Part One of a Three Part Series (links at bottom)

In Puerto Rico, Hurricane Fiona has left 1.5 million people without power or water and has been linked with 25 deaths. Five years since Hurricane Maria, the island territory has struggled to keep the power on and become a cautionary tale of the critical need for energy resilience in the age of climate catastrophe.

After Hurricane Fiona, a multinational team of electrical engineers from LUMA Energy, a joint U.S./Canadian venture, huddled in a stuffy office trying to bring power back online as they have multiple times this year when massive apagones, or blackouts struck.

Since taking over the power system in Puerto Rico in June, 2021, LUMA’s executives have been publicly reviled, threatened with arrest, and hauled in to testify before Puerto Rican politicians who insisted on reading them Miranda rights.

Protests at LUMA’s San Juan office are a daily occurrence. Protesters shout “Fuera LUMA!” or “LUMA get out!” As evidence of the frequent power outages, rotten food that has spoiled in the protesters’ refrigerators is left outside the office.

If LUMA accomplishes its goal to create a smart grid that will rely on decentralized power distribution and mix renewable and fossil fuel energy, it will be a Harvard Business School case study for the ages because Puerto Rico’s power grid has never recovered from the Category 4 Hurricane Maria in 2017.

Nearly 3,000 Puerto Ricans died due to Hurricane Maria, and island residents continue to pay exorbitant fees for power and frequently go without, which makes running any kind of business difficult, resulting in a loss of 12% of Puerto Rico’s population in the last decade. Local residents spend 8% of their income on electricity, more than 300% higher than the U.S. average. The cost doubled just in the last two years.

So, who is responsible for Puerto Rico’s shocking loss of life from natural disasters, the increasingly high energy costs and frequent blackouts?

The Grid from Hell and the Blame Game

If you only listened to the U.S. government, you’d think that it’s all LUMA’s fault that the island suffers frequent outages.

On September 27, the House Committee on Energy and Commerce sternly rebuked LUMA in a letter to CEO Wayne Stensby, writing “Ongoing outages and the complete disruption of power following Hurricane Fiona amplify concerns that LUMA has failed to adequately develop and maintain crucial electrical infrastructure in Puerto Rico despite its lucrative 15-year contract.”

LUMA employees conceal their association with the company for fear of retribution, although they bear no responsibility for the island’s current state of electrical misadventure. After all, LUMA has only been on the case for a year and a half.

It is widely known that the island’s power grid relies on a central power line and obsolete equipment over 50 years old. The reasons for this are popularly cited as “underinvestment” which is only a small part of the story.

What is less well-known is that the cause of Puerto Rico’s power woes is greatly due to massive fraud perpetrated by the formerly government-owned power utility company, Puerto Rico Electric Power Authority, known as PREPA. Although bankrupt, PREPA technically owns the island’s grid assets, not LUMA.

It’s counterintuitive that PREPA continues to own electrical infrastructure and be the recipient of federal disaster funds meant to rebuild the power system, given its monumental theft and waste of billions of dollars from investors and customers, for which government and independent investigators said PREPA employees should be prosecuted and the company should be restructured.

It seems like this should be a big deal, but it has been sparsely reported in the media, and none of the criminals who perpetrated this fraud have been held accountable, nor has the company been restructured. However, one of the victims of the fraud, Richard Lawless, whose solar power company nearly went belly up because of PREPA’s shocking deceptions, is the lone voice agitating for justice.

Solar Power CEO versus Puerto Rico’s state-owned fraud machine

From 2000 to 2012, PREPA issued bonds totaling around $11.4 billion dollars to pay for the projects. The future looked bright.

PREPA was tasked with expanding renewable energy in Puerto Rico, and the company doled out millions of dollars in contracts to North American solar power companies to bring solar power to Puerto Rico. Richard Lawless’s company, Commercial Solar Power, was a recipient of one of these contracts.

Barclay’s and Morgan Stanley underwrote $3.5 billion in bonds in 2014, but by 2017, the SEC recommended enforcement actions against Barclay’s bankers James Henn and Luis Alfaro for fraud, deception, and misrepresentation regarding the bonds.

Bloomberg reported that the SEC also intended to issue sanctions against Morgan Stanley managing director Charles Visconsi and Jorge Irizarry “in connection with disclosures Puerto Rico made in documents circulated to investors,” which is a dainty way of saying that they knew or should have known that they were aiding in the perpetration of a fraudulent scheme.

Wall Street Rating agencies S&P, Moody’s, and Fitch gave these bonds BBB+ ratings, meaning that the risk of default is low. It didn’t matter that PREPA was already bankrupt and their financial statements were full of holes that a first-year accounting student could identify.

