Copper doesn’t lie. It never has. It was called “Dr. Copper” for a reason. The metal has a track record of signaling where the global economy is heading before most analysts catch up. In 2026, it’s telling us something loud and clear: the world is running short of one of its most critical raw materials, and the pressure is building.

Copper Prices Surge to Record $14,527.50 per Metric Ton

Copper prices on the London Metals Exchange rallied 22% from under $11,000 per ton at the close of November to a record high of $13,387 on January 6. Then it kept going. Prices surged to a record $14,527.50 per metric ton on January 29, a level that, not long ago, would have seemed like analyst fantasy.

What makes this remarkable isn’t just the number. It’s the breadth of forces pushing it there at once.

Three Key Drivers Fueling the 2026 Copper Surge

The first is supply. A fatal mudslide at Freeport-McMoRan’s Grasberg mine in Indonesia, the world’s second-largest copper mine, triggered a force majeure, with the Grasberg Block Cave portion expected to remain closed until the second quarter of 2026 while other parts of the mine have restarted production. That’s 800,000 metric tons of wet material pouring into the primary shaft. Meanwhile, Chile, the world’s top copper producer, accounting for 25% of global supply, saw persistent declines in late 2025. Anglo American cut its 2026 production forecast to 700,000–760,000 tons in February, down from earlier guidance of 760,000–820,000.

The second driver is structural demand. As we covered extensively during our AI infrastructure reporting, data centers are no longer a footnote in commodity markets; they’re a headline. Data center demand could translate into approximately 475,000 metric tons of copper demand in 2026, up by roughly 110,000 metric tons versus the prior year,per J.P. Morgan.

Add electric vehicles, which require three to four times more copper than combustion-engine vehicles, along with grid upgrades, and you have a demand cocktail that miners cannot easily match. Goldman Sachs notes that grid and other power infrastructure are projected to drive more than 60% of copper demand growth until 2030.

The third driver is trade policy. The US Commerce Secretary is due to deliver a copper market report to the White House by June 2026, ahead of a proposed 15% tariff slated to begin in January 2027, rising to 30% from January 2028. Traders aren’t waiting. CME warehouse totals rose to over 453,000 tons, a record high compared to the previous peak of nearly 360,000 tons set in January 2003. That stockpiling is distorting price signals globally.

Analyst Forecasts: Bullish Consensus but Tempered Expectations

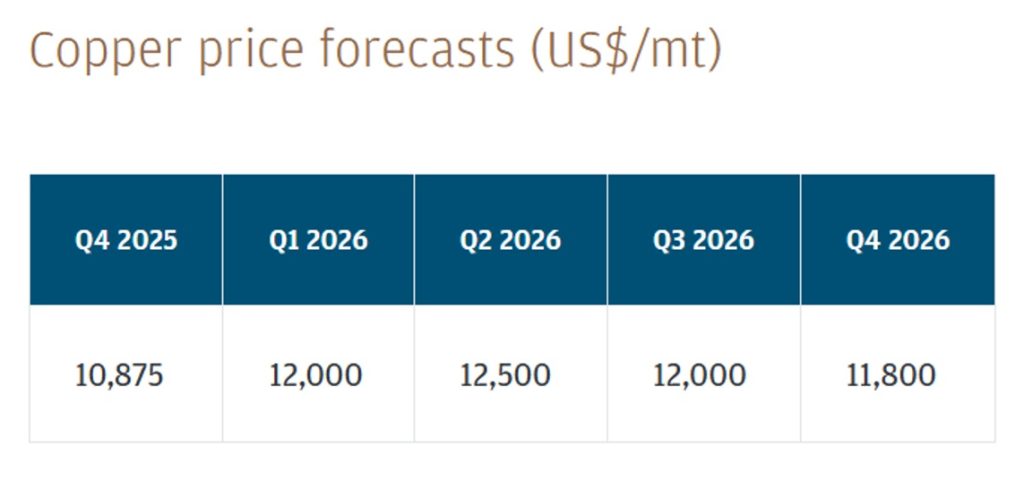

A Reuters poll of 31 analysts published January 29 placed the median 2026 copper price forecast at $11,975 per tonne, below recent peaks, but the highest consensus forecast ever recorded.

J.P. Morgan is more bullish, projecting copper could reach $12,500 per metric ton in Q2 2026, with a full-year average near $12,075. Goldman Sachs, meanwhile, expects the rally to fade once tariff uncertainty resolves, pointing to a 300,000-kilotonne global surplus in 2026, the largest since 2009.Bank of America lands somewhere in between at approximately $11,313 per tonne.

Structural Deficit vs. Surplus Risks: The Real Tension in 2026

Where is the tension? the International Copper Study Group forecasts refined copper use to grow 2.1% to 28.73 million metric tons in 2026, outpacing production growth and leading to a 150,000 MT deficit. That’s structurally bullish.

But one analyst cautioned that mining companies have been so effective at promoting the idea of a looming deficit that investors and traders have prematurely priced in future shortages. “Mining companies are pushing a compelling long-term shortage narrative, and the market believes it. But belief and fundamentals aren’t the same thing.”

The Bottom Line: Strong Structural Case, But 2026 Will Test Patience

BloombergNEF’s Transition Metals Outlook warns copper demand for the energy transition could triple by 2045, and the metal may enter a structural deficit as early as 2026.

The long-term structural case is real. But 2026 will test patience. US tariff decisions, Chinese demand swings, and a surplus that’s larger than most anticipated are all live variables.

As we’ve noted in our AI in Finance coverage, the infrastructure buildout driving copper demand is real and accelerating. But markets move faster than mines. The copper story in 2026 is strong, just don’t expect it to be smooth.

Author: Ayanfe Fakunle

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organizations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

The Great Silver Crash 2026 and the Alleged Paper Reset | Disruption Banking