When it comes to business accounts, 53% of small and medium businesses (like us) have never changed their business banking provider. Is this a true reflection of the market though? Or has there been a change in customer sentiment? Our editorial team looks in to whether the Barclays business bank account is any good. Good for businesses and good for founders.

The Barclays website presents an enticing offer to small and medium companies. The bank offers them potential access to business finance by helping them build up credit history for their business. It also mentions how having a business account means that you can access features like the knowledge and support of business banking managers. Ones who can help you identify opportunities in the market and support your business growth.

Whilst the offer of supporting small businesses seems genuine, it’s probably a bit of over-promising and under-delivering. Take our business, registered as Digital StartUp Ltd on Companies House (because the FCA wouldn’t allow us to register Disruption Banking Ltd). How many times has the business banking team from Barclays reached out to discuss finance with our founders? Not as many times as the bank’s website would lead you to believe.

How easy is it to work with the Barclays business banking team?

You pay for it, so you expect to have access to it. Business accounts are not like current accounts, a bank like Barclays will charge £102 to businesses over a year for using a business account (after the first year). Banks like Barclays don’t demand your financial statement each year, they can probably get this from Companies House anyway. But what they should be doing is ensuring business bankers are reaching out to founders who hold business accounts with the bank. But do the business bankers at Barclays do this?

Long gone are the days when you could sit down face-to-face with a business banker at your local branch. And with that a sense of bewilderment and confusion has settled around the talk of business banking and the related support offered.

In almost six years of having a business account with Barclays there has only ever been two interactions between the business banking team and the founders of our newswire. The first, when the account was opened. This took place in early 2018 when there were still business bankers in branch to help with this.

The second, not so pleasant experience, was in November 2022 with a Business Lending Manager from the High Value and Regulated Lending Team of Barclays Business Banking. There looked like there was a third one coming up, but there were some restrictions involved which we will explain later.

Access to business finance with Barclays

The second contact with the Barclays business banking team was a short interaction. Our founders decided that with revenues rising it would be useful to apply for an overdraft. Seemed easy at first glance, but the forms added up. As did the amount of financial knowledge that the business banking team expected. And then you had to get through to the business banking team on the phone. No simple feat:

Once Barclays respond you are asked to send a completed form as a director. Similar to a mortgage application, but about your personal finances as a director. Then you have the ‘appointment’ with the business banking team. Who, in our case, had a full set of accounts on her screen ready to go through with our founders in fine detail. The company accountants would have been useful at this stage as we trade internationally, and we don’t have an easy set of accounts to review.

Inevitably our application was rejected. The accountants weren’t on the call, and there was no option to reschedule a call when they could join.

Startup. Nearing four years on the market. Mainly focused on client relationships. Break even. Probably another tick in the box. Business bankers move on. Who’s the next customer who wants something?

There has never been any follow-up. No help with identifying opportunities in the market or supporting our business growth. And one gets used to this. We accept that this as ‘normal’. Of course, one can be pro-active with the bank. There must be some business owners out there who speak to their Barclays business banker quite regularly. But there must also be a lot of business owners who don’t. Like us.

Was it because of something that we said?

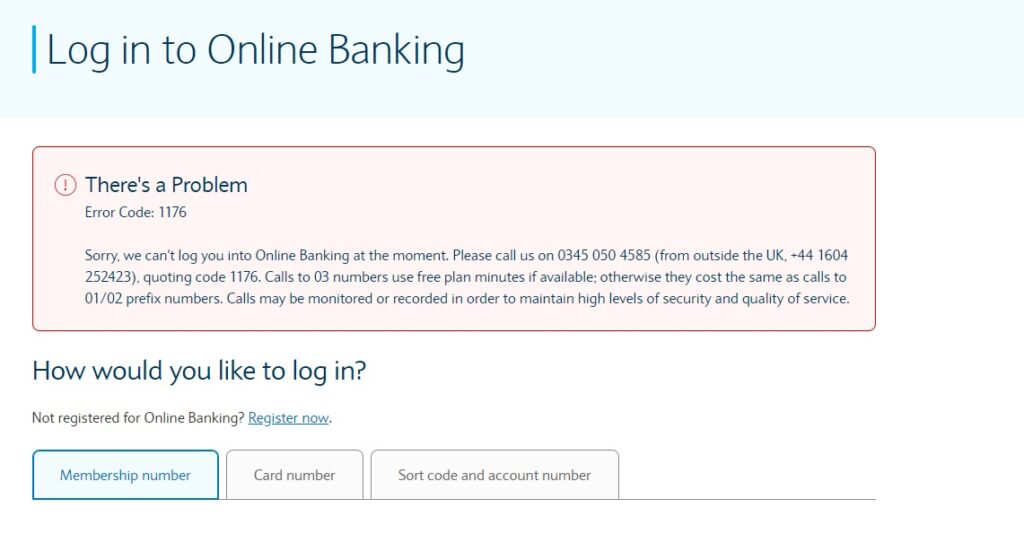

Something prompted this short review about whether the Barclays business bank account is any good. For a few days one of our founders had his access to the Barclays business bank account restricted. Turned off. Access denied. No call. No SMS. Just blocked. Maybe it was because of something that was published on the Disruption Banking site? That was the first thing that came to mind.

