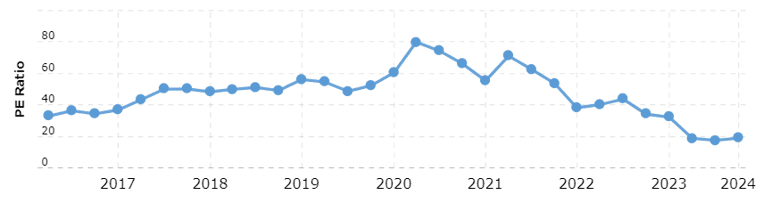

PayPal’s shares are trading at their lowest level since 2019, based on its current P/E ratio of 18.86, which is far below its five-year average of 51.74. But low P/E ratios can be misleading. Not every cheap stock is a bargain. Some stocks are cheap for a good reason, and some are cheap for a bad reason. PayPal seems to belong to the latter category.

PayPal is the cheapest it’s been in more than five years. Source: Macrotrends

Cheap stocks can be either value plays or value traps. Value plays are stocks that are undervalued by the market, but have strong fundamentals, growth prospects, and resilience. Value traps, on the other hand, are stocks that appear undervalued, but have weak performance, poor outlook, and high risk. To distinguish between them, investors need to dig deeper and examine the underlying factors, as both can look attractive on the surface.

Disappointing Outlook Drives Stock Lower

PayPal is a tempting target for value investors, as it trades at a low multiple compared to its peers. However, low multiples can also signal a value trap, which is a stock that looks cheap but has no catalysts for growth or recovery. Value traps often result from financial distress, competitive disadvantage, or poor capital allocation. PayPal does not suffer from financial distress, but it does face increasing competition and slowing growth in its core business.

The company’s Q4 2023 earnings report, released on Feb 7, showed that PayPal beat analysts’ expectations on both revenue and earnings. However, the stock plunged nearly 10% in pre-market trading on Feb 8, as investors were spooked by the company’s weak guidance for 2024. PayPal expects GAAP earnings of about $3.60 per share in 2024, down from $3.84 in 2023 and below the consensus estimate of $4.03. The company also expects revenue growth to slow down to 14% in 2024, compared to 18% in 2023 and 22% in 2022.

The main reason for PayPal’s dim outlook is the intensifying competition in the digital payments space. PayPal faces pressure from rivals such as Square, Stripe, Apple Pay, Google Pay, and Amazon Pay, as well as traditional banks and credit card companies.

Therefore, PayPal may not be a bargain after all. It may be a value trap that lures investors with a low valuation but fails to deliver growth or profitability. Investors should be wary of falling into this trap and look for more compelling opportunities elsewhere.

Restoring Investor Confidence

PayPal CEO Alex Chriss announced a new strategy to boost the company’s profitability and share price, which has been lagging behind its peers in the Nasdaq 100 Index. The strategy involves cutting costs by reducing the company’s workforce by 9%, or about 2,500 jobs, in 2024. The layoffs will be done through a combination of direct terminations and not filling open positions.

The memo sent by Chriss to the employees said that the move was necessary to streamline the business and increase its agility and responsiveness to customer needs. The layoffs will hit hard in San Jose, where hundreds of workers will lose their jobs. PayPal had about 29,900 employees worldwide at the end of 2022, with about 40% of them based in the U.S.

PayPal’s market cap has crashed. Source: Seeking Alpha

PayPal’s stock has been on a downward spiral since reaching its all-time high in July 2021, when it had a market cap of about $346 billion. As of February 2024, its market cap had shrunk to $66 billion, indicating a significant loss of investor interest in the stock in the past three years. It remains unclear whether the layoffs will be enough to turn around PayPal’s fortunes, as the company faces stiff competition from other payment platforms and fintech startups.

Competition Mounts

PayPal makes money mainly from charging fees on payment transactions. These fees include charges for currency conversions, cross-border transactions, and fund transfers. Besides transaction fees, PayPal also generates revenue from other value-added services, such as interest and fees on its loan receivables and assets.

However, PayPal is not the only option for online payment. There are many competitors that offer different features and benefits for online businesses and consumers. For example, Square is a popular service among businesses that need point-of-sale systems and payment processing. Square also provides tools for invoicing, payroll, and e-commerce. Another example is Stripe, a service that enables online businesses to accept payments seamlessly and securely. Stripe integrates with many platforms and supports various payment methods, including cryptocurrencies. Other notable services include Payoneer and Google Pay.

The financial services industry has been undergoing rapid changes with the emergence of fintech innovations. One of the latest trends is the interest that customers can earn on their accounts, which many neo banks and challenger banks are offering. In the US, one such service is Wise, which offers fast, secure, and affordable international transfers. Wise pays customers interest daily and monthly, unlike many traditional banks that pay interest annually.

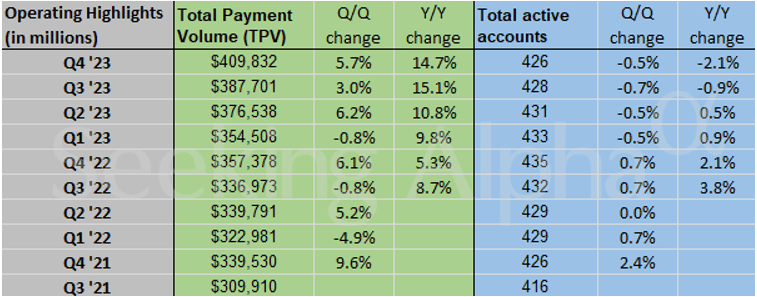

PayPal’s active accounts have stagnated since 2022, pointing to increase competition. Source: Seeking Alpha

Amidst this mounting competition, legacy players like PayPal are coming under pressure. This competitive pressure is reflected in the plateauing of its total active accounts in recent quarters. The company disclosed in its latest earnings call that total active accounts totalled 426 million by the end of 2023, down from 428 million on September 30th and 435 million on December 31st 2022.

Give It Time?

PayPal has been a leader in online payments for over two decades. It has a strong and profitable business model, with a large and loyal customer base. The stock price is currently undervalued, which could offer an opportunity for investors. However, the company faces some challenges, such as growing competition and changing consumer preferences. The management and the analysts agree that PayPal needs to invest in new products and services to regain its edge. The question is how long it will take for these efforts to pay off and boost the stock performance.

In response to the company’s recent earnings, Wall Street analysts said the dim outlook for 2024 will weigh on shares in the near term. “It’s clear that 2024 will be more of a transition year than we were expecting, with previously targeted operating leverage coming after 2024. We expect pressure on the stock as estimates come down,” JPMorgan wrote.

“We’re doing a lot of things to drive change internally and externally. However, nothing happens overnight. It will take time for some of our initiatives to scale and move the needle,” said chief executive Chriss on the earnings call.

According to Jason Kupferberg, a senior payments analyst at Bank of America, the main challenge for the company is the lack of growth in transaction profits for the next two years. He expects this metric to remain flat in 2024 and 2025, disappointing investors who hoped for a recovery after a stagnant 2023. “It takes time to turn around a big battleship,” Kupferberg said, stressing PayPal must put real effort into new initiatives that would spark growth.

Author: Acutel

We are global investors who invest in good companies at fair valuation and speculate on all else subject to the risk exposure we can afford.

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organisations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.