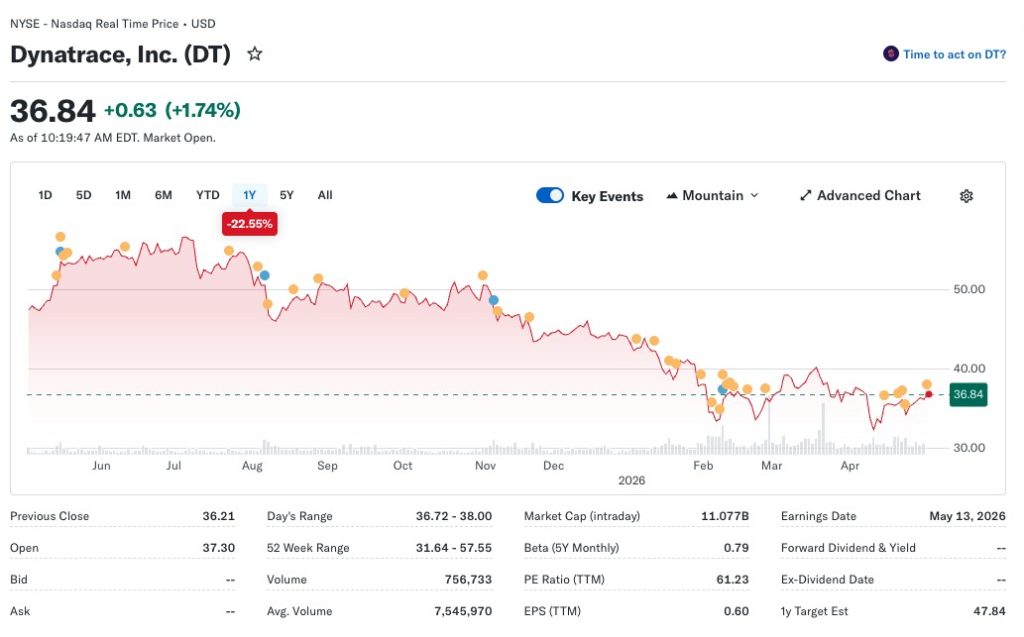

Activist investor Starboard Value piled into Dynatrace (DT), an AI software company, causing the DT stock to surge 8% in after-hours trading on a day when the S&P lost 0.49%. Starboard is looking forward to “an AI-enabled world” and is bullish on the prospects of Dynatrace in that future, despite the market’s recent sell-off of software stocks.

Dynatrace is an AI-powered software platform that monitors and automates a company’s digital operations with a market value of about $10.6 to $11 billion.. The idea is to use AI as the brain to run an enterprise as much as possible. It is how enterprises see, understand, and fix complex distributed systems. Perhaps in the future, an entire enterprise can be run by AI itself. Maybe the next victims of AI layoffs will be CEOs!

Peter Feld, managing member of Starboard, held talks with Dynatrace leadership. Starboard delivered a letter last week, after building a stake privately in recent months. It is now a top-five holder, size undisclosed.

Why the Market Has Dynatrace Stock Completely Backwards

In the letter, Feld cited slow growth and investor doubts about the company for a 15% decline in the stock’s value during 2025 and another 17% lost so far this year. Dynatrace acknowledged the letter and said it had “introductory meetings” and will continue to engage.

Feld writes, “Investors have incorrectly bucketed Dynatrace with companies exposed to AI-related risks.”

Feld called for the board to accept all paths to maximizing shareholder value, pushing share buybacks in particular. That part seemed slightly coercive. That line probably jumped out at Dynatrace management.

This is not Starboard’s first investment in this sector; the last one, Splunk, ended up with Cisco purchasing the company outright. Cisco closed a $28 billion deal for Splunk in early 2024, where Starboard was also an investor. This was a big win for Starboard and adds to their credibility with Dynatrace.

This Setup Looks Familiar

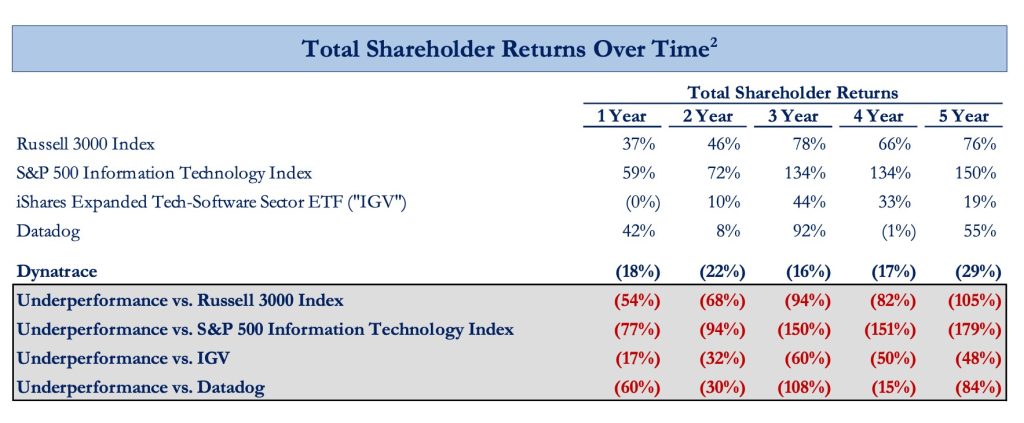

Revenue projections for Dynatrace are expected to exceed 18% year-on-year, and Starboard forecasts that Dynatrace could return $2.5 billion within three years. Despite these rosy predictions, the company has significantly underperformed in terms of shareholder returns, even though it has prominent visibility and attractive positioning in the sector, according to Starboard’s letter.

