Pershing Square Inc.’s June 4 Form 8-K and Form 10-Q put Bill Ackman’s 2026 milestone in plain view. Pershing Square is trying to become a larger, more public investment platform through Pershing Square Holdings (PSH), Pershing Square USA, Ltd. (NYSE: PSUS), and Pershing Square Inc. (PSI, the listed parent asset manager trading as NYSE: PS). But the move is landing while short-term performance is weaker.

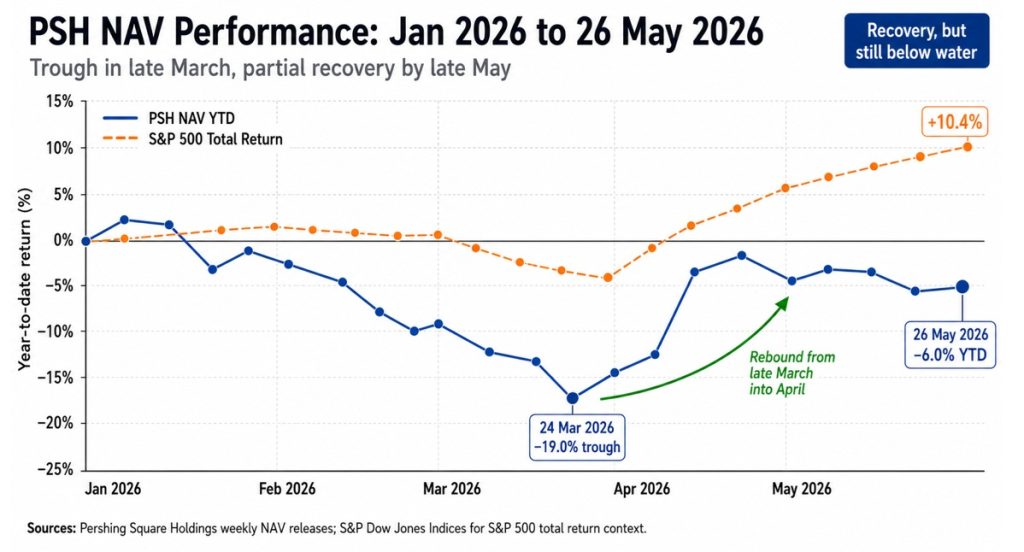

According to Ackman’s annual investor presentation, PSH reported net asset value (NAV) was down -5.4% year-to-date (YTD) in early 2026 after rising +20.9% in 2025. By May 31, the latest PSH NAV table showed a smaller but still negative –4.7% YTD return. That does not erase Ackman’s long record. It does make the pitch harder. Public permanence is easier to sell when NAV is compounding, not recovering from a drawdown.

The June 4 Filings Show the New Pershing Square Machine

The 8-K filing showed Pershing Square released extra April data so investors could understand the business through the April 30 closing of the combined PSUS initial public offering (IPO) and PSI listing. PSH is the older London-listed closed-end fund. PSUS is the new U.S. closed-end fund. PSI is the management-company listing meant to give public investors exposure to Pershing Square’s fee stream and platform growth.

The 10-Q filing revealed that PSUS and PSI began trading on the NYSE under “PSUS” and “PS”, and gross PSUS proceeds from the combined transaction were $5 billion. The market reception was rough.

Reuters reported that PSUS closed about 18% below its $50 IPO price on its first trading day. That is a relevant piece of information because the whole structure depends on investor confidence in closed-end permanence.

AUM Jumped, But the Discount Problem Did Not Disappear

Pershing Square reported April 30 asset under management (AUM) of roughly $17.8 billion for PSH, $4.93 billion for PSUS, $1.13 billion for Pershing Square, L.P., and $329 million for Pershing Square International. Total core-fund AUM reached $24.19 billion, or approximately $33 billion including Howard Hughes Holdings (NYSE: HHH). In asset-gathering terms, PSUS worked. In market-confidence terms, the evidence is mixed.

PSH’s April fact sheet described PSH as a closed-ended fund normally holding 8 to 12 large-cap positions, but it also showed a 31.1% dollar share-price discount to NAV. PSH kept buying back stock: on June 4 it bought 2,538 public shares at an average price of $53.61 while NAV was $81.12. Buybacks help, but a persistent discount is still the market’s blunt vote on structure, liquidity, and trust.

