Given at Brunswick Group’s Cost of Living Conference, Coin Street, London

1 March 2023

The latest release of data for the UK consumer price index showed an annual increase of 10.1% in January. It is down from a peak of 11.1% in October, not least because direct effects from energy prices have eased. But also, core inflation, which excludes the most volatile components of the consumer price index, fell more than expected to 5.8% in January.

The Bank’s Monetary Policy Committee spends a lot of time poring over these data. Consumer price inflation remains much too high, and it is our job to bring it back down to our 2% target. That is why we have increased Bank Rate by nearly 4 percentage points over the past 15 months. To set the appropriate level of Bank Rate over the months ahead, we have to monitor our progress towards our target very carefully.

But the data can only tell us so much. At times like these, more than ever, it is important to hear the human stories behind the data. These stories help us understand both what is actually going on and the impact it has on people’s lives. The MPC’s inflation target sits within the Bank’s wider mission – set out in our founding charter from 1694 – to promote the good of the people of the United Kingdom. These are not just words from an old charter. It is the heart and soul of what we do.

It is therefore important to us to listen to what the people of the United Kingdom have to say. We of course also talk to financial market participants through our market intelligence gathering, and our Agents travel to all corners of the country. We join them regularly in this work. I personally go on visits to each of the 12 regions and nations of the UK at least once a year to hear from businesses and organisations first-hand.

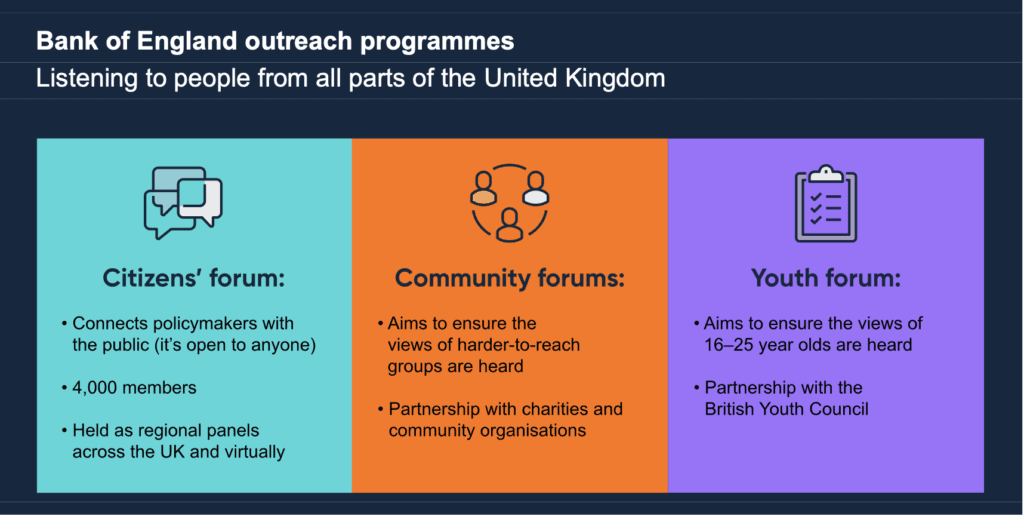

But today I would like to focus on our outreach programmes: our citizen’s forum consisting of 12 regional panels, each chaired by a devoted volunteer from the local community, and currently counting 4,000 members; our community forums for charities and the people they support; and our youth forum specifically for young people aged 16 to 25. These are the events where we talk with and listen to people from all walks of life. We set out some of the high-level themes from those conversations in a report from the chairs of the regional panels published today.

What we hear from them is sobering. At a recent citizens’ panel in Leeds, for example, a young woman shared her story of trying to juggle studies with caring responsibilities for her parents. Higher costs of transport, food and heating had left her struggling to cope, let alone to make the most of her time at university. In Manchester, a carer told us how higher fuel prices had eaten into her pay as she relied on private transport to deliver vital services to vulnerable people. A woman at our panel in Durham told us how she received her pay on a weekly basis and struggled to budget for her monthly direct debits. Although she had health concerns, she felt unable financially to take time off from her full-time work. She told us she had cut back on all but the most essential purchases. We hear many such stories. For many people, this really is a cost of living crisis.

Let me provide some wider context.

The UK economy has been hit by a series of significant economic shocks. These include the change in our trading relationship with the European Union, the Covid pandemic with associated bottlenecks in global supply chains, and the sharp rise in global energy prices related to Russia’s brutal war on Ukraine and its people.

For the United Kingdom, these shocks have eroded the terms on which we trade with the outside world. The prices we can get for the goods we sell have not kept up with the prices we have to pay for the goods we buy. This has made us poorer as a country. The fall in our national real income has manifested itself in a rise in the prices we have to pay for the things we buy as consumers.

