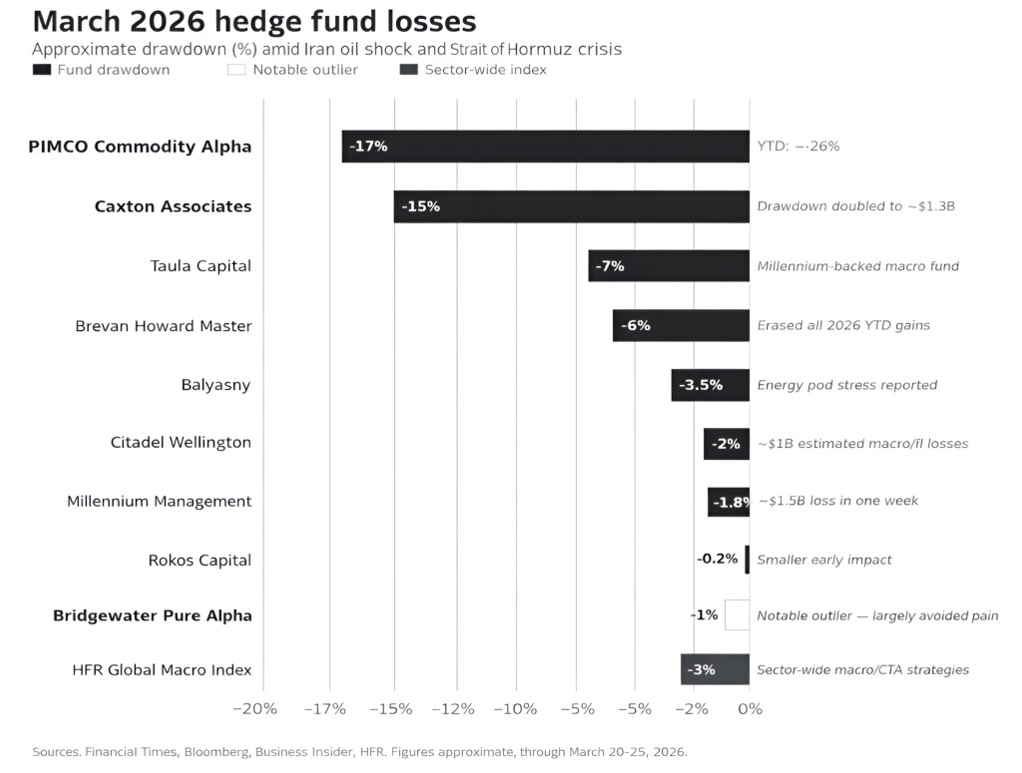

The PIMCO Commodity Alpha Fund, a relative-value strategy that has been running for more than a decade, has shed roughly 17% this March alone, pushing year-to-date (YTD) losses to approximately 26%, according to Bloomberg.

Before this month’s collapse, the fund managed around $3 billion. The fund had already lost about 9% over the course of 2025, according to an anonymous source familiar with the matter. That means the slide predates Operation Epic Fury. The fund’s positioning was already flawed before the U.S. and Israel struck Iran on February 28, 2026.

Asian Jet Fuel Prices Up 114%

The losses weren’t just about crude oil. The damage was amplified by jet fuel trading, according to Tenet Research. Joint U.S.-Israeli strikes sent Brent rocketing from around $72 a barrel on February 27 to over $119 briefly in early March (TradingView).

Iran retaliated by attacking vessels in the Strait of Hormuz, collapsing tanker traffic, and pushing Asian jet fuel prices 114% higher to $199.66 per barrel by mid-March. Singapore gasoil also shot up 57% to $143.88 per barrel. LNG plants in Qatar were disrupted. U.S. gasoline prices climbed more than 30% to their highest level since 2022.

The PIMCO fund’s relative-value structure, designed to profit from price spreads between energy products, was caught off guard. A shock that moved all energy prices violently in the same direction at once demolished the spread logic entirely.

PIMCO Down 26% as $1B+ Losses Hit Citadel, Millennium & Caxton

Other major funds absorbed serious damage. Caxton Associates’ $9 billion macro fund is down roughly 15% in March, a $1.3 billion loss. Millennium Management lost approximately $1.5 billion in a single week. Citadel shed roughly $1 billion from its fixed-income and macro books. Brevan Howard, Taula Capital, Balyasny, and Chris Rokos’ fund all posted losses in early March.

More than 95% of funds have lost money since the strikes began. Not everyone lost, though. Pierre Andurand’s fund gained 6% last week. NB Commodities and Galena Commodities gained double digits on the oil spike. Saber Capital is up 12% year-to-date (YTD).

The dividing line? Directional energy bulls got paid. Relative-value plays that missed the direction got crushed. The split shows how quickly the Iran War divided winners from losers.

Brent at $106: Iran Rejects Ceasefire Talks Again

As of March 26, Brent crude traded at ~$106, up 3.8% on the day, after Iran’s Foreign Minister Abbas Araghchi publicly rejected direct U.S. peace talks. West Texas Intermediate (WTI) futures climbed 6.8% to $100. Both benchmarks sit roughly 47% above pre-war levels.

On March 25, the U.S. sent Iran a 15-point peace framework via Pakistan, stocks rose globally and Brent briefly dipped to around $102. But President Trump told Iran on March 26 to “get serious” on negotiations while threatening further escalation, and oil edged higher again.

The Strait of Hormuz remains contested. The IEA has described the disruption as the greatest global energy security challenge in history.

Goldman Sachs and Mattioli Woods Warn: Don’t Count on a Fast Rebound

Daan Struyven, co-head of global commodities research at Goldman Sachs, describes current pricing as “a geopolitical risk premium” over fundamentals, estimating that supply fundamentals alone justify roughly $85–88 Brent. The bank’s base case assumes Hormuz flows normalize in April over four weeks.

But Mattioli Woods’ investment manager, Katy Stoves, isn’t convinced markets are pricing in the rebuild time. “Even if we do get a resolution, I think it’s very, very important to note that there’s been a lot of energy infrastructure destroyed during this, and even if we do get some sort of ceasefire … repairing those facilities, bringing those facilities back online is going to take time…,” she told CNBC.

If ceasefire talks hold, oil could retreat toward $80–$90 and give some funds room to claw back losses. But history shows these shocks last longer than markets expect, especially with damaged infrastructure that takes years to fix.

What’s Next for PIMCO, and the Market?

PIMCO declined to comment on the fund’s losses. That silence speaks volumes. The fund is now down by a quarter for the year with a war unresolved, ceasefire talks stalling, and Brent holding above $100 for the sixth consecutive week.

If anything, the PIMCO story illustrates a broader problem: relative-value commodity strategies assume markets return to historical spread relationships. They don’t. Not when a geopolitical shock closes the world’s most critical energy chokepoint.

In all, the PIMCO Commodity Alpha Fund’s drawdown is not the end of commodity plays, but a tangible lesson in strategy during geopolitical tensions: in 2026, generating alpha in commodities demands better risk controls when wars break out. Ignore that at your portfolio’s peril.

Author: Richardson Chinonyerem

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organizations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

Dow Jones Down 2,440 Points as Iran’s Hormuz Oil Crisis Hits Hard | Disruption Banking

From “Liberation Day” Panic to 10 % Gains, PIMCO’s Revenge | Disruption Banking