The wait is over. On March 17, 2026, the U.S. Securities and Exchange Commission, along with the Commodity Futures Trading Commission, published a 68-page joint interpretation that formally classifies crypto assets under federal law. Sixteen assets have been named as digital commodities. That’s in writing, from both agencies, right now.

This is the most consequential U.S. crypto policy document of the year. Probably the decade.

What the SEC’s Token Taxonomy Actually Says

The taxonomy divides digital assets into five groups: digital commodities, digital collectibles, digital tools, stablecoins, and digital securities. Only digital securities, tokenized versions of traditional financial instruments like stocks or U.S. Treasuries, remain firmly under SEC jurisdiction.

Speaking at the DC Blockchain Summit in Washington, SEC Chair Paul Atkins said, “We’re not the ‘securities and everything commission’ anymore.” His agency is planning a formal rulemaking process shortly after, which will introduce an innovation exemption and additional guardrails.

The CFTC joined in, with Chairman Michael Selig stating, “With today’s interpretation, the wait is over. Chairman Atkins and I are committed to fostering a regulatory environment that allows the crypto industry to flourish in the United States with clear and rational rules of the road.”

The 16 Named Digital Commodities: BTC, ETH, XRP, SOL, and Beyond

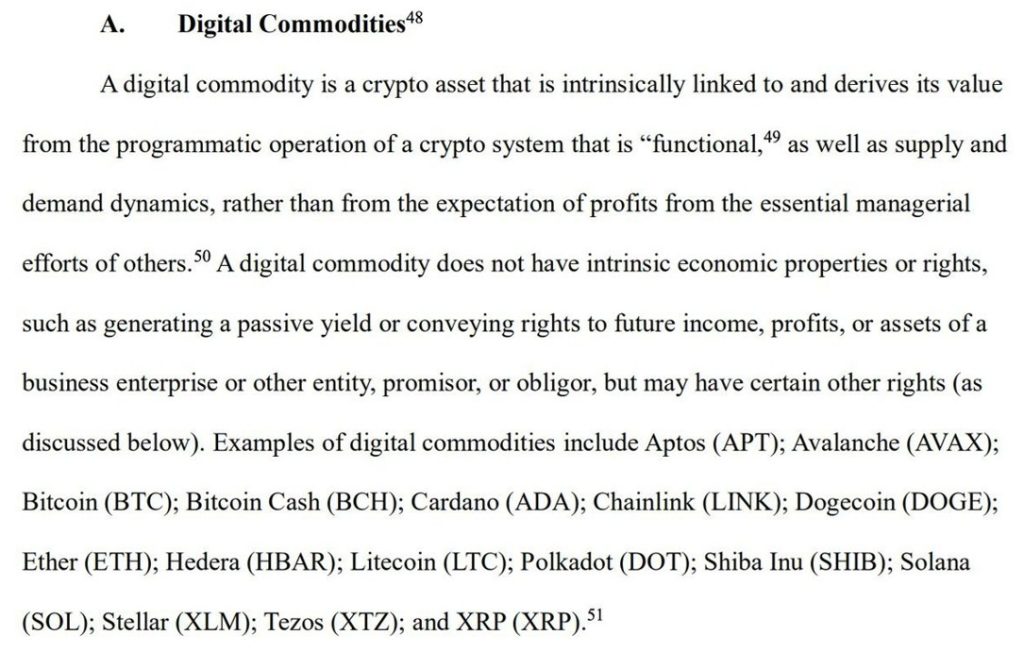

The SEC explicitly listed Bitcoin (BTC), Ethereum (ETH), XRP, and Dogecoin (DOGE) as flagship digital commodities, with Solana (SOL), Cardano (ADA), Bitcoin Cash (BCH), Aptos (APT), Avalanche (AVAX), Hedera (HBAR), Litecoin (LTC), Polkadot (DOT), Shiba Inu (SHIB), Stellar (XLM), Tezos (XTZ), and Chainlink (LINK) also named under this classification.

To qualify as a digital commodity, an asset must be “intrinsically linked to and derive its value from the programmatic operation of a crypto system that is functional,” driven by supply-and-demand dynamics and not by the managerial efforts of others.

One important caveat: classification as a digital commodity is not a permanent shield. These assets can become securities if an individual or group offers and sells them subject to an investment contract.

Staking, Mining, and Airdrops Are Cleared With Caveats

The SEC stated that some protocol mining, protocol staking, certain airdrops, and some wrapped non-security tokens do not involve securities transactions. For builders and DeFi protocols, this is meaningful clarity. These activities have sat in legal limbo for years.

Although lawmakers’ progress on the CLARITY Act has stalled in recent months, the SEC’s implementation shows that the regulator isn’t waiting for laws pertaining to the crypto market’s structure to be enacted before it establishes clearer rules for the industry. That’s a pragmatic move from Atkins, and arguably the right one.

One Framework, Two Agencies: What This Signals for 2026

This joint action follows an MOU signed earlier this month by the SEC and CFTC, cementing a coordinated approach to digital asset oversight. As former CFTC Chair J. Christopher Giancarlo stated at NABS25, the relationship between these two regulators is foundational to building a functional crypto market in the U.S.

Miller Whitehouse-Levine, founder and CEO of the Solana Policy Institute, called the interpretation “of profound importance, and what we’ve been asking for from the agency for 10 years before appealing to Congress.“

The taxonomy is still interpretive guidance, not statute. Congress could override it. And until the CLARITY Act, or something like it, passes the Senate, the legal architecture remains fragile. But right now, for the first time, the U.S. government has formally named which digital assets are commodities, who oversees what, and how the rules apply. A starting point the market has needed since 2013.

Author: Ayanfe Fakunle

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organizations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

How Paul Atkins as SEC Chairman Might Transform Crypto’s Legal Landscape | Disruption Banking