The developments in energy prices have been particularly stark. The impact of that is very clear in the data so forgive me for spending a bit of time setting that out too.

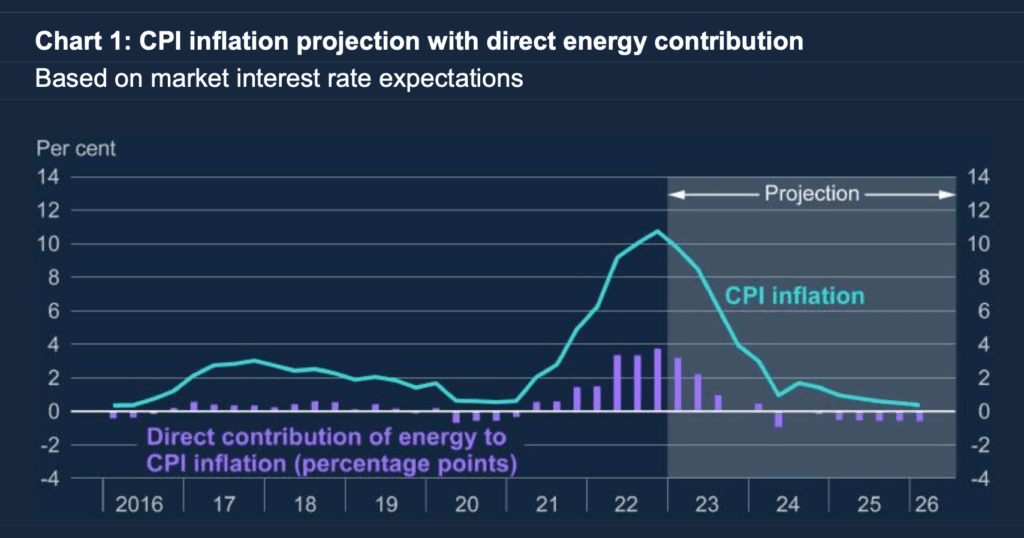

The purple bars on this chart show that a big part of the rise in consumer price inflation has been caused directly by energy prices. But the chart also shows the almost mechanical flipside of that. In the MPC’s central projection, inflation falls quite sharply over 2023 as last year’s large increases in energy prices drop out of the annual calculation.

