A Concluding Statement describes the preliminary findings of IMF staff at the end of an official staff visit or mission undertaken as part of regular consultations under Article IV of the IMF’s Articles of Agreement. The authorities have consented to the publication of this statement. The views expressed are those of the IMF staff and do not necessarily represent the views of the IMF’s Executive Board. Based on the preliminary findings of this mission, staff will prepare a report that, subject to IMF Management approval, will be presented to the IMF Executive Board for discussion and decision.

Bern – June 25, 2026:

- Switzerland’s strong policy frameworks and economic flexibility have supported stability and growth through the past year’s global volatility. Despite a challenging external environment, exports have remained resilient and the impact of the global energy price shock has been milder than in neighboring countries.

- While relatively slow this year, growth is expected to recover. The strong franc has mitigated upward pressure on inflation from energy prices, and inflation expectations remain within the SNB’s price stability range. The 2025 external position was broadly in line with medium-term fundamentals and desirable policies.

- Extending Switzerland’s success amid these and new challenges will require continued adherence to prudent policy frameworks. With the policy rate at zero, monetary policy is constrained but still has room to respond to shocks, as negative rates and FX intervention remain important tools. Implementation of the Too Big To Fail (TBTF) package, continued strengthening of financial sector supervision, and enhancing the macroprudential framework will deepen resilience. The debt brake helps ensure fiscal sustainability while preserving flexibility in response to severe shocks.

- Over the medium to long term, fiscal pressures from demographic change, the energy transition, and defense should be managed within the debt-brake framework. Structural reforms—alongside fiscal measures—should be taken to contain these costs, and in addition will support continued labor market flexibility, productivity growth, and environmental sustainability.

Context

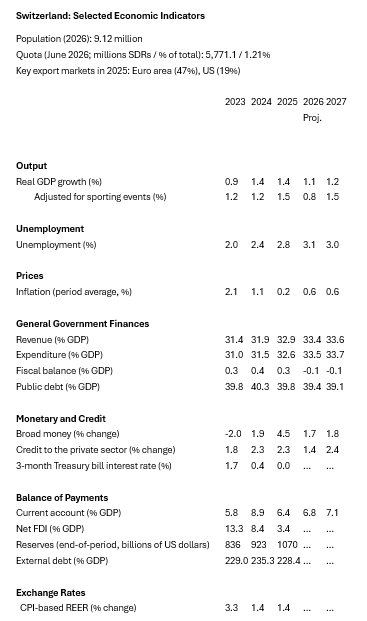

Switzerland has navigated global volatility well. Growth slowed in 2026, falling to 0.4 percent (adjusted for international sporting events) in Q1 y/y, amid subdued investment and weakened external demand. Inflation remained at 0.6 percent in May, but with limited pass-through from energy prices to underlying inflation, core inflation remained at 0.3 percent. Inflation expectations remain anchored around 0.7–1 percent. Full-year inflation is forecast at 0.6 percent, with pass-through from the stronger franc partly offsetting upward pressure from global prices and energy costs. Pension increases are generating a modest fiscal expansion, but the fiscal deficit and public debt remain low and sustainable. Despite trade uncertainty, goods exports (excluding gold valuables and merchanting) increased by 2.4 percent in 2025. Switzerland’s external position is assessed to be broadly in line with medium-term fundamentals and desirable policies.

Continued adherence to Switzerland’s strong policy frameworks will be key to maintaining growth and addressing medium-term challenges. The external environment remains challenging: high global energy prices raise domestic inflation while weakening trading partner growth and financial system shifts are making safe-haven inflows even less predictable. Monetary and exchange rate policy will thus have to remain nimble. Recent mandated increases to government spending should be managed within the debt rule. At the same time, maintaining the high quality of Swiss public services as the population ages and given other spending pressures will be challenging. Growth would be strengthened and made more sustainable by focusing on improving productivity—especially among SMEs —addressing labor mismatches, and continuing the carbon transition.

Economic Outlook

Inflation and growth will remain subdued in the near term. Sluggish growth among trading partners and elevated geopolitical and tariff uncertainty have weakened external demand. But accommodative monetary policy, strong housing demand, and recent real wage gains should keep growth in 2026 around 0.8 percent. As the global economy recovers, growth should rebound to 1.5 percent in 2027 (1.2 percent without adjustment for international sporting events). Inflation is projected to remain subdued (0.6-0.7 percent in 2026-28) as continued franc strength weighs on import prices.

