Five days after pricing the largest IPO in history, SpaceX has deployed its newly minted stock on one of the year’s biggest acquisitions. Transforming a valuation debate into a referendum on how far investors will stretch for the AI and space narrative.

The question hanging over ticker SPCX now is no longer whether the IPO was priced correctly. Five trading days of momentum and a $60 billion bet on an AI software company have made that question beside the point. What investors are asking now is: “How strong will SpaceX stock (SPCX) be in 2026?”

SpaceX’s First Five Trading Days: $75 Billion Raised, $2.5 Trillion Priced In

SpaceX priced 555.6 million shares at $135 on June 11, raising $75 billion at a valuation of roughly $1.77 trillion. DisruptionBanking reported it was more than triple the size of Alibaba‘s 2014 debut and larger than Saudi Aramco‘s 2019 listing, the previous record holder. Shares opened the next morning at $150, climbing as high as $176.52 before settling at $160.95, a 19.2% first-day gain. That pushed the market cap above $2 trillion and, by some calculations, made Elon Musk the world’s first trillionaire.

The rally didn’t stop there. By its fourth trading day, June 16, SPCX touched an intraday all-time high of roughly $226 before closing at almost $202, up about 49% from the offer price. That move came on the same day SpaceX confirmed a binding, all-stock deal to acquire Cursor‘s parent company, Anysphere, for $60 billion, per a securities filing. By far the largest acquisition of a venture-backed AI startup on record.

At the time of writing, SPCX sits at $189.50, with a $2.5+ trillion valuation (TradingView).

SpaceX’s $60 Billion Cursor Bet: AI Breakthrough or Expensive Rescue Mission?

The Anysphere deal brings roughly $2.6 billion in annualized B2B revenue and a widely used coding assistant, exactly the finished product the AI division and xAI’s exodus left it without. Cursor CEO Michael Truell, framed the deal as a chance in “building the world’s most useful AI models” alongside SpaceX’s engineering teams.

The all-stock nature of the $60 billion deal implies issuing roughly 312 million new shares at current levels (~$192/share). This represents meaningful dilution to existing shareholders, potentially 12-15%+ depending on the final share count and exact pricing at close, which will pressure near-term per-share metrics even as the acquisition bolsters the AI unit.

A separate, less-discussed transaction may matter just as much over the long run. The Federal Communications Commission (FCC) approved SpaceX’s purchase of roughly 65 MHz of nationwide spectrum from EchoStar for next-generation direct-to-device (D2D) Starlink, though regulators attached a $2.4 billion escrow requirement that could complicate final stages.

