While the war in Iran has caused shortages and price spikes in Liquefied Natural Gas (LNG), it has not had a significant effect on Bitcoin mining operations. Only 8–10% of global hashrate sits in crude-linked electricity markets. Part of this is due to the world’s move towards renewables, and part of this is the digital mining industry trying to minimize cost.

Since its halving, Bitcoin has become more expensive to mine. It costs, on average, $87k to mine a single Bitcoin. The conflict in Iran has only further encouraged miners to move away from LNG-dependent markets.

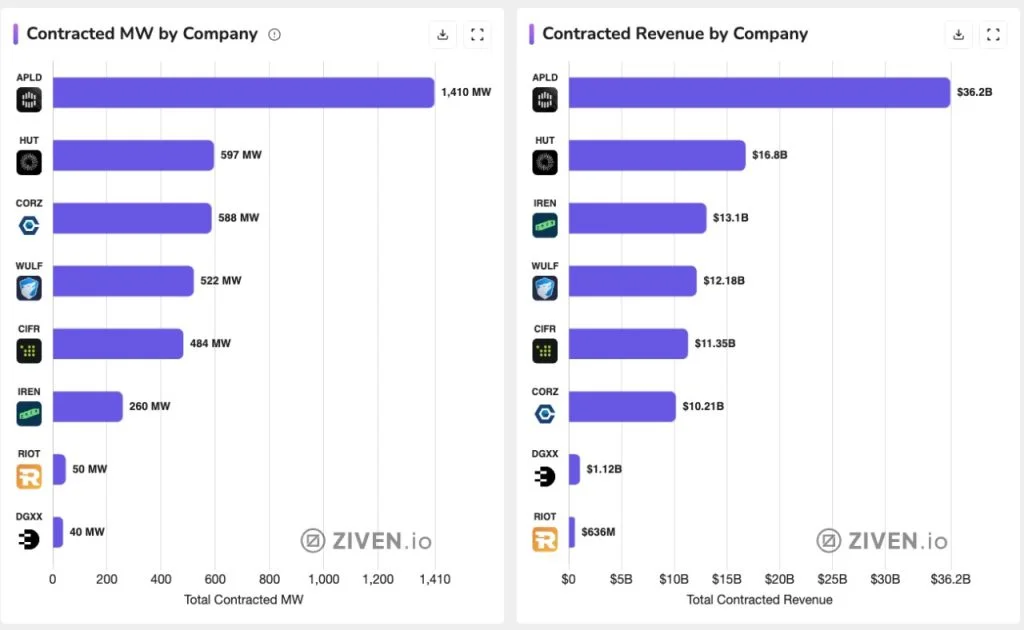

Given the location-agnostic aspect of mining operations, miners are migrating toward cheap gas and stranded renewables. Meanwhile, AI firms are locking in 20-year PPAs, and the two industries are fusing at the infrastructure layer. Companies like Applied Digital (APLD), which has now crossed 1.2 GW of contracted net IT load, Core Scientific (CORZ), IREN, and Hut 8 exemplify this shift; each has pivoted significant capacity toward high-performance computing and AI data center hosting, blurring the line between Bitcoin miner and infrastructure operator.

What the Numbers Say

In April 2025, the University of Cambridge released a report in which they surveyed a large swath of mining firms, finding that 52.4% of bitcoin miners got their electricity from non-fossil fuel sources. Renewables accounted for the largest share of that percentage at 42.6% of the total (hydropower at 23.4%, wind at 15.4%, solar at 3.2%, and other renewables at .5%). Nuclear accounted for 9.8%.

Europe depends mostly on renewables and natural gas. Asia relies predominantly on coal. The United States relies on a combination of sources, but leans heavily on its own natural gas production.

Fossil fuel-linked energy made up the remaining 47.6%, with natural gas leading all sources (38.2%), followed by coal (8.9%) and oil (0.5%).

