Few trades in recent market history have been this dramatic. The shares of SanDisk Corporation (NASDAQ: SNDK), the Milpitas, California-based pure-play NAND flash memory and enterprise solid-state drive manufacturer, have climbed roughly 3,710% since its separation from its parent company, Western Digital Corporation (NASDAQ: WDC), in February 2025, transforming a mid-tier storage business into a $231 billion (TradingView) AI infrastructure story.

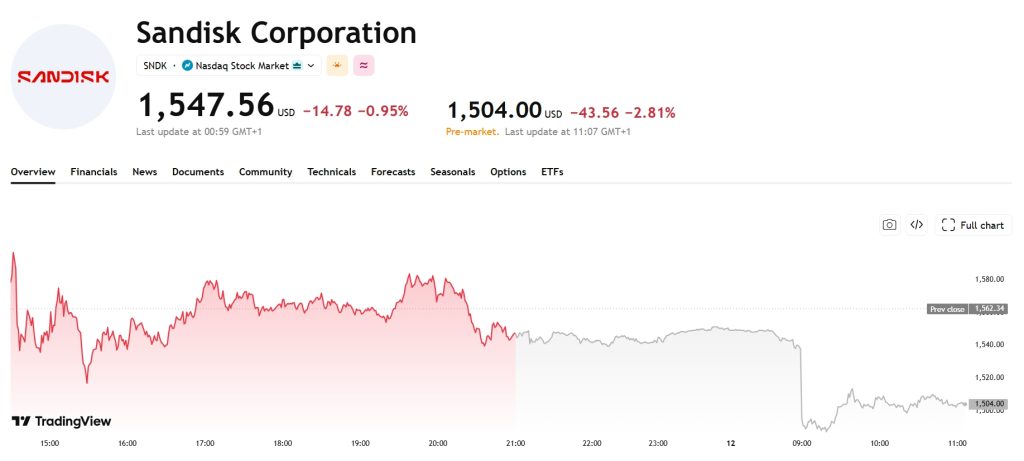

Moving from an initial low of $33-$34 to close at around $1,547.56 per share (TradingView) at the time of writing, the company now sits among the S&P 500’s most expensive positions on a valuation basis.

For investors who missed the initial surge, the question now is: Is there still a case to be made for buying, or has the market already priced in the good news?

Source: TradingView

The Spin-Off That Rewrote the Valuation of SanDisk

When Western Digital, the San Jose, California-based data storage company and SanDisk’s former parent, completed the separation of its flash business on February 21, 2025, SanDisk listed independently with a market capitalisation of roughly $7 billion. Western Digital, retaining the hard drive business, was worth approximately $17 billion at the time. That relationship has since inverted.

SanDisk’s market value now surpasses that of Western Digital, which currently sits at roughly $165.5 billion (TradingView), at the time of writing. According to Slickcharts data, SNDK now rubs shoulders in terms of market value with the likes of Verizon Communications (VZ) ($197 billion), McDonald’s (MCD) ($196 billion), and IBM ($216 billion).

The split removed complexity and allowed SanDisk to focus entirely on its flash memory and Solid-State Drive (SSD) business. Markets typically assign higher multiples to pure-play companies than to diversified conglomerates. Once freed from Western Digital’s hard drive operations, SanDisk could be priced purely on its enterprise SSD and NAND flash exposure. The market quickly concluded that it was worth substantially more on its own terms.

How Is AI Turning Flash Memory Into Essential Infrastructure?

The timing aligned with a structural change in demand. AI systems, from the large language models (LLM) powering consumer applications to the inference engines embedded in cloud infrastructure, require vast quantities of high-speed storage. Every model trained, every prompt processed, every dataset staged for a GPU cluster needs NAND flash: the type of storage used in solid-state drives across consumer and enterprise markets alike.

Big Tech is spending $700 billion this year alone on data centers, with Microsoft expecting capex to rise to $190 billion. To secure supply, customers are offering to fund factories. Reuters reported SK Hynix has “essentially zero” available capacity, and that Samsung and SK Hynix said the shortage will persist due to structural AI growth.

Memory makers have responded with a new playbook: multi-year agreements with price bands and prepayments, designed to smooth volatility. Sandisk calls it a shift to “multiyear customer engagements backed by firm financial commitments.”

The Numbers That Justified, Then Outpaced, The SanDisk Rally

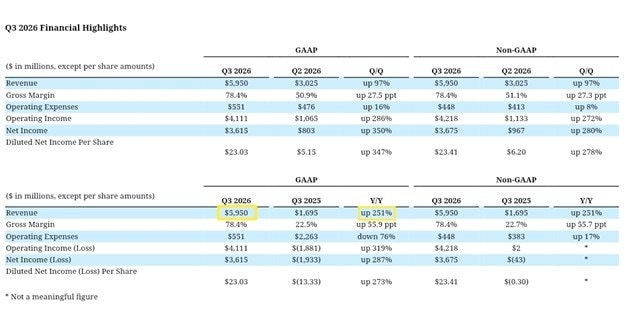

SanDisk’s financials tracked the demand surge decisively. In its fiscal third quarter ending April 3, 2026, the company reported revenue of $5.95 billion, up 251% year-on-year (YoY) and 97% sequentially, beating its own guidance range by a significant margin.