Why Vantage Turns HHH Into More Than Real Estate

The 10-Q reported Howard Hughes Holdings (HHH) agreed to buy Vantage Group Holdings, a privately held specialty insurance and reinsurance company previously backed by Carlyle and Hellman & Friedman, for about $2.1 billion in cash, and that the acquisition closed on June 4, 2026.

Ackman, Executive Chairman of Howard Hughes said in the deal announcement “Vantage will now become the cornerstone of Howard Hughes’ transformation into a diversified holding company”. For Ackman, HHH is no longer just a real-estate holding. It is becoming a Berkshire-style experiment built around real assets, insurance capital, and investment management.

Pershing Square will manage Vantage’s investment portfolio on a fee-free basis. No advisory fees. No management fees. Ackman is betting that the alignment, rather than the fee income, produces better long-term outcomes. Over time, Vantage’s portfolio will be directly invested in Treasurys and a portfolio of common stocks. That is the float-driven equity investment model, applied to a specialty insurer.

Whether the model works depends on two things that remain unproven: Vantage’s underwriting profitability and Ackman’s stock-picking performance in 2026 and beyond. On the first, Vantage has built a credible track record since its 2020 founding. On the second, the current year has not been kind.

Ackman Buys Microsoft While Loeb Moves Toward Alphabet: Two Sharpest Minds, Opposite AI Calls

The divergence between Pershing Square and Third Point on technology is one of the most instructive trades in the hedge fund industry right now. According to Reuters and confirmed by 13F filings, Ackman spent Q1 2026 building a new Microsoft position of 5.65 million shares, roughly $2.1 billion, while simultaneously cutting his Alphabet stake by 95%, dumping approximately $1.9 billion worth of shares across both Class A and Class C.

Daniel Loeb did the reverse. Third Point sold 925,000 Microsoft shares in Q1, liquidating a position held since late 2022, while buying 175,000 shares of Alphabet worth $50.3 million in a Class A position.

Ackman’s rationale is structural. He entered Microsoft at roughly 21x forward earnings, near a decade low for the stock, citing Azure’s cloud share gains, the Microsoft 365 enterprise lock-in, and what he described as an undervalued 49% stake in OpenAI. Loeb’s move toward Alphabet reflects a different read: that Google’s AI integration into search, YouTube monetization, and Google Cloud will prove more durable than the market currently prices in.

Both cannot be right over the same time horizon. But the divergence exposes something important about the current AI trade: the “Magnificent Seven” is no longer a single exposure. Hedge funds are now rotating between AI winners rather than buying the cohort wholesale. Ackman’s Microsoft bet has already recovered ground from the February lows, though PSUS’s post-IPO discount suggests investors are not yet rewarding his structural conviction with a premium.

The UMG Buyback Complicates Ackman’s Public-Market Pitch

PSH’s own fact sheet warns that past performance is not necessarily indicative of future results. That warning cuts both ways. A weak 2026 start does not kill Pershing Square 2026. But listed vehicles are judged daily by NAV, discount, liquidity, and credibility.

Reuters also reported that Universal Music bought back more than 14 million shares (~€250M/~$290M) from Pershing Square after rejecting Ackman’s takeover proposal (~$64B), adding another moving part to the portfolio.

The Harder Question for 2026: Can Ackman Sell Public-Market Permanence While Pershing Square NAV is Falling?

Pershing Square’s public market structure adds a layer of accountability that did not exist when the firm operated purely through PSH on the London Stock Exchange (LSE). PSUS and PS trade on the NYSE. Every quarterly filing discloses positions, NAV, AUM, and performance. Ackman can no longer operate with the opacity available to a private fund.

That accountability is exactly what he says he wants. It is also what makes a -5.4% NAV decline in the opening months of 2026 immediately visible. Investors who bought into PSUS at $50 are sitting at a discount. Investors in PSH have watched NAV move from -19% in March to -6% by late May, a meaningful recovery, but still a loss.

The Vantage deal and the Microsoft position are both long-duration bets. Neither resolves in 2026. The question Ackman’s investors are asking is whether the structural conviction, ie. public markets, permanent capital, fee-free insurance float, a concentrated equity portfolio, is strong enough to justify holding through a difficult year.

That is the question now. Can Pershing Square sell permanence while near-term NAV looks weaker? The answer is not no. But Ackman has less room for narrative. He needs NAV growth, narrower discounts, and proof that concentration still works when AI is no longer one obvious bet.

Based on the June 4 filings and the disclosed portfolio moves, Ackman’s answer is clearly yes. Whether the market agrees will take longer to determine.

Author: Richardson Chinonyerem

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organisations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.