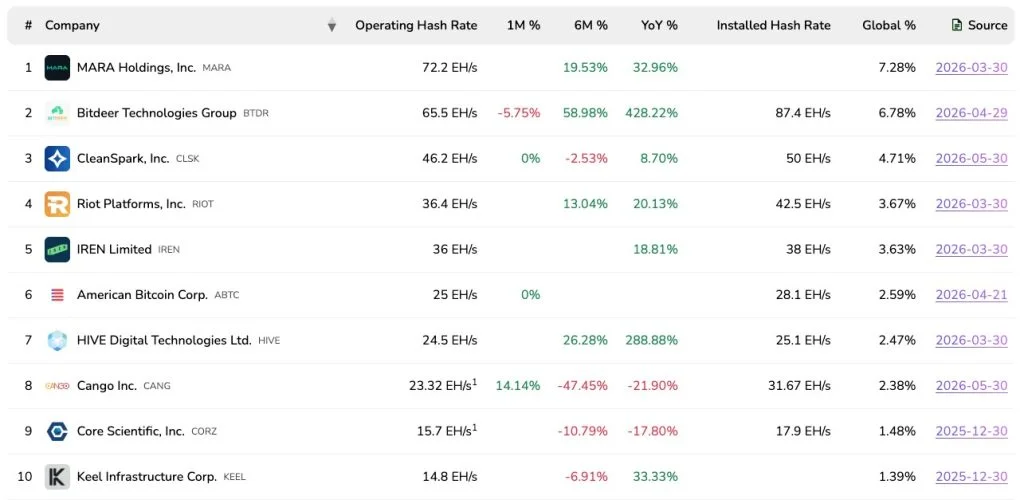

The largest U.S. public miners reflect this energy diversification. Marathon Holdings (MARA), which Disruption Banking wrote about here, one of the industry’s hashrate leaders at over 66 EH/s, has pursued a geographically diversified portfolio including flared gas projects. Bitdeer has the top spot, reporting 87.4 EH/s hash rate under management. CleanSpark (CLSK), which hit 50 EH/s entirely on American infrastructure, has secured low-cost power deals in Georgia and Wyoming with an emphasis on sustainable sourcing.

Riot Platforms (RIOT), operating out of Rockdale, Texas, remains one of the more prominent pure-play miners, participating in demand-response programs that benefit from cheap, curtailed renewable energy. Disruption Banking reported on its data center hedging strategy here.

TeraWulf (WULF), which Disruption Banking covered here, and Cipher Mining (CIFR), which Disruption Banking wrote about here, round out the mid-tier, with 522 MW and 484 MW of contracted capacity respectively, both heavily weighted toward nuclear and low-carbon power sources.

A Tale of Two Grids

While the world is experiencing energy shocks from the closure of the Strait of Hormuz, Bitcoin miners in the United States have been insulated due to America’s abundant natural gas. While price spikes elsewhere have created a stronger demand for American natural gas, prices have not exploded stateside yet.

Bitcoin mining is heavily concentrated in Russia as well, which has its own abundant supply of natural gas. China and Asia, however, are partially reliant on natural gas imports for electricity. While coal-powered electricity accounts for approximately 60% of electricity in Asia, natural gas accounts for 17%.

In the Middle East, Bitcoin miners in countries like Iran and Kuwait are reliant on natural gas-powered electricity, which is heavily subsidized, making mining cheaper than almost anywhere on the planet. Europe, while reliant on LNG from the Middle East, isn’t a huge Bitcoin mining hub.

Getting It From the Source

Mining operations are increasingly finding their own power, moving to off-grid sources. According to the Cambridge report:

“Industry stakeholders attribute this potential shift to the flexible, location-agnostic nature of digital mining, which uniquely positions miners to act as buyers of first and last resort. In practical terms, this flexibility allows miners to tap into otherwise stranded energy, absorb temporal oversupply of electricity from VREs, or utilise fossil fuel by-products such as flared natural gas.”

When oil is extracted, a combination of gases escapes, which have traditionally been burned to avoid dangerous pressure buildup. Unlike natural gas operations, there aren’t pipelines or economical ways to extract the gas.

That’s where Bitcoin miners have come in. Utilizing generators that convert the flared gas into electricity, mobile mining units tap into the byproduct on the cheap. While flared natural gas only accounts for 1% of Bitcoin mining, it is growing at wellheads in the Permian and Bakken. Marathon Holdings has been among the miners experimenting with flared gas capture at oil fields, deploying mobile units that convert what would otherwise be wasted emissions into mining revenue.