Richard Lawless wrote in his book, Capitol Hill’s Criminal Underground, “It would have been impossible to commit $70 billion in fraud without the explicit knowledge and approval of the executives and the board of directors at the rating agencies. It would also be statistically impossible for Moody’s, Fitch, and S&P to all miss the same critical underwriting issues without some form of collusion or antitrust issues.”

Puerto Rico Follows the Money

Where did all this money go? The Puerto Rican House of Representatives created a Commission to find out. In 2015, the legislative body held hearings concerning an alleged oil scam. They discovered that PREPA was deeply in debt, to the tune of $8.3 billion.

PREPA had raised $11.4 billion from the bonds, spending $2.7 billion on capital works and paying $164 million on various financial consultants and advisers who worked for PREPA. The remaining $8.5 billion was spent on refinancing and interest payments.

The House Commission report explicitly showed that PREPA “thereby circularly [refinanced] its debts and interest, with no regard for the amortization of the original debt.”

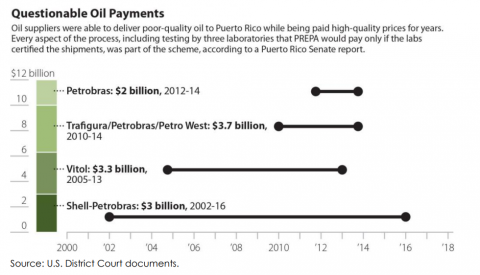

Meanwhile, the utility was importing Venezuelan sludge oil, for which it paid a premium price, falsifying quality reports at PREPA labs to claim it was higher-grade oil and paying kickbacks to politicians and executives.

When the President of the Commission went to PREPA to obtain documents of what they had done with the billions they solicited in bonds from 2000 and 2012, the utility couldn’t even produce documents.

