London-based systematic hedge fund Aspect Capital, managing $9 billion, is opening its established absolute return systematic futures program to international investors for the first time as allocators intensify the search for diversifying returns amid mounting risks in traditional portfolio.

As the “war premium” tied to the U.S.-Israeli strikes on Iran fades from Brent crude prices and the CLARITY Act continues to reshape the digital asset sector, institutional investors are increasingly seeking sources of uncorrelation. Rather than chasing growth, many are prioritising return streams that are less sensitive to Federal Reserve policy shifts or geopolitical developments in the Strait of Hormuz.

The World Bank forecast Brent crude would average $86 a barrel in 2026, up from $69 in 2025, assuming the most acute Middle East disruptions ease in May and shipping through the Strait of Hormuz gradually normalises by late 2026.

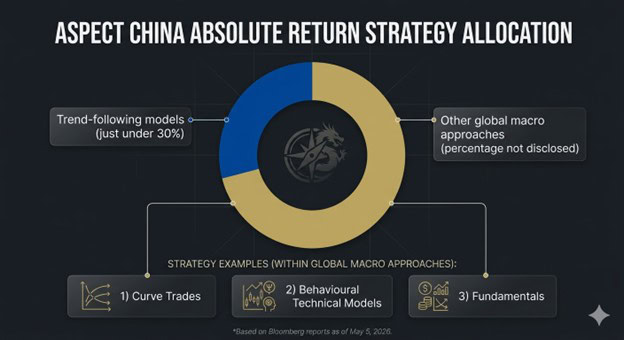

Aspect Capital began offering its China absolute return systematic futures strategy to global investors in early April, according to Chief Product Strategist Razvan Remsing. The strategy, which has been available to mainland Chinese investors since July 2019, trades across 65 Chinese futures markets and currently oversees approximately $550 million.

China Futures Without the Equity Risk

This is not a “buy the dip” play on Chinese equities. It is not a simple China Securities Index (CSI) 300 or Morgan Stanley Capital International (MSCI) China proxy. It is a China absolute return strategy, meaning it aims to make money in both rising and falling markets rather than simply ride a benchmark higher.

That’s a relevant piece of information because many investors remain cautious about Chinese equities. A futures-based global macro strategy gives them a different entry point: commodities, bond futures, stock index futures, curve trades, and systematic signals.

Why the Other 70% Makes This Strategy Stand Out

Just under 30% of the strategy is based on trend-following models. Trend-following models try to profit when prices keep moving in the same direction. They can work brilliantly in sustained trends. They can also get punished in violent reversals.

The remaining portion is where the more interesting allocator case sits. Bloomberg reported that the rest of the strategy uses other global macro approaches, including curve trades, technical models that exploit behavioural patterns, and fundamental models.

Curve trades look at changes in the shape of futures or bond curves, not just the outright price. Behavioural technical models try to exploit repeatable market patterns. Fundamental models look at supply, demand, policy, growth, inflation, and inventory data.

Put simply, this is not a single-engine CTA, but a multi-engine systematic China macro strategy.

Eggs, Glass & Rubber: Inside China’s Unique Futures Markets

The commodity engine is the point.

Aspect’s strategy trades mainly Chinese commodity futures, alongside eight stock indices and bond futures. That mix gives the fund access to China’s real economy without forcing it into Chinese equities.

China’s futures markets include contracts that are either unavailable or far less central in Western markets. Aspect’s co-founder and research director Martin Lueck previously noted that Chinese exchanges include contracts on coal, glass, PVC, polyethylene, eggs, palm oil, lead, and rubber. Hedgeweek also reported that Aspect’s China strategy covers markets including urea, potash, silicon manganese, and glass.

These are not decorative markets. They sit close to manufacturing, construction, agriculture, technology supply chains, and infrastructure demand.

CME Group noted that China processed 45% of the world’s copper in 2024. The International Energy Agency (IEA) said China’s grid investment was the single largest contributor to copper demand growth over the previous two years.

That is why Chinese commodity futures matter. They can act as a live macro signal for industrial demand, infrastructure cycles, supply pressure, and policy stimulus. For a global macro allocator, that is more useful than another equity beta product.

Why Allocators Want the Backdoor Now

Allocator demand is not hard to understand. The world is harder to hedge.

BNP Paribas found in its 2026 Hedge Fund Outlook that 9% of allocators invested in China-focused hedge funds in 2025 and a further 14% planned to do so in 2026, a reversal from a 42% net reduction in 2023. Reuters also reported that hedge funds were trimming North America exposure amid trade tensions, dollar pressure, and mega-cap weakness.

That does not mean allocators suddenly love China. It means they dislike overdependence on U.S. assets.

Man Group argued that elevated inflation regimes require investors to rethink diversification because bond diversification benefits depend heavily on the macro regime. HFR reported that hedge fund industry capital reached a record $5.22 trillion in Q1 2026 as investors favoured hedge funds during volatility and uncertainty.

This is the real allocator question: what can make money when U.S. equities, bonds, oil, gold, and the dollar are all being pulled by the same geopolitical shock?

A China futures strategy is one answer. Not the answer. One answer.

How Aspect Navigates China’s QFI Rules for Global Access

Trading China is not straightforward. It is notoriously complex. That is part of the attraction and part of the problem.

Aspect manages this through a Qualified Foreign Investor (QFI) license, providing direct access to 45 of its 65 targeted markets. The remaining 20 are accessed via total return swaps with local counterparties.

This hybrid structure is designed to mitigate the operational risks that have historically scared off Western capital. By using an offshore vehicle to mirror its onshore strategy (which has returned an annualized 11.5% through March 2026), Aspect is effectively selling a “sanitized” version of mainland volatility.

Aspect also said it has been researching Chinese futures markets for more than 10 years, qualified as a Qualified Foreign Investor in 2022, and registered Aspect China as a Wholly Foreign Owned Enterprise in Shanghai’s Pilot Free Trade Zone in March 2024.

That infrastructure is pivotal. Clearly, this is not a London desk casually pointing models at Chinese prices.

The “Black Box” Risk: Absolute Return is Not Risk-Free

Despite the 16% returns in 2024 and 11% in 2025, investors must remain skeptical. An absolute return strategy, one that aims to profit regardless of whether markets are up or down, is only as good as its underlying models. Those numbers will sell; but they do not remove the risk.

China is a policy-heavy environment. A sudden regulatory pivot by the CCP or a freeze in the futures markets could render even the most sophisticated “curve trade” model useless overnight. Furthermore, while the strategy has an estimated capacity of $1.5 billion, the liquidity of “exotic” contracts like liquid glass can vanish during a systemic credit squeeze.

Reuters showed the danger in October 2024, when Winton’s China strategy was hit after Beijing’s surprise stimulus triggered sharp reversals across stocks, bonds, and commodities, hurting trend-following positions.

That is the warning label. Absolute return does not mean risk-free. It means the strategy is trying to make money without depending on market direction. That attempt can still fail.

A Hedge, Not a China Bet

Aspect Capital is not asking global allocators to believe in the Chinese equity market. It is asking them to believe that China’s futures markets offer a distinct source of risk and return.

That is the arbitrage of divergence.

The real test will not come when trends are clean and volatility is friendly. It will come when Beijing shifts policy, liquidity thins, commodity curves break, and geopolitical risk hits the tape at the same time. That is when Aspect’s China strategy will prove whether it is genuine diversification, or just a sophisticated black box in a market that still changes the rules mid-match.

Author: Richardson Chinonyerem

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organizations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

Are Dow Jones Components Targets for Activist Hedge Funds? | Disruption Banking