There was a story about Barclays in August:

Who knows? Maybe the PR team in a fit of rage had done a ‘Nigel Farage’ on our newswire? Maybe the journalist didn’t properly credit the story. It’s not as if these things don’t happen. All that we could see was the dreaded 1176 Error Code which meant that someone needed to call Barclays.

Lifting restrictions placed by mistake on a Barclays business account.

The restriction couldn’t be unblocked during the first call to Barclays. Unfortunately it was out of office hours and the business bankers could only be in touch after the long weekend (New Years). And the business banking team were needed to lift the restriction. Apparently.

No problem.

A call back was arranged for the 3rd of January, this week, where a 9am – 1pm time slot was offered by the Barclays social media team on X, formerly known as Twitter. There was a call, but it was missed, and no second attempt to call was made. The next message from Barclays was offering another 4-hour time slot for a call back. Probably on the next day.

Confused? So were we. Eventually we contacted Barclays on the same number as during the first call. After a lengthy phone interaction part of the restrictions have now been lifted. No need to speak to the business banking team this time.

Importantly. It wasn’t because of anything published on the website thankfully. It was some fraud issue that was causing problems with accounts of late.

However. The issue isn’t what happened in the case of our contact with Barclays. The issue here is one of time. An investment of time in the case of a startup. Time that would be better used to get the support and advice that the Barclays website so generously offers.

Are business bankers at banks like Barclays doing a good job?

In the case of our newswire, if Barclays do step up. If the banks’ offer of support and complaint resolution is successful, could it not be avoided? What does the average founder have to do to get better service? Or, God forbid, their bank account restrictions lifted…

According to Trustpilot, Barclays are just as bad as the other main banks with a score of 1.4 stars (out of 5). The bank scores better on the App Store and Google Play, but it is plagued with a bad customer service record. A record that doesn’t make Barclays customers readily want to interact with the bank’s customer service team.

And, when you call them up and one of the messages played to customers on hold states that bad behaviour to Barclays employees could lead to the call being disconnected. How it won’t be tolerated. It’s almost like they are expecting customers to contact the bank when things are not good.

Even should the powers that be at Barclays try to improve the standards needed to operate in the digital era, have they not forgotten one of the main things about banking? Trust. When you play with people’s bank accounts and provide them less than adequate customer service. Warn these people to behave on calls with bank employees. What do you think that says to potential new customers?

Is the Barclays business bank account any good? Probably not as good as it should be.

Author: Andy Samu

See Also:

Why is Barclays’ share price so low? | Disruption Banking

What do we know about the new CEO of Barclays? | Disruption Banking

One Response

Hello, and thank you for this article. It sums up most of our experiences with Barclays – but I wonder if you realise just how bad it actually is?

We are a community interest company providing fencing services (a sport, improving physical and mental balance). We are paid by subscriptions from our membership and rely on this to operate. When we opened our account with Barclays, they confused the company name with another and opened our bank account under another company. That company went into liquidation and Barclays shut down our account that they had opened in error, taking our assets with them.

That was in January. It is now March. We cannot get payments from our membership. We cannot pay our staff or invoices. This as raised with the business team who missed every callback they promised us. Again and again and again… Eventually it is referred to the complaints team, who lost the complaint. Barclays will not give us an email address to communicate with the complaints team. The complaints team will then inevitably tell us this has to go through the business team who promise another callback that never comes. All of this happens on the telephone, so there is no paper trail. I get constant emails that I need to read a new document or other on my account and need to log in to do so, but Barclays has shut that account and I cannot access it to read anything. Calling Barclays just results in another promised callback that never happens.

At the beginning of March we are finally contacted. But it is by the new business team. “We are pleased that you are interested in opening a new bank account with Barclays…”. This is with the full stack of documents to reapply for a new business account “Provide with full evidence. You cannot send this by email, it must be through the post. Fill out with ‘black’ ballpoint pen. We will contact you”. When I chased them back with my complaint number I got an automated response that I should receive a response maybe in four working days or so. When the human person finally deigned to get in touch it was with an air of disinterest, as she informed me that all forms must be completed and she has no truck with any other department – such as complaints.

During all of this time I am trying to keep my company afloat. I am paying bills out of my own pocket while subscriptions stack up in our payment portal (we cannot access these without a business account). We have initiated a new business account with ***** bank, but that process can take another month, and it is admitting the loss of all our existing assets held at Barclays.

I hope this gives some insight into the situation for some small businesses and possibly part of the cause for so many small business shut downs over the last couple of years.

Here are some links to news articles on Barclays and their behaviour to community or charity groups:

https://www.theguardian.com/money/2023/dec/09/charities-barclays-frozen-bank-accounts

https://www.thirdsector.co.uk/orchestra-charity-loses-staff-banking-difficulties/finance/article/1861852

https://www.thisismoney.co.uk/money/saving/article-12851267/Barclays-debanked-residents-associations-pay-bills-blocks-flats.html

https://www.thewestmorlandgazette.co.uk/news/23975187.cumbria-deaf-association-struggling-barclays-debanking-chaos/

https://www.thetimes.co.uk/article/big-demands-for-small-firms-from-overbearing-barclays-l09qfgx0r

I think we can safely say that Barclays has failed to achieve the ambition of it Chief Executive to be trusted by the public once again: https://www.bbc.co.uk/news/business-25549660