Hedge funds are not running from AI. They are locking in gains before the market questions how much of the AI boom is already factored into prices. Goldman Sachs’ prime brokerage data, reported by Reuters on July 6, showed that U.S. hedge funds net-sold information technology hardware and semiconductor stocks for a fourth consecutive week, as the Philadelphia Semiconductor Index (SOX index) fell 4.2% in the week ending 3 July.

That same week, Bloomberg reported that many of the same managers had just posted their strongest first half in five years. Both facts are real, and they belong in one story. The story is about de-risking, or trimming exposure to protect existing profits rather than a change of view, after a crowded trade that worked.

The AI Trade Paid: Lone Pine, Appaloosa, Coatue and Whale Rock Post Outsized Returns

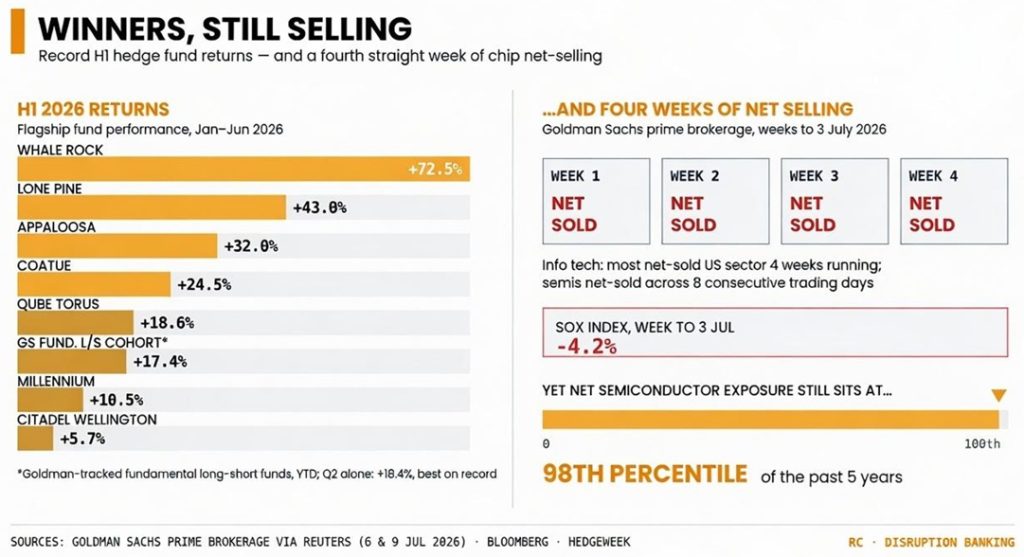

Lone Pine Capital returned 43% in the first half, one of its best starts on record, with both long and short books contributing. Appaloosa Management gained roughly 32%, built largely on memory-chip bets. Whale Rock Capital surged 72.5%, its long-only sleeve 82%, powered by SanDisk (up more than 850%), SK Hynix (over 300%) and TTM Technologies (about 170%), not Nvidia. Coatue Management added 24.5% year-to-date (YTD).

Goldman-tracked fundamental long-short hedge funds returned 4% in June and 18.4% for the second quarter, the strongest quarterly result on the bank’s records, for 17.4% YTD, with systematic funds up 11.3%. The multistrategy giants trailed: Millennium gained 10.5%, Citadel‘s Wellington 5.7%, Qube Research & Technologies’ Torus 18.6%. The funds now selling chip stocks are, in large part, the funds that made the trade pay.

Goldman’s Prime Data Points to Profit Protection, Not an AI Exit

The selling is real and orderly. Net selling in semiconductors stretched across eight consecutive trading days, and it was net-sold in aggregate, with more selling than buying overall, even as some funds kept adding. Managers also cut single names in industrials and consumer discretionary while buying index and ETF products and rotating into commercial services, consumer staples, real estate and energy.

Positioning settles the exit-versus-de-risking question. Even after four weeks of selling, hedge fund net exposure to semiconductors remained at the 98th percentile of the past five years. “We don’t think this is a regime shift from a fundamental perspective,” Goldman’s Vincent Lin said; rallying chip positions mechanically swelled as a share of portfolios, forcing risk-management sales. Funds are trimming from extreme concentration, not fleeing it.

Samsung’s Profit Rose Nineteenfold. Its Shares Still Fell Sharply 10%

On 7 July, Samsung Electronics estimated second-quarter operating profit of 89.4 trillion won ($58.4 billion). Up roughly 19-fold from 4.7 trillion won a year earlier and beating the LSEG SmartEstimate of 87.3 trillion won, with revenue up 129% to 171 trillion won. The shares still fell as much as 10.1% intraday to close down 6.9%, erasing more than $80 billion of market value; SK Hynix ended 6% lower.

When a record beat triggers a double-digit slide, the market’s bar for AI-linked earnings has moved above what even blowout results can clear. Morgan Stanley told clients that investors are bracing for “more capex discipline in the near-term” from the hyperscalers. Against that bar, trimming winners before they report is rational even for managers who still believe in AI capex.

What Comes Next: Earnings Season Will Decide Whether Four Weeks of Chip Selling Was Brilliant or Premature

Earnings from the AI-infrastructure chain will now decide whether the expectations wall holds or this proves routine profit taking. At the 98th percentile, funds still own most of the upside if guidance clears the bar, and most of the drawdown if it does not. The positioning is a judgment deferred, not a verdict delivered.

The pattern matches what Disruption Banking observed in June, when Pershing Square and Third Point traded Microsoft and Alphabet in opposite directions, hedge funds rotating within the AI trade rather than out of it. Four weeks of chip selling by funds sitting on five-year-best returns is the same behaviour at sector scale: the trade has not been abandoned. It has been banked.

Author: Richardson Chinonyerem

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organisations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

Can Ackman Sell Public-Market Permanence While Pershing Square NAV Is Falling? | Disruption Banking