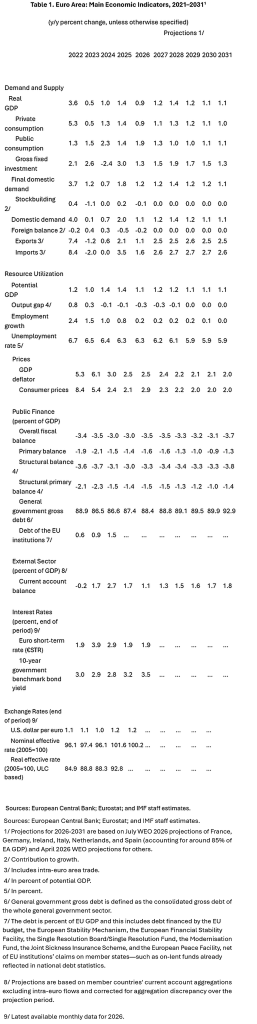

- The war in the Middle East has weakened the euro area outlook, with growth projected to slow from 1.4 percent in 2025 to 0.9 percent in 2026 and 1.2 percent in 2027 and headline inflation projected to rise from 2.1 percent in 2025 to 2.9 and 2.3 percent, respectively.

- Risks are skewed toward weaker growth and higher inflation, with the extent of energy market disruption from the war in the Middle East being the largest source of uncertainty.

- Monetary policy should aim to keep inflation expectations anchored and fiscal policy should mitigate the war’s harm to activity while remaining prudent. Structural fiscal consolidation remains a priority, especially in high-debt countries. Reforms should focus on strengthening energy security, deepening the single market, and lifting medium-term growth.

Washington, DC – July 16, 2026: On July 13, 2026, the Executive Board of the International Monetary Fund (IMF) completed the 2026 discussions on common euro area policies with member states.[1] The authorities have consented to the publication of the Staff Report prepared for this consultation.[2]

Following a period of growth at potential and inflation at target, the euro area outlook has weakened. The effects of the war in the Middle East include weaker confidence, tighter financial conditions, and inflationary pressures. Growth is projected at 0.9 percent in 2026 and 1.2 percent in 2027—0.5 and 0.2 percentage points below pre-war estimates—while headline inflation is projected at 2.9 percent in 2026 and 2.3 percent in 2027.

Risks are skewed toward weaker growth and higher inflation. A slower restoration of global energy supply would dampen growth and raise inflation further, even as a drop in confidence or financial stress could weaken demand. Further intensification of the war in Ukraine, or renewed disruptions and uncertainty from tariffs and trade policies, could weigh on activity more strongly or for longer than expected. Financial stability risks have risen with the weaker outlook and could increase further if a sharp global risk-off episode were to amplify negative wealth effects, or if balance sheet stress in leveraged nonbank financial institutions (NBFIs) arose and propagated to banks and core funding markets.

A carefully calibrated policy response is needed to manage the macroeconomic consequences of the current shock while advancing structural reforms to boost medium-term growth and resilience. The immediate priority is to keep inflation expectations anchored and cushion the impact of the shock within available fiscal space. These efforts should remain consistent with the longstanding structural agenda to strengthen Europe’s energy security, economic resilience, and potential growth.

Executive Board Assessment[3]

Executive Directors noted that while the euro area entered 2026 from a position of strength, energy supply disruptions linked to the war in the Middle East have weakened the outlook by raising inflation and dampening growth. A number of Directors also reiterated the continued impact of Russia’s war in Ukraine. Directors recommended a prudent, state‑contingent policy mix that balances maintaining macroeconomic stability and fiscal sustainability when managing the shock, while also advancing reforms to boost resilience, productivity, and medium‑term growth.

Directors supported a data‑dependent and well‑communicated monetary policy that is focused on maintaining price stability and well‑anchored inflation expectations by calibrating the response to the evolving inflation outlook. They broadly agreed that monetary policy communication underpinned by continued use of scenario analysis could help guide expectations given high uncertainty.

Directors agreed that the fiscal policy response to the current shock should rely on automatic stabilizers, and that any discretionary support should be temporary and targeted and preserve price signals. They emphasized the need for credible medium‑term plans to safeguard fiscal sustainability, which should be underpinned by expenditure prioritization, efficiency gains, structural reforms, and effective implementation of the EU fiscal framework.

Directors agreed that deepening the single market remains the most effective way to strengthen growth and resilience. They welcomed efforts to reduce cross‑border barriers, including through a proposed voluntary 28th regime, and called for measures to improve labor mobility, including effective integration of migrants, and AI readiness. Directors emphasized that achieving greater energy security requires further efforts to deepen energy market integration and advance the energy transition. They also stressed the need to advance the Savings and Investments Union and broadly agreed that the digital euro could enhance payments efficiency and deepen financial integration. Directors concurred that strengthening the EU budget and its financing framework would help support common priorities and resilience.

Directors welcomed the EU’s continued trade diversification efforts and its support for an open, rules‑based trading system. They concurred that policies aimed at reducing external supply vulnerabilities should be targeted in order to limit economic distortions, fiscal costs, and adverse spillovers, while building longer‑term resilience.

While noting the banking system’s resilience, Directors called for continued monitoring of vulnerabilities from stretched asset valuations and growing NBFI activity. They supported implementation of the FSAP recommendations, in particular to strengthen system‑wide stress testing, data collection and sharing, supervisory capacity, and the AML/CFT framework. Directors stressed the need to further strengthen the financial safety net through stronger resolution frameworks and completion of the Banking Union, while ensuring that regulatory simplification does not weaken prudential standards and that Basel III is fully and timely implemented. They agreed that stablecoins require continued monitoring as well as strong cross‑border supervisory cooperation and regulation.

[1] Under Article IV of the IMF’s Articles of Agreement, the IMF holds bilateral discussions with members, usually every year. Staff hold separate annual discussions with the regional institutions responsible for common policies for the countries in four currency unions – the Euro-Area, the Eastern Caribbean Currency Union, the Central African Economic and Monetary Union, and the West African Economic and Monetary Union. For each of the currency unions, staff teams visit the regional institutions responsible for common policies in the currency union, collect economic and financial information, and discuss with officials the currency union’s economic developments and policies. On return to headquarters, the staff prepares a report, which forms the basis of discussion by the IMF Executive Board. Both reports subsequently are considered an integral part of the Article IV consultation with each member.

[2] Under the IMF’s Articles of Agreement, publication of documents that pertain to member countries is voluntary and requires the member consent.

[3] At the conclusion of the discussion, the Managing Director, as Chairman of the Board, summarizes the views of Executive Directors, and this summary is transmitted to the country’s authorities. An explanation of any qualifiers used in summings up can be found here: http://www.IMF.org/external/np/sec/misc/qualifiers.htm.

See also:

IMF Executive Board Concludes 2026 Article IV Consultation with Israel | Disruption Banking

IMF Executive Board Concludes 2026 Article IV Consultation with Luxembourg | Disruption Banking

IMF Executive Board Concludes 2026 Article IV Consultation with Ireland | Disruption Banking