The main risks are external and tilted to the downside. Adverse geopolitical events, higher energy prices, and renewed trade tensions could weigh on growth and exports. In the long run, increasing trade fragmentation could undermine potential growth by disrupting supply chains and Switzerland’s export-driven growth model. In a downside scenario, weaker external demand and higher commodity prices could reduce GDP growth by about 0.3 ppts over 2026-27. However, inflation would rise only modestly and stay within the SNB’s 0–2 percent range. A more severe stagflationary shock could lower growth by an additional 0.6 ppts over two years and raise inflation further, potentially requiring tighter monetary policy. Overall, the strong monetary policy framework will continue to support resilience, with fiscal buffers available if needed.

Fiscal Policy: Managing Rising Expenditure Pressures

This year’s modest fiscal expansion is cyclically appropriate. The 13th monthly pension payment beginning this year will outweigh higher corporate tax revenues from OECD Pillar 2 implementation, shifting the general government balance to a deficit of 0.1 percent of GDP (the Confederation deficit would remain broadly stable at 0.2 percent of GDP). With energy prices and global uncertainty weighing on growth, this expansion (0.2 percent of GDP cyclically adjusted) is appropriate.

Switzerland’s debt brake has kept debt sustainable, but medium- and long-term spending pressures will have to be addressed.

- By making spending and revenue decisions transparent, the debt brake ensures clarity and predictability in fiscal policy. It proved sufficiently flexible to accommodate significant relief spending—for example, during the COVID-19 pandemic and to provide support to Ukrainian refugees. Recourse to emergency spending provisions may be needed under another severe shock.

- Higher mandated pension and defense spending will require additional tax effort to comply with the debt brake. Following expenditure reductions in 2024-25 and Relief Package 27, which reduces the deficit by 0.2 percent of GDP, further consolidation will likely be needed during 2027-29. Additionally, without further measures, reducing the amortization account—now estimated at CHF 26 billion—as required to offset previous emergency spending will be challenging.

- While public debt is expected to remain low, additional challenges are on the horizon. Rising pressures from pensions, health care, and climate policies could increase deficits and public debt substantially by 2060. With discretionary expenditure already contained, spending cuts are not feasible; revenue reforms will thus be necessary. Switzerland’s tax rates are low compared to other OECD countries, and this would remain the case even if the fiscal gap were closed with a gradual VAT rate rise over the long term. The required adjustment could also be reduced through other tax reforms, including base broadening or greater collection efficiency.

Monetary Policy: Managing Increasingly Frequent Shocks

The monetary policy stance is appropriate, but high uncertainty warrants maintaining flexibility to adjust policy rates in either direction. With inflation expectations well anchored within the 0-2 percent price stability range—and above current inflation, the current mildly expansionary stance supports price stability. Going forward, the SNB should continue to look through temporary energy shocks, although under a stagflation scenario triggered by a sharp and sustained rise in energy prices, higher interest rates might be necessary to keep inflation expectations anchored. However, a severely disinflationary demand shock—especially in conjunction with safe‑haven inflows and currency appreciation—could push inflation and inflation expectations down significantly, in which case negative interest rates, despite possible financial system distortions, are the strongest of the SNB’s policy options in such a deflationary environment. In any case, the costs and benefits of all options need to be considered.

Foreign exchange intervention (FXI) can also be an effective tool in specific cases, but has limitations. When inflation expectations are in danger of being de-anchored, especially amid safe haven financial inflow surges, and to smooth their impact, FXI can be a useful tool to support monetary policy, as it is targeted and flexible. However, FXI are not intended to address underlying macroeconomic imbalances, and by expanding the central bank’s balance sheet, can heighten financial risks. In case of severe disinflationary shocks, FXI is thus best used as a complement to negative policy rates.

The SNB’s monetary policy framework remains appropriate. The SNB’s flexible 0–2 percent stability range is highly credible, and medium- to long-term inflation expectations are anchored around 1.0 percent. The SNB should avoid allowing expectations to drift too far below this level, as this would weaken monetary policy effectiveness and raise financial stability risks. Clear communication —signaling a willingness to keep rates low or negative and to deploy FX interventions—would be key to sustaining well‑anchored expectations.

Financial Sector: Enhancing Systemic Resilience

The authorities’ determination to implement their TBTF agenda is welcome, though some additional measures noted in the 2025 FSAP would reinforce the package.

- The proposal to require G-SIBs in Switzerland to fully back foreign subsidiaries with CET1 capital is targeted, commendable, and in line with FSAP recommendations.

- The SNB’s new Extended Liquidity Facility (ELF), to be introduced in 2027, will enhance the safety net, and final approval of the long-standing proposal to fund a public backstop would further reinforce stability.

- Ongoing increases in FINMA staffing and proposed increases to its powers are welcome. This includes enabling FINMA to fully mandate and oversee external audit, and to further limit suspension of enforcement of FINMA decisions during legal appeals.

