At last year’s Point Zero Forum, Sergey Nazarov, co-founder of Chainlink, was arguably the most influential crypto leader at the event. This year there were …

There is a danger that Binance, and other cryptoexchanges, are selling crypto as the solution to all the world’s ills – in the case of Africa, the nightmare of persistently high inflation, poor wages, and in some cases, poverty. The glamour of elite football is making such products all the more appealing, and helping cover over many of the risks.

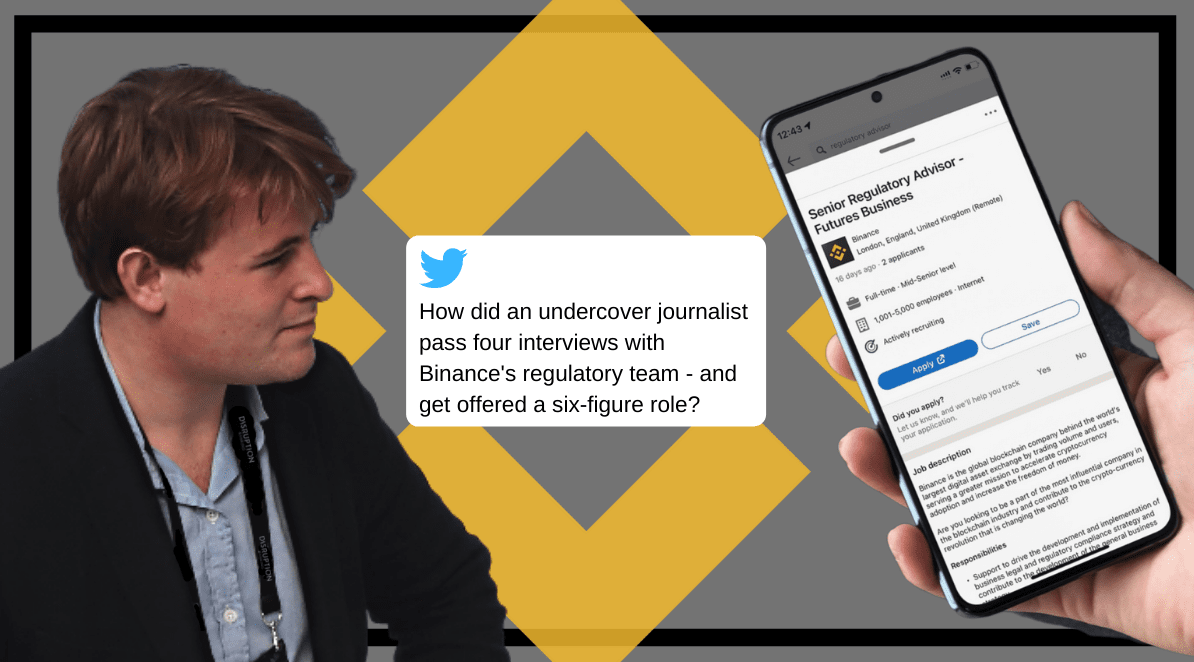

Is Binance serious about becoming “even more compliant?” Or are they simply seeking to hire a couple of people who appear to be experts, just so they can say to the regulators that they have? The company might make grand announcements about doubling its number of compliance staff, but that does not mean much if this is how they are going about their recruitment.

I was keen to investigate how serious Binance really was about cleaning up their act, and how robust the compliance recruitment processes of the world’s biggest cryptoexchange are. So I decided to apply for the role under a fake name and with false credentials.

I was keen to investigate how serious Binance really was about cleaning up their act, and how robust the compliance recruitment processes of the world’s biggest cryptoexchange are. So I decided to apply for the role under a fake name and with false credentials.

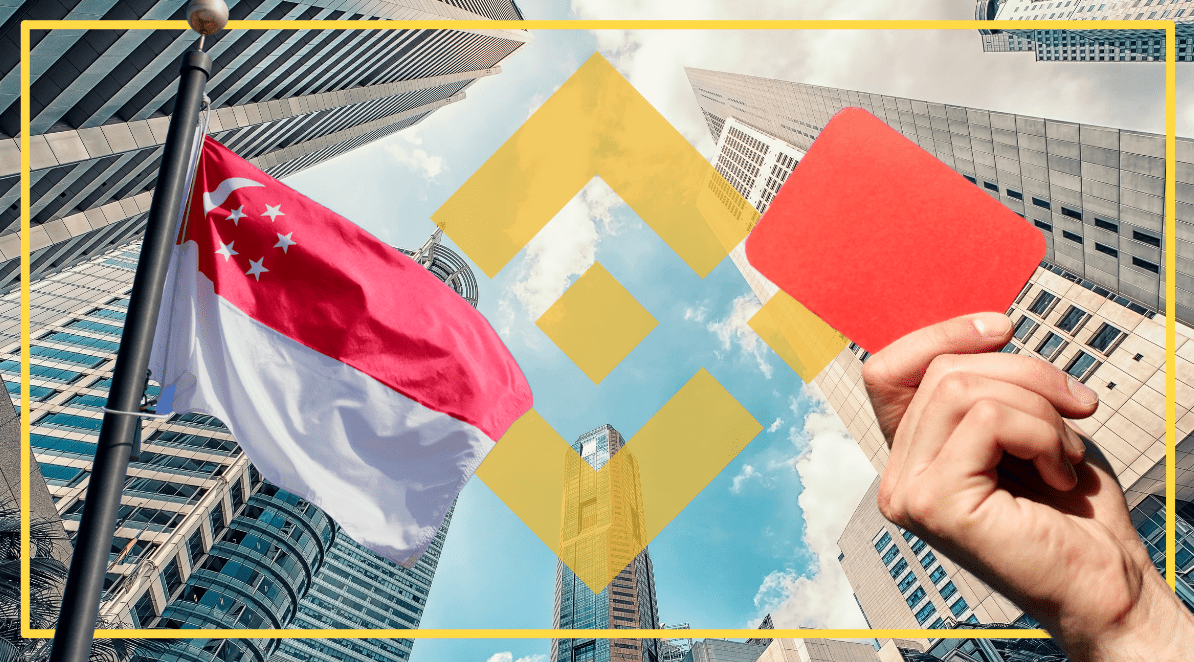

Earlier in December we heard the news that Binance had withdrawn its application to obtain a cryptoexchange licence in Singapore. This followed frequent clashes with the regulator in Singapore, which in September prompted Binance to ban its users in the country from trading on its global platform.

Just as Reddit users drove prices of GameStop and Robinhood stock, the same is the case in crypto. Today, Matt Damon is the face of Crypto.com. Not to mention Kim Kardashian…

Binance is facing a class action lawsuit in Illinois, which alleges that the world’s largest cryptoexchange has unlawfully collected its users’ biometric data.

Liti Capital SA, a Swiss blockchain-based litigation funding provider, says the Binance Claim group has received more than 1,000 claims against Binance in the last week alone, following the Binance outages of May 19.

Sign up for our free newsletter and receive the latest banking and fintech stories, straight to your inbox - every week

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkPrivacy policy