Datacenter revenue grew 645% YoY to $1.47 billion, and 233% sequentially, with gross margin hitting 78.4%, driven by a mix shift toward higher-value customers. Net income reached $3.6 billion, or $23.41 per share non-GAAP, up from a loss a year earlier. The company has also signed long-term contracts worth at least $42 billion with hyperscaler customers, providing a revenue floor that traditional memory businesses rarely enjoy.

Fourth-quarter guidance projects revenue of $7.75-$8.25 billion, with non-GAAP earnings per share of $30–$33 — figures that would have seemed implausible twelve months ago.

CEO David Goeckeler called it “a fundamental inflection point” toward higher-value markets.

SanDisk SNDK Q3 2026 Financial Report Filing. Source: SEC

Why Bulls Think the Run Is Not Over for SanDisk

The numbers above support the re-rating thesis. Bernstein raised its price target on SanDisk to $1,700 following the Q3 results, maintaining an Outperform rating. Morgan Stanley remains Overweight, though it notes it will take time for earnings to grow into the current stock price.

Bulls point to three main drivers:

- Contracted demand. Sandisk signed three agreements in the March quarter and two more in June. Jefferies estimates the first three represent a minimum of $42 billion in value.

- Pricing power. With supply tight, Bernstein’s Mark Newman argues the contracts allow “long-term stability” and “attractive economics over a longer horizon.”

- Balance sheet optionality. The company ended the quarter with zero debt and authorized a $6 billion buyback.

The structural case, however, centres on constrained NAND supply, multi-year contracts that reduce earnings volatility, and the broader AI inference build-out, described by analysts as still in early innings.

While 2023 to 2024 was about GPU-heavy AI training, the shift from late 2025 may make 2026 the year of AI inference, a workload that places sustained, high-volume demands on enterprise storage.

Is SanDisk Overvalued? The Risks Behind the 3,700% Surge

The concern of investors is not the business, it is the price. Morningstar currently estimates SanDisk is trading at a 343% premium to its assessed fair value, describing the company as selling commodity-like NAND flash with limited pricing differentiation and meaningful exposure to cyclical oversupply.

Bernstein, while bullish long-term, recently warned that Original Equipment Manufacturer (OEM) and module houses are being forced to reduce purchases as prices surge, and sees price increases “decelerate notably into 3QCY26.” After a 3,756% gain in a year, Sandisk trades with expectations that leave little room for error.

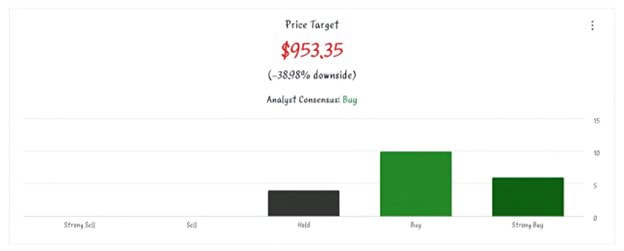

The average price target across 20 analysts sits at approximately $953, according to Stockanalysis, implying the stock has already overshot the consensus by a wide margin. JPMorgan initiated coverage with a Neutral rating, a notable counterweight to the bullish consensus.

SanDisk SNDK Analysts’ Price Forecast. Source: Stockanalysis

The structural risk has not disappeared. Memory markets have repeatedly rewarded demand booms with capacity expansion, eventually producing the price collapses that made semiconductors famous for their cyclicality.

SanDisk’s consumer segment, per the company’s fiscal Q3 2026 financial results, already contracted 10% quarter-on-quarter (QoQ) in Q3, an early signal that not all segments are immune to that dynamic.

Is SanDisk’s 2026 Rally a Structural AI Win or Cyclical Risk?

SanDisk is genuinely benefiting from a fundamental shift. AI infrastructure requires storage at a scale and density that has changed the economics of NAND in ways that long-term hyperscaler contracts now reflect. That is not nothing. But the stock trades as though the story is already complete, certain, and uninterrupted.

Morgan Stanley’s own caveat, that earnings will need time to grow into the current valuation, is perhaps the most useful framing available. SanDisk may still be worth owning as a long-term AI infrastructure position.

For investors entering at today’s price, however, the margin for error is narrow. After a nearly 28-fold rally, the burden of proof has shifted significantly.

Author: Richardson Chinonyerem

See Also:

How Is Oil Futures Complacency Risking Global Supply Chains? | Disruption Banking