From Waste to Watt

Other operations are tapping into solar and localized hydropower. In Africa, a company called Gridless has set up mobile bitcoin miners near remote hydropower plants. The power plants often create more power than the local community needs. Bitcoin miners tapping into the system help subsidize these plants, which otherwise might not be sustainable.

Like flared gas and solar mining operations, these miners account for only a small slice of the pie, but their numbers are growing. Miners relying on curtailed renewables, i.e., temporary oversupplies of electricity that strain the grid, are also growing.

In West Texas, ERCOT curtailment data shows a meaningful reduction in grid areas where large mining operations have been established. Riot Platforms’ Rockdale facility is a prime example. The company has repeatedly curtailed its own operations during peak demand periods, selling power back to the grid and collecting demand-response credits.

Because miners can turn on and off quickly, they are effective at utilizing temporary gluts of energy provided by wind power and other renewables.

The Peace Deal Paradox

Reports of a U.S.-Iran peace agreement have already sent oil prices down more than 20% from their 2026 peak. Ceasefire talks briefly reopened the Strait of Hormuz. A lasting deal would push prices lower still.

For Bitcoin miners, this creates a strange situation.

The conflict never meaningfully raised their electricity costs. Their diversified energy mix, heavy on renewables and domestic natural gas, insulated them from LNG price spikes. But the war hurt them anyway. Inflation above 4% kept the Federal Reserve from cutting rates. Tighter money meant less capital flowing into crypto. Bitcoin dropped from over $120,000 in early 2025 to around $62,000 today.

A peace deal reverses that chain. Cheaper oil eases inflation. Easing inflation opens the door to rate cuts. Rate cuts loosen the money supply. Looser money tends to find its way into Bitcoin.

The miners who never needed relief from the energy shock are now positioned to benefit most from its removal, not through lower electricity bills, but through a recovering BTC price. For companies like Marathon Holdings, Riot Platforms, and CleanSpark, which are currently mining at a loss relative to spot price, even a modest BTC recovery changes the math significantly.

The conflict hurt miners through the one channel they weren’t exposed to. A peace deal heals them through that same channel.

Macroeconomic Conditions

While Bitcoin miners are largely insulated from oil price shocks regarding electricity, the indirect effects are being felt and could increase into 2026. Inflation in the US recently broke above 4% due to the Iran war.

Bitcoin is hovering around $62,000, half of what it was worth in early 2025. Crypto, in general, benefits from ample liquidity in the space. Moreover, investment flows more freely with lower rates. However, with inflation rearing its ugly head again, it’s unlikely the Federal Reserve will lower rates, which means a tighter money supply.

The average cost to mine Bitcoin is currently well above its market price. Like any commodity, investors expect a rebound, but with capital scarce and macroeconomic uncertainty looming, less money is flowing into the space.

Enter Trump

On June 14, Trump announced a deal with Iran. Reading deeper, it’s actually a deal to make a deal, which is probably more tenuous than Trump portrayed. He also called on oil tankers to begin crossing the Strait of Hormuz.

Every single time Trump has made this declaration before, it was obviously untrue, and most people took the American President’s words about as seriously as one takes a child who is explaining that he isn’t the one who broke the window.

This time, however, there is a date, a location, and a mediator. The signing ceremony is scheduled for June 19 in Switzerland.

If it holds, which is probably the biggest, most dubious “if” in recorded history, the chain reaction should be straightforward: oil prices fall, inflation cools, the Fed gets room to cut, and liquidity returns to risk assets. Bitcoin would likely be among the first beneficiaries.

The miners who survived the war without much damage to their electricity costs may end up being the ones most transformed by the peace.

Author: Tim Tolka, Senior Reporter

#Crypto #Blockchain #DigitalAssets #DeFi

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organizations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

Why IREN is Shifting Away from Bitcoin Mining to Data Centers | Disruption Banking

Why Riot Platforms is Focusing on Data Centers, and not just Bitcoin | Disruption Banking