As Reddit commences trading on the New York Stock Exchange (NYSE) today, early signs point to potential volatility in its initial trading period. The IPO, which aims to raise up to $748 million, targeting a valuation of approximately $6.5 billion, has been oversubscribed by “as much as five times,” according to insiders who disclosed this to Reuters. This fervent investor interest, primarily from mutual funds, hedge funds, and other major investment groups that typically participate in IPOs, indicates a strong eagerness to secure shares at the IPO price range of $31 – $34.

While IPO oversubscription is not a definitive predictor of robust post-IPO performance, it does imply that Reddit’s bull case has found considerable support among market participants. So what is this bull case exactly – and more importantly – how does it compare with the bear case? It’s crucial for prudent investors to consider both sides of the coin, assessing not just the strengths but also the weaknesses of an investment thesis.

“Down Round” IPO Offers Margin Of Safety

One of the possible reasons why some investors are bullish on Reddit’s IPO is that its planned valuation of up to $6.4 billion represents a massive haircut from its previous valuation of $10 billion in 2021 when it raised $410 million from Fidelity Investments Inc in a private round. This essentially makes Reddit’s transaction a “down round IPO,” which simply means that the company is being sold to the public at a lower price than in previous private funding rounds. This could offer some margin of safety for investors who scoop up the shares at the IPO price.

This thesis, of course, rides on the assumption that Reddit’s previous valuation was a far more accurate reflection of the company’s fundamentals and potential than its IPO price. Whether this is the case, however, is debatable. It’s important to remember that in 2021 when Reddit raised capital from Fidelity, the broader market was significantly overpriced due to the post-coronavirus wave of monetary and fiscal stimulus. Market conditions right now are markedly different due to monetary tightening, so a case can be made that the drop in Reddit’s valuation doesn’t really offer a bargain but reflects a change in market conditions.

Strong Financial Performance

Another reason why Reddit’s IPO has whetted the appetite of bullish investors is its improving financial performance. While still a loss making entity, the social media platform’s losses have shrunk in the past two years while revenues have grown. According to its IPO prospectus, Reddit’s revenues grew from $666.70 million in 2022 to $804.02 million in 2023, while losses as represented by net income narrowed from -$158.55 million to -$90.82 million.

Reddit co-founder and Chief Executive Officer Steven Huffman said in a signed letter included in the filings that the company has many opportunities to grow both the platform and the business. “Advertising is our first business, and advertisers of all sizes have discovered that Reddit is a great place to find high-intent customers that they aren’t able to reach elsewhere,” he noted. “Advertising on Reddit is rapidly evolving, and we are still in the early phases of growing this business.”

Assuming the company’s future growth impresses analysts and investors, the stock could perform well post-IPO given the current trajectory in terms of its shrinking losses and growing revenue.