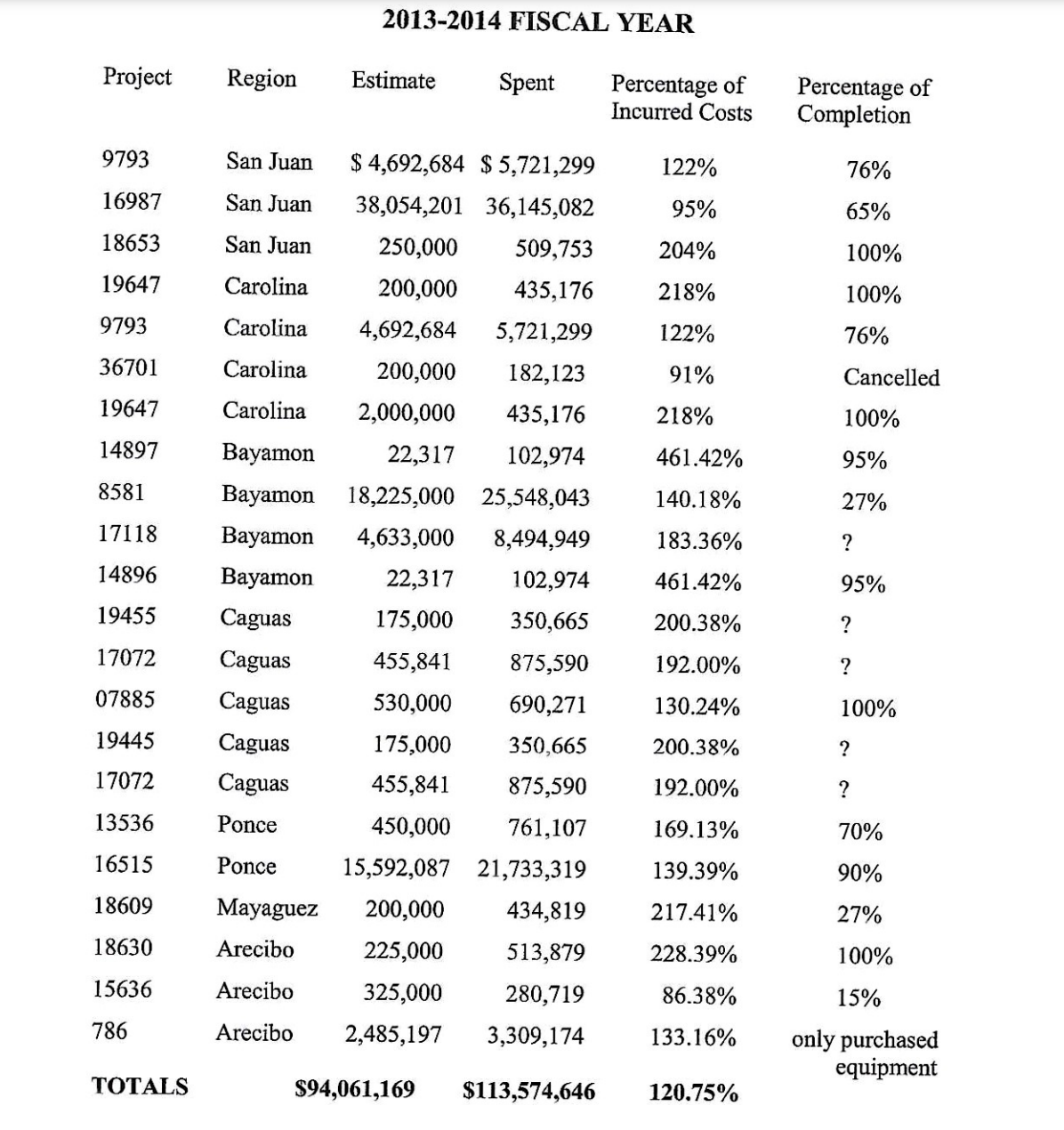

The Commission was able to retrieve documents for the budget from 2012 to 2014, and the documents clearly showed how PREPA repeatedly underestimated costs and abandoned projects. The company didn’t even engage in projects that would generate power.

Just one page clearly laid out the disastrous hash PREPA made with the billions it was entrusted.

I would draw attention to the last two columns, which shows that the company routinely spent twice as much as it estimate on projects, yet just as often failed to complete the projects, abandoned them, or didn’t even know how much was completed.

The Commission seemed puzzled that anybody invested in PREPA’s bogus bonds, writing that “Bondholders must have been aware of the above because… this information was available and no false representations were made.”

Perhaps, the bonds’ BBB ratings, courtesy of Fitch, S&P, and Moody’s, along with the Wall Street banks’ underwriting, were sufficient to coax investors to reach into their wallets, which was the conclusion of the Commission, accusing PREPA’s creditors of “negligent acts.”

The Commission also documented how from 2000 to 2012, PREPA went from using half of its money to refinance its debt, then up to 85% during multiple years. So, PREPA sold bonds on Wall Street and then used most of the money to refinance.

The Commission writes that it “realized that PREPA paid previous bondholders with capital received from new investors.” Sounds a lot like a Ponzi scheme, yet the financial intermediaries were handsomely compensated with $40 to $60 million over a four-year period.

Hedge Funds Pile in on Junk Bonds

Then, when the bondholders realized the debt was bad, the hedge funds, such as Elliott Capital Management (which we wrote about here) swooped in to buy them for .50 cents to the dollar, or even as low as .40. These vulture funds didn’t want anybody making noise about how worthless these bonds were, given that the issuer was not only bankrupt but deep in criminal fraud.

However Richard Lawless, the solar power CEO who lost his business due to the fraud, was making noise. Lawless sent emails and letters to the SEC, the FBI, and the boards of every organization involved, including the rating agencies and the partners of PREPA, explaining the fraud and begging for accountability.

When he got cease and desist orders or silence as a response, he started publishing articles. Then, he started receiving calls from blocked numbers and death threats. One caller allegedly represented the new group of hedge fund bondholders, who tried to bribe Lawless with the suggestion that the new bondholders could “help with the financing for your project.”

The hedge funds were betting that they could recoup their investment in the bankruptcy court, but publicizing the fraud could draw more attention to those proceedings and make the creditors more forceful and more numerous. So if they paid him off, could he just keep quiet? Lawless angrily declined, later saying the offer made his skin crawl.

And so the question arises, what stopped regulators from intervening in this Ponzi scheme?

We’ll explore this question in Part Two of our series. In Part Three, we’ll discuss who benefits.

Author: Tim Tolka, writer, journalist, and BI researcher

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organizations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

2 Responses

You should write an article about how the USA congress should introduce legislation to impose and name a gobernor in PR.the incompetence of the politicians in PR is incredible this people lack the knowledge to do anything that will actually help the island the island is in terrible condition, there is garbage all over the place badly built highways mediocrity and monopolies that operate without accountability a total disaster nothing works,a judicial system corrupted and in cahoots with organize crime.this island needs a total cleanup.

Mr. Lawless in still in process of taking on our Justice dept by himself. Legal firms want in the millions to represent him. How can one who has be ruined by govt corruption afford this. Sept 6, 2023 in Santa Ana, Ca he will have a trial-setting conference. It’d be nice if any media was present to show an interest in this case because it will set a precedence for the rest of those ruined in similar situations.