Its stock has performed poorly, including against its top competitor, Datadog, as well as the wider industry. Datadog trades at roughly 9 times forward sales versus about 5 times for Dynatrace, based on each company’s FY2026 guidance and late-April market caps. The efficiency gap is just as stark: Dynatrace spent 47% of 2025 revenue on SG&A compared with 36% at Datadog, an 11-point difference that Starboard says can be narrowed by at least $75 million annually.

Why the AI Trade Misprices Dynatrace

The reason for that can be explained by a number of explanations. Starboard suggests ultimately that the AI “gold rush” does not understand the Dynatrace thesis simply because it is too focused on seeing “AI disruption” rather than “AI adaptation.”

What Starboard is really forcing into the open is a broader mispricing across the enterprise software stack—one that extends beyond Dynatrace itself. The current market narrative has been dominated by the idea that generative AI, particularly large language models, will compress the value of traditional software layers.

With banks pivoting toward AI-driven architectures, the complexity of their digital stacks increases exponentially, and with it, the potential for catastrophic failure. In an age where a microsecond of downtime in high-frequency trading systems or a glitch in a flagship mobile banking app translates directly into lost capital and eroded consumer trust, the stakes are high. This is where Dynatrace positions itself as more than just a software vendor.

DT serves as an indispensable infrastructure layer, providing the real-time visibility required to manage the inherent “chaos factor” of modern fintech (and other enterprises). For an industry where “always-on” is the only acceptable modus operandi, Starboard’s bet on Dynatrace is effectively a bet on the very scaffolding.

AI Makes Dynatrace More Essential

As enterprises move from static software environments to dynamic, AI-driven architectures, the number of variables increases exponentially. Autonomous agents, real-time inference, multi-cloud deployments, and API sprawl all introduce new points of failure.

The result is controlled chaos. And chaos, in enterprise environments, demands visibility, traceability, and automated remediation, often in real-time. That is exactly the layer Dynatrace is operating in, and why Starboard is pushing back so forcefully against the “AI disruption” narrative.

This is where the activist’s argument becomes more strategic than financial. By positioning Dynatrace as infrastructure rather than application software, Feld is effectively reframing how the company should be valued.

Why Dynatrace Deserves Premium AI Valuation

Infrastructure layers like cloud, cybersecurity, and data pipelines tend to command premium multiples because they are deeply embedded and difficult to rip out.

If Dynatrace can successfully anchor itself in that category, the persistent valuation discount highlighted by Starboard evaporates.

There is also a second-order effect that the market may be underestimating: AI increases the cost of downtime. When systems are partially autonomous, failures are decision-level failures. An AI agent making incorrect calls because of degraded system performance introduces compounding risk.

That raises the stakes for real-time observability and automated correction, a point that has been increasingly emphasized across enterprise AI coverage in the financial press.

In that context, the comparison to Datadog becomes more than just a margin benchmark—it becomes a narrative benchmark. Datadog positioned itself cleanly as a core observability layer, and the market has rewarded that clarity. Starboard’s push for Dynatrace to close its sales and marketing efficiency gap echoes similar arguments being made in public investor discussions, particularly around the roughly 10 percentage point delta in S&M spend.

Another angle worth watching is capital allocation discipline. The proposed $2.5 billion buyback is a signal. At current valuation levels, aggressive repurchases would effectively allow Dynatrace to arbitrage its own mispricing.

Starboard’s Playbook: Buybacks for Dynatrace

This is classic activist playbook, and one that has precedent. As the Wall Street Journal noted in its comparison to Starboard’s earlier Splunk position, disciplined capital allocation combined with strategic pressure can materially shift outcomes for observability platforms.

There is, of course, a risk that Starboard’s thesis runs ahead of reality. Enterprise AI adoption remains uneven, with many organizations still in pilot phases rather than full-scale deployment. Reuters made the case that while investor enthusiasm around AI remains strong, execution timelines across enterprise software are still extending, particularly in a tighter macro environment.

That tension is visible in the muted retail reaction. While institutional investors moved quickly on the news, broader market sentiment remains cautious. Still, the strategic logic underpinning Starboard’s move is difficult to ignore.

Why the Market Misses Dynatrace’s AI Opportunity

The enterprise stack is being rebuilt in real time, and companies that can position themselves as indispensable layers within that stack stand to benefit disproportionately, just as Oracle did in decades past. Observability, particularly when fused with AI-driven automation, sits close to the center of that rebuild.

If Dynatrace can tighten its operating model, sharpen its narrative, and align capital allocation with its long-term positioning, the current valuation gap may start to close. And if the Splunk playbook is any indication, Starboard is unlikely to wait patiently for the market to figure that out on its own.

Author: Tim Tolka, Senior Reporter

#Crypto #Blockchain #DigitalAssets #DeFi

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organizations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

Why is XRP Price $1.39 Despite the Bullish Las Vegas Billboards? | Disruption Banking

CLARITY Act Stalls as Trump’s Memecoin Crashes 14% After Mar-a-Lago Gala | Disruption Banking