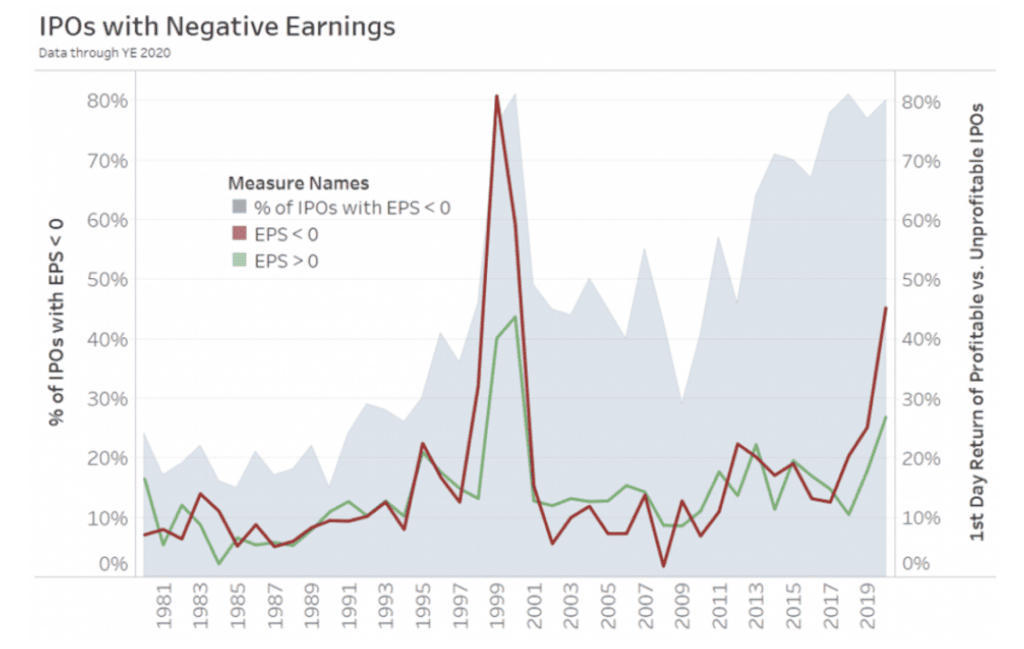

When it comes to the stock’s near-term performance, Reddit’s lack of profits is unlikely to be a factor that will influence returns in the first few days and weeks of trading. The lack of profits is surprisingly not a determinant of first day returns of IPOs in Wall Street. The average first-day return of unprofitable companies has on average exceeded the first-day return of profitable companies over the last 41 years, according to Nasdaq Economic Research.

Unprofitable IPOs outperform profitable ones on the 1st Day; Source: Nasdaq

Formidable Bear Case

Reddit’s bear case presents a significant challenge, particularly when assessing its ability to generate consistently strong advertising revenue. It significantly lags behind social media giants like Facebook and X (formerly Twitter). Founded in 2005, Reddit has a slight age advantage over Facebook and predates X by four years. Yet, despite its earlier start, Reddit’s commercial endeavors only began in earnest in 2018, a considerable time after its competitors had already surpassed the billion-dollar mark in annual ad revenues. To date, Reddit has not crossed the $1 billion threshold in yearly revenue.

“We did not begin meaningful monetisation efforts at Reddit until 2018, and we are currently exploring new strategies for monetisation. Our limited operating history may make it difficult to evaluate our current business and our future prospects,” the company notes in its prospectus.

Reddit’s business model faces a paradoxical challenge: its core value proposition of authenticity and human connection stands in stark contrast to the perceived artificiality of advertising, which currently forms the bulk of its revenue (98%).

Reddit’s ongoing push to diversify its revenue streams is both a strategic pivot and a timely endeavor. The company said it’s in the early stages of allowing third parties to license access to data on the platform, including to train artificial intelligence models. The company said that in January it entered into data licensing arrangements with an aggregate contract value of $203 million and terms ranging from two to three years. It expects a minimum of $66.4 million of revenue from those agreements this year, according to the filings. This move, coupled with a partnership with Google to enhance AI technologies using Reddit data, underscores the platform’s commitment to diversifying its sources of revenue.

Yet, the question looms: can these initiatives propel Reddit towards the coveted $1 billion revenue mark? The platform’s $6.5 billion IPO valuation (which works out to a price/sales multiple of more than six) seems lofty and suggests that risks to the downside for investors who buy-and-hold on the assumption that Reddit’s sales will grow on the diversification push.

Dangers Of Stock-Based Compensation

Another risk worth considering before buying into the Reddit IPO is the high level of executive compensation that saw the CEO Steven Huffman earn a staggering $193.24 million in 2023, $98.33 million of which was stock awards. The Prospectus further shows (page 170) that Jennifer Wong, the company’s chief operating officer took home $92.53 million in 2023, $45.69 million of which was stock awards.

There is nothing wrong with a management team getting well rewarded for outcomes that enhance shareholder value. However, shareholders should watch out if the company continues relying on stock awards to incentivize management, especially if there is no corresponding increase in shareholder value. Left unchecked, stock-based compensation dilutes existing shareholders by increasing the number of shares and puts downward pressure on the stock price by artificially lowering the earnings per share (EPS) figure.

Author: Acutel

We are global investors who invest in good companies at fair valuation and speculate on all else subject to the risk exposure we can afford.

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organisations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.