Summary

- The Fed may be preparing to adjust the structure of policy rates to encourage banks to hold fewer reserves.

- The Powell–Warsh transition could be turbulent, but is unlikely to materially affect Fed policy.

Market Implications

I continue to expect a recession and around four Fed cuts in H2, in contrast to market pricing, which reflects a soft landing and only a one-third chance of a 2026 cut.

Is The Fed About to Shrink It Balance Sheet?

In this note, I discuss the next steps in the Fed balance sheet adjustment as well as in the Powell-Warsh transition.

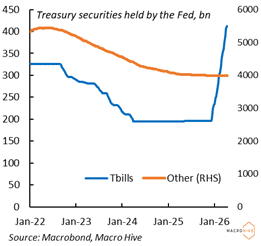

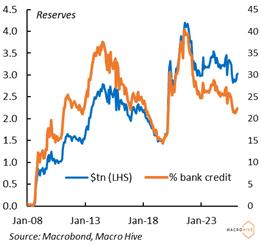

The New York Fed has announced a reduction in its reserve management T-bill purchases to $25bn per month, down from the $40bn per month pace introduced after the 10 December FOMC meeting (Chart 1). At the time, the Fed was responding to volatility in money market rates, which, following a roughly $300bn decline in reserves, suggested that reserve levels had fallen below what is considered “ample” under its operating framework (Charts 2 and 3).

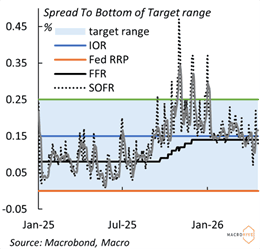

The resumption of asset purchases helped to stabilize SOFR well below the Fed’s Standing Repo Facility (SRF) rate. Interestingly, however, the Fed has not adjusted the federal funds rate (FFR) within its target range. The FFR now sits just 1bp below the interest on reserves (IOR)—effectively the deposit rate—compared with an average spread of around 8bp prior to August 2015. As a result, banks’ incentive to hold excess reserves has diminished.

The Fed could even consider allowing the FFR to rise above the deposit rate, further reducing the incentive to hoard reserves. International experience suggests this could lead to a smaller balance sheet: in countries such as Australia, Canada, and Sweden—where policy rates sit below market rates—banks tend to hold fewer reserves relative to the size of their banking systems.

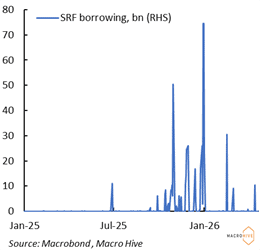

While the FOMC remains committed to an ample reserves framework, it is increasingly aware of its inefficiencies. In the latest round of quantitative tightening, the Fed attempted to lower the level of reserves required by boosting banks’ reliance on the SRF. However, take-up has been limited, and at times SOFR has traded well above the SRF rate, raising questions about its effectiveness (Chart 4).

As Chair nominee Kevin Warsh has expressed a preference for a materially smaller balance sheet, a potential compromise with an FOMC that broadly supports the ample reserves regime could involve adjustments to the structure of policy rates, rather than a wholesale shift in the operating framework.

Chart 1: Fed Rebuilding Reserves

Chart 2: Reserves Ample Again?

Chart 3: Interest Rates Have Stabilized

Chart 4: Limited SRF Uptake

A Complex Leadership Transition

Senator Tillis spoke warmly of Warsh during his confirmation hearing but made clear that he would not lift his hold until the DOJ drops its lawsuit against Chair Powell and the Fed. The DOJ, however, shows no sign of backing down: last week, it sent two criminal prosecutors and an investigator to the Fed building site without prior notice.

This suggests that, by 15 May—when Powell’s term as Chair expires—Warsh is unlikely to have been confirmed. At the 18 March FOMC, Powell indicated that he intends to remain as chair pro tempore until a successor is confirmed.

This could trigger a legal dispute with the administration, as the statutes are unclear. The Federal Reserve Act provides neither an acting chair provision nor a defined succession mechanism. It is also uncertain whether the Federal Vacancies Reform Act—which allows the President to appoint an acting official to a Senate-confirmed role—applies. Precedent offers limited guidance: most Fed Chair transitions have been seamless, while the few longer postwar gaps saw either the outgoing Chair remain in place or the Vice Chair assume operational leadership.

I still expect Warsh to be confirmed eventually. If Democrats win the Senate, confirmation could come in the lame-duck session after the DOJ drops its lawsuit. If Republicans retain control, confirmation is more likely after the new Congress convenes in January 2027, as Senator Tillis is retiring this year.

Table 1: Multiple Transition Precedent

Market Implications

In my view, markets are overestimating the “Warsh factor.” I was struck by the relatively hawkish tone of his confirmation hearing: the word “inflation” was mentioned 74 times, versus just 23 references to “employment”. In addition, the Chair is only one of twelve FOMC voters, and Warsh’s incentives are likely to shift once in office, when he can no longer be removed. I also do not think the size of the balance sheet will have much economic impact, as any change would be gradual, and the FFR for now remains the Fed’s main policy instrument.

I therefore continue to expect a recession and around four Fed cuts in H2, in contrast to market pricing, which reflects a soft landing and only a one-third chance of a 2026 cut.

See also:

Allfunds Publishes Trading Update for Q1 2026 | Disruption Banking

The Payments Association Calls for Revised Stablecoin Regulation | Disruption Banking

Gebeya and PROFF-IT (VukaOS) Forge Strategic Alliance to Redefine African Startup Creation | Disruption Banking