in the face of consecutive external shocks. The domestic economy, as measured by the Modified Gross National Income, is estimated to have grown by about 4 percent in 2025. Robust consumption and investment, together with strong exports dominated by foreign multinational enterprises (MNEs), contributed to solid growth. Headline inflation remained close to 2 percent in 2025 but has accelerated recently due to higher energy prices. The labor market has become less tight as employment growth slowed. The general government balance remained in a sizeable surplus in 2025, supported by continued strong corporate income tax receipts from MNEs.

The economy is projected to grow at a slower but still robust pace. Private consumption is expected to slow down due to weaker employment and real income growth. Modified investment is projected to normalize from the high 2025 level and would be supported by continued construction activity. Export growth is expected to slow significantly in 2026 and the current account surplus to moderate over the medium term.

Risks to the growth outlook are on the downside and to inflation on the upside. Substantial external risks stem from the war in the Middle East, contingent on the war’s intensity and duration. Ireland’s reliance on MNEs continues to be a key source of vulnerability. Rising geoeconomic fragmentation and elevated policy uncertainty could lead to further reorganization of supply chains and shifts in trade and capital flows that would be detrimental to Ireland’s globally integrated economy. The rapidly evolving landscape of AI poses novel risks, including threat to cyber security. Domestically, persistent supply-side constraints could weigh on productivity.

Executive Board Assessment[2]

The Irish economy has remained resilient and is projected to grow at a slower but still robust pace amid higher energy prices and global uncertainty. Modified domestic demand growth is projected to moderate from almost 5 percent in 2025 to about 2½ percent in 2026–27, largely reflecting a softening of private consumption due to weaker employment and real income growth, as well as normalization of modified investment. Headline inflation is projected to rise to about 3½ percent in 2026 and return to 2 percent around 2028. The outlook is subject to elevated uncertainty, with downside risks to growth and upside risks to inflation. Ireland’s external position is preliminarily assessed to be moderately stronger than the level implied by medium-term fundamentals and desirable policies.

Ireland’s current strong economic position provides an opportunity to future-proof its economy. Reliance on MNEs continues to be a source of vulnerability; housing and infrastructure gaps remain to be fully addressed; long-term spending pressures from aging and the green transition are looming; and the rapid development of AI presents both risks and opportunities. Given these vulnerabilities and risks in a more shock-prone and fragmented world, Ireland cannot take its resilience for granted and should use the current window to address vulnerabilities, improve productivity, and secure lasting prosperity.

Fiscal policy should achieve a broadly neutral stance while scaling up public investment efficiently. With the economy operating at full capacity and upside inflation risks, fiscal policy should avoid injecting unnecessary demand stimulus. Furthermore, a broadly neutral stance would help build buffers for future shocks and spending needs stemming from aging and the green transition. In case of downside risks materializing, automatic stabilizers should be allowed to operate fully. Any discretionary fiscal support should be temporary, targeted, and preserve price signals, to be accommodated within a broadly neutral fiscal stance, except in a severe downside scenario. Staff welcomes the authorities’ commitment to accelerating public investment and effective implementation will be key. Current expenditure needs to be closely managed, including through stronger controls to minimize overruns.

Broadening the tax base and strengthening the national fiscal framework would reduce vulnerability to the highly concentrated CIT and help prepare Ireland for long-term challenges. Increasing revenues from PIT, VAT, and local property taxes would provide more sustainable revenue sources for permanent spending commitments and allow for channeling more excess CIT revenues into the two savings funds. A stronger national fiscal framework would help Ireland balance competing priorities, enhance budget credibility, and safeguard sustainability. Given the lack of a fiscal anchor at present, the MTFSP should guide annual budgets and act as a binding mechanism on spending ceilings over the medium term.

Systemic risks have risen, warranting ongoing vigilance to safeguard financial stability. The financial system has proven resilient in the face of external shocks. But vulnerabilities in segments of Ireland’s large and complex non-bank sector related to leverage and liquidity mismatches could amplify and transmit adverse shocks. Asset quality should remain a key supervisory focus for banks. Macroprudential settings are appropriate, and the CBI should continue to review and adjust them as macro-financial conditions develop. Evolving risks from digitalization and cybersecurity require continued focus on operational resilience.

Strengthening regulation and supervision of non-banks requires continued efforts and cooperation with the international community. The CBI should maintain its leadership role in developing a macroprudential framework for non-banks and continue to monitor the implementation of the macroprudential measures for Irish property funds and GBP-denominated liability-driven investment funds. The CBI’s ongoing efforts, in collaboration with ESMA and other regulators, to improve data availability and quality, enhance risk assessment, and develop system-wide stress tests are welcome.

Structural reforms should focus on addressing housing shortages, enhancing energy security, and preparing for the AI transformation. Achieving the new housing targets will require further efforts to streamline the complex planning and judicial review process, increase urban density, boost construction productivity, and crowd in private capital. Upgrading the electricity grid, strengthening integration with the EU energy market, and harnessing Ireland’s potential in renewables are key to bolstering energy security and delivering a cost-effective green transition. Realizing AI-related productivity gains while ensuring adjustment does not undermine inclusive growth will require policies to help workers adapt and acquire new skills, enhance labor mobility, and foster innovation to leverage Ireland’s abundant talent.

The Irish economy would benefit significantly from deepening the EU Single Market. The SIU can facilitate the redirection of savings into productive investments, and Ireland’s financial sector, a global leader in asset management, is uniquely positioned to lead the transition. The proposed 28th corporate regime, if designed and implemented well, would enable Irish firms to operate more efficiently in the Single Market and bring economies of scale. Advancing new EU trade agreements would allow Irish firms to diversify supply chains and capture efficiency gains from trade.

[1] Under Article IV of the IMF’s Articles of Agreement, the IMF holds bilateral discussions with members, usually every year. A staff team visits the country, collects economic and financial information, and discusses with officials the country’s economic developments and policies. On return to headquarters, the staff prepares a report, which forms the basis for discussion by the Executive Board.

[2] The Executive Board takes decisions under the lapse-of-time procedure when the Board agrees that a proposal can be considered without convening formal discussions.

See also:

IMF Executive Board Concludes 2026 Article IV Consultation with Portugal | Disruption Banking