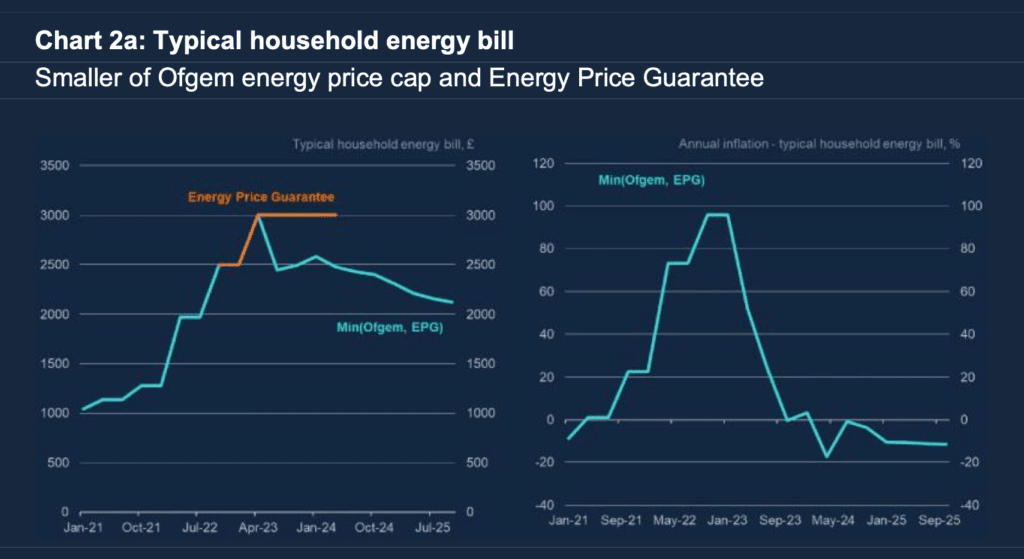

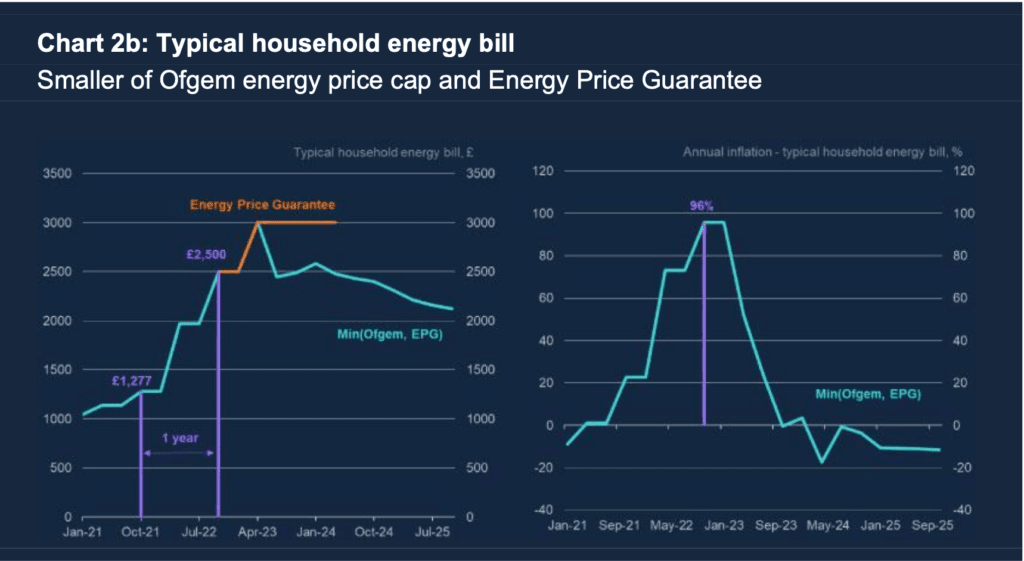

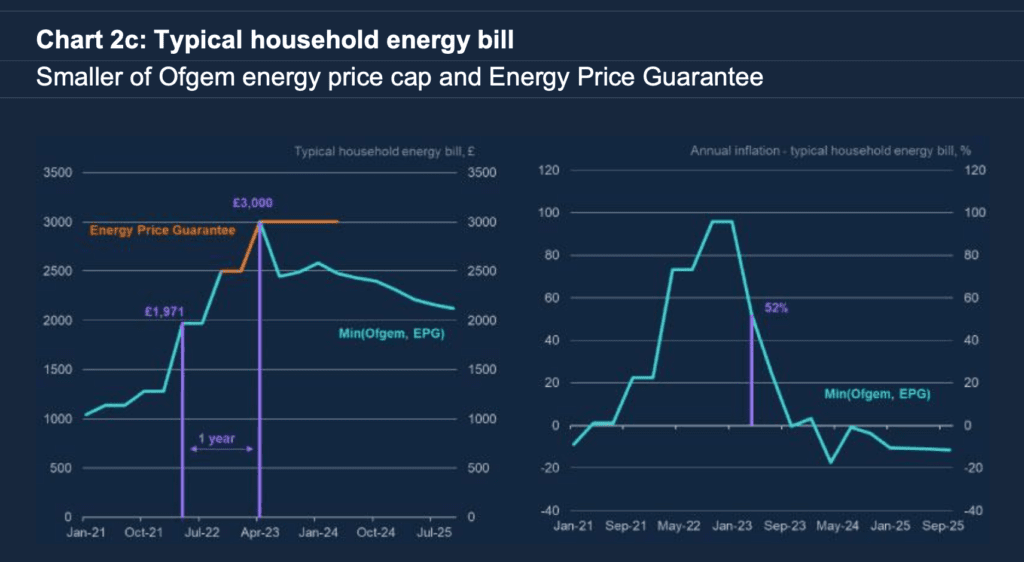

This next chart illustrates what is going on. The blue line on the left-hand chart shows the evolution of the ‘typical’ household energy bill. Nobody actually pays the typical energy price bill, of course, but it has become an industry standard as a measure of what households pay on average. It is generally determined by Ofgem’s cap on the price that energy suppliers can charge consumers. In turn, Ofgem bases its calculation of the cap on the wholesale prices energy suppliers are expected to pay in European energy markets. Since October, the cap has itself been capped by the Government’s Energy Price Guarantee (shown in orange).

You can see that the typical energy price bill went up in a few big strides as Russia’s assault on Ukraine drove up wholesale energy prices. In October, as the Energy Price Guarantee was put in place to moderate what would have been an even higher increase in Ofgem’s price cap, the typical energy price bill was nearly twice as high as a year earlier. As shown in the right-hand chart, annual inflation in the typical household bill was nearly 100%. Even if electricity and gas only accounted for about 31⁄2 per cent of the consumer price index, this increase had a big impact on the overall inflation rate: a 100% price increase in 31⁄2 per cent of the consumption basket adds 31⁄2 percentage points to inflation.

Looking ahead, with the announced adjustment to the Energy Price Guarantee, the typical energy price bill is set to rise further to £3,000 in April. But to calculate the annual inflation rate at that point, we have to compare with the April 2022 bill, which had already risen significantly. Because of this base effect, even if the bill itself goes up to a higher level, it goes up by less over a year than it did in October. The annual inflation rate therefore falls sharply from 96% to 52%. The contribution to consumer price inflation from the energy bill will nearly halve.