The macroprudential framework and toolkit should be strengthened to address rising systemic risks. The high concentration of lending in real estate exposes the banking sector to significant risks. Prices in the owner‑occupied segment are estimated at well above fundamentals, compressed residential rental yields raise default concerns, and the share of loans not meeting banks’ own affordability criteria is still high. While progress on interagency cooperation is welcome, establishing a dedicated macroprudential committee would help overcome potential inaction bias and improve policy design within the context of existing institutional mandates. With the sectoral countercyclical capital buffer (SCCyB) already fully deployed, new measures, such as borrower-based measures that target affordability, a higher limit on the SCCyB, or higher risk weights could help contain vulnerabilities. Complementary policies to streamline approvals and ease permitting would facilitate construction, reducing pressure on real estate markets.

Risks among Switzerland’s non-bank financial institutions (NBFIs) are generally contained. Supervisors should remain vigilant regarding insurers’ derivative exposures and existing data gaps. Rising housing market risks could eventually lead to vulnerabilities in institutions that issue covered bonds backed by mortgages and in the banks that use them for funding. Although these risks are contained, continued monitoring of linkages across the financial system is warranted, as is improved cooperation with other supervisors to understand linkages between the Swiss financial system and foreign-domiciled NBFIs.

Other reforms would also add to financial system resilience. Rising cyber risks—including those driven by rapid AI development—underscore the need to reinforce risk management and regulatory frameworks. Further refinements to risk-based AML/CFT supervision, including enhanced oversight of “gatekeeper” professions (e.g., financial and legal advisors) would help, while the recent introduction of the beneficial owner registry will increase transparency.

Structural Policies: Enhancing Productivity and Resilience

Given age-related fiscal pressures, comprehensive pension and healthcare reforms are a top priority. Structural deficits in Pillar 1 public pensions could reemerge after 2030, underscoring the need to improve sustainability. Key measures could include linking retirement age to life expectancy and indexing pension benefits only to inflation. For Pillar 2, aligning conversion rates with longevity would help reduce cross‑subsidization. Consolidation of the fragmented pension fund industry could enhance efficiency, while facilitating greater competition among pension fund asset managers could enhance the overall risk-return profile. Strengthening incentives for delayed retirement e.g., raising eligibility ages for Pillar 2 pensions or allowing pension accrual beyond retirement age — would support sustainability of both pillars. In health care, while recent reforms are welcome, additional efforts are needed to contain costs such as expanding integrated care models, accelerating digitalization, and reinforcing cost accountability. Cantonal-level measures such as expanded access to targeted subsidies would help ensure the long‑term affordability of mandatory health insurance.

Addressing labor shortages would ease business constraints. Aging and skill mismatches are tightening labor supply, especially in high‑skill sectors and construction. Policies should prioritize targeted upskilling—ensuring vocational training continues to adapt to rapid technological change—and improve mobility between academic and vocational paths, particularly as the use of AI spreads. Beginning no later than 2032, the income tax is expected to be civil-status neutral, which should boost employment of women. This should be complemented by enhancing access to affordable childcare. Maintaining openness to skilled migration is also key to maintaining Switzerland’s high level of labor market flexibility.

Additional reforms would further strengthen productivity. Switzerland’s productivity remains strong, supported by innovation, a high-quality and flexible educational system, and global integration, but weaknesses persist among SMEs and in services. Further reforms should focus on reducing regulatory burdens, especially by streamlining procedures for smaller firms and harmonizing rules across cantons. Higher risk appetite among pension funds could support scaling up productive investment for SMEs and startups, boosting business dynamism, and lowering the cost and complexity of dispute resolution and contract enforcement would encourage investment.

Switzerland should build on its low‑carbon energy mix to enhance resilience. Electricity generation already relies heavily on hydro (about 60 percent) and nuclear power (about 30 percent), though fossil fuels remain important in transport and heating. Recent policy measures aim to accelerate renewable energy and grid expansion (the “Acceleration Decree” adopted in September 2025) while improving energy security through greater integration with the EU electricity market (one part of the “Bilaterals III” package). Further climate action should focus on strengthening carbon pricing to promote electrification of transport and heating, alongside targeted support for energy‑efficient building upgrades.

* * * * *

The IMF team thanks the Swiss authorities and other stakeholders for their hospitality, engaging discussions, and productive collaboration. We are especially grateful to the SNB and the State Secretariat for International Finance of the Federal Department of Finance for assistance with arrangements.

Sources: IMF’s Information Notice System; Swiss Institute for Business Cycle Research; Swiss National Bank; IMF World Economic Outlook database; and IMF staff estimates and projections.

See also:

IMF Executive Board Concludes 2026 Article IV Consultation with Portugal | Disruption Banking