Hedge fund manager Paul Singer is at it again with his activist fund Elliott Investment Management, piling billions into Synopsys, one of only three “electronic design automation companies” (a fancy way of saying it designs microchips) that are essential in the semiconductor value chain.

The chip racket is one of the most capital-intensive endeavors humankind has ever attempted, and the road to the iridescent city is littered with broken dreams. It takes $10-20 billion just to start and decades of iteration to develop the precise process knowledge, at which point the technology used to reach the apex atomic scale will probably already be obsolete.

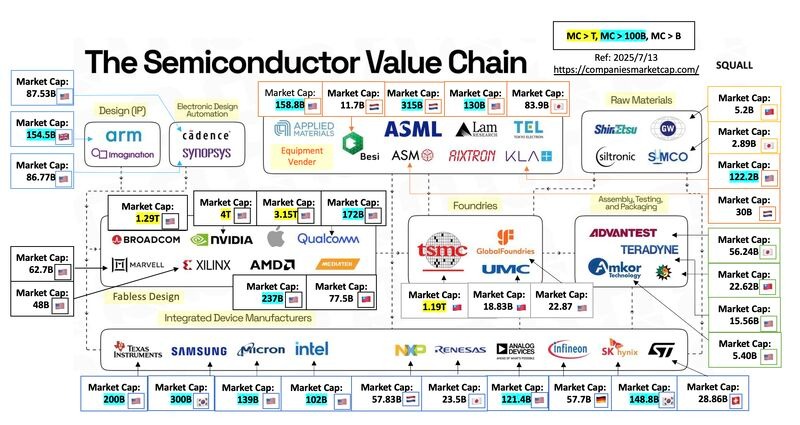

The Quiet Cartel Behind Every Chip

Valued at $80 billion, Synopsys has been in the chip business for decades and is one of the main providers for Nvidia, which mints $.68 cents of profit for every dollar of chips it manufactures.

Singer smells an opportunity. Renowned for risky bets on Latin American bonds and suing countries in U.S. federal district courts, Singer is a guy who notices things others miss, and he plays the long game.

Synopsys shares have dropped 12.5% this year, but Singer is betting that the headwinds the company has faced will prove transitory, once the firm’s management takes Singer’s advice.

The Elliott Way: Don’t Buy the Dip, Buy Leverage

Elliott Managing Partner Jesse Cohn told the Wall Street Journal, “as AI drives a step change in chip complexity and capital investment, Synopsys is uniquely positioned to benefit from this growth.”

The shares of Synopsys are up 4% since the news broke. Activity in the options market leans clearly optimistic. According to dashboard data from Barchart, traders expect more movement in Synopsys shares in the near term than the stock has shown recently, indicating that Elliott’s stake is expected to shake things up.

There are more bets on the stock going up than down, and overall positioning points to investors taking on risk rather than hedging against losses.

The options market is pricing in bigger-than-usual moves in Synopsys, but not a full-blown volatility spike, while positioning remains decidedly bullish. Volatility is elevated compared to much of the past year, but it’s not at extreme levels, suggesting it’s likely anticipation.

Synopsys has only two competitors, Cadence Design Systems and Siemens, although only Cadence appears in the Value Chain diagram below.

It’s not a bad position to be in, considering global semiconductor sales are expected to top $1 trillion this year.

High Barriers, Higher Margins, Highest Stakes

Elliott has its fingers in a lot of pies. Singer goes as big in global commodities as he has in risky bonds. Disruption Banking recently covered Elliott’s investment in Citgo, exposing an explosive conflict of interest accusation that no other outlet bothered to actually read, including Reuters.

When Elliott isn’t (allegedly!) fixing cases in U.S. federal district courts, they’re doing deep research into supply chains and profit margins.

In the case of Synopsys, they seem to be betting that chipmakers can’t easily change their electronic design automator. Still, when the customer is a company as wealthy as Nvidia, it’s not exactly a straightforward bet.

Also, it’s not clear that other firms shelling out big bucks on R&D won’t surpass Synopsys and take its place. Big tech is starting to design its own custom silicon, so Synopsys better get its butt in gear if it doesn’t want to lose its sought-after market position, which has been heretofore guarded by protectionist policies, weakening in the era of Trumpian backroom deals for the administration’s “special friends” in the Persian Gulf.

Elliott Doesn’t Show Up Without a Plan

The next indication of Elliott’s activity with respect to Synopsys is coming due very soon. Under current rules, an investor who becomes the beneficial owner of more than 5% of a covered class generally must file a Schedule 13D within five business days after crossing that threshold.

Initial reports of Elliott’s stake surfaced on March 22, so the 13D/13G should be arriving on the 27, unless the stake is under the threshold, which would be in keeping with Singer’s typically low profile, unless he gets fussy and files a lawsuit, exposing whoever has the misfortune to be against him to sophisticated, even treacherous, litigation tactics.

In the near term, keep your eyes peeled for that. In the long-term, watch out for Singer’s next move. Elliott probably has an ace up their sleeve.

Author: Tim Tolka, Senior Reporter

#Crypto #Blockchain #DigitalAssets #DeFi

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organizations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

If These Conflict Allegations Hold, the Citgo Auction Is Legally Unsalvageable | Disruption Banking

Hedge Funds and Crypto: A 2025 Bubble Waiting to Pop? | Disruption Banking

Billionaire Paul Singer Declares War on Phillips 66 | Disruption Banking