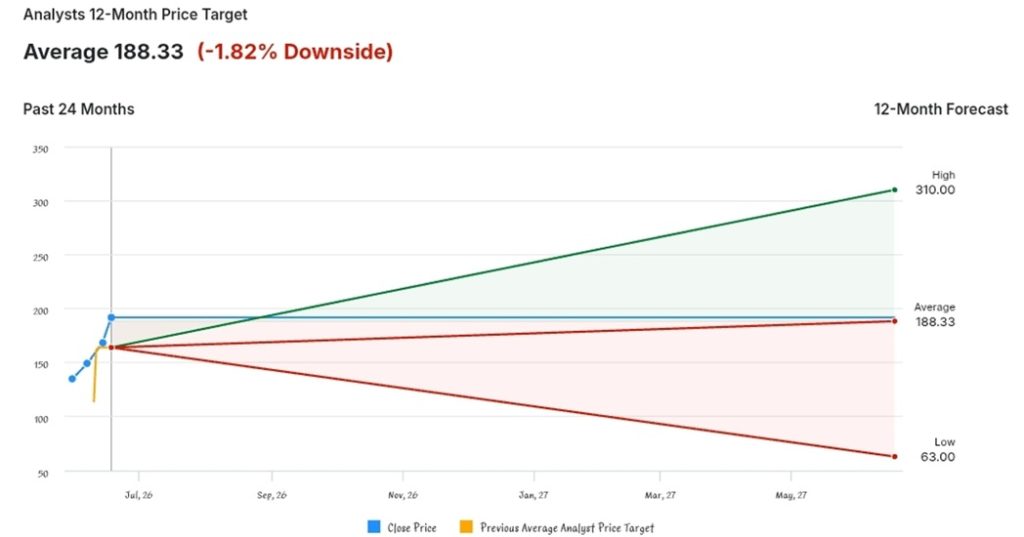

The Unusual 392% Analyst Spread: Nobody Knows How to Value SpaceX Stock Yet

According to Investing.com, six analysts have set 12-month price targets since the SpaceX IPO, with a spread unusual even by mega-IPO standards: a high of $310, a low of $63 (or $115 from the initial coverage), and a consensus average around $188 (implying a modest ~1.8% downside from the recent close near $192 on June 17). That’s a spread of roughly 392%,from low to high ($63-$310). For context, “Apple analysts normally sit within 10-15% of each other,” a report noted. Even “Tesla, which has attracted more analyst disagreement than almost any company in the S&P 500, carries a spread of around 40-50%.”

Oppenheimer‘s Timothy Horan was first off the mark, initiating coverage at Outperform with a $190 target. The stock blew past that target within 48 hours.

Other recent bullish readings are: Truist Securities ($261), and Zephirin Group ($310).

CFRA‘s Keith Snyder holds the only Sell rating at $115, built on a sum-of-the-parts model that pegs launch near $188 billion, Starlink near $159 billion, and the AI unit near $877 billion for a roughly $1.22 trillion fair value.

Morningstar‘s Nicolas Owens is most bearish at $63 a share on a probability-weighted DCF. His most optimistic “Moonshot” case, assigned only a 7% probability, tops out at $154, below where the stock trades today. Owens notes the tiny float and looming Nasdaq-100 inclusion could keep shares elevated “indefinitely” regardless of fundamentals.

Cathie Wood’s ARK Bought $529 Million of SPCX as Retail Investors Flooded the IPO

On the institutional side, Cathie Wood‘s ARK Invest bought roughly 3.29 million SPCX shares across four ETFs on listing day. A stake worth more than $529 million, while trimming positions in Tesla, AMD, Rocket Lab, and Roku to fund the purchase. The move aligns with ARK’s existing $2.5 trillion base-case valuation target for SpaceX by 2030, built on assumptions that Starlink ARPU stabilizes above $70, Starship reaches routine commercial service, and the Cursor deal helps xAI claw back enterprise AI market share.

Retail demand has been equally aggressive, with roughly 30% of the offering going to individual investors through Fidelity, Robinhood, and Schwab. An unusually large retail allocation for a U.S. mega-cap debut.

The Three Tests SPCX Must Pass in 2026

The bull case rests on a tripod converging at once:

- Starlink’s subscriber growth holding against Kuiper,

- Starship reaching commercial cadence in the second half of 2026. Made urgent by NASA’s Artemis III lunar mission in late 2026,

- The AI division, now anchored by Cursor, rebuilding the credibility it lost when its founding research team walked out the door.

SpaceX is currently excluded from the S&P 500 due to its $4.94 billion GAAP net loss in 2025 from its AI/xAI division, with S&P Dow Jones Indices explicitly declining to waive its profitability requirements, pushing potential inclusion to mid-2027 at the earliest. Nasdaq-100 entry is a nearer-term catalyst, expected around early July (that’s 15 days after SpaceX’s stock listing), with MSCI’s fast-track addition locked in for June 29. A combination of analysts’ estimates could force $22–27 billion in mechanical index-fund buying indifferent to valuation.

The standard 180-day insider lockup expires around December 8, with Musk’s shares locked separately for 366 days, until roughly June 2027.

SPCX at 134x Sales: The First Earnings Test Could Decide the 2026 Narrative

The spread between Wall Street’s most bearish Morningstar’s $63 fair value and the most bullish Street’s highest target of $310 is roughly 392%. Both sides are reading identical numbers on the S-1 filing: $18.67 billion in revenue, a $4.94 billion net loss, and the same Starlink ARPU data. What separates them is how much probability each assigns to breakthroughs nobody has proven at commercial scale.

At roughly 134 times trailing revenue, SPCX is priced for a decade in which nearly all of those bets land. The first real test is the September 2 earnings, which arrive in just over two months. Execution risks around Starship, AI integration, regulatory hurdles, and intensifying competition remain significant.

Ultimately, how strong SPCX will be in 2026 hinges on execution across the three tests. If Starlink holds share, Starship hits cadence, and Cursor integration delivers credible AI progress, the bullish case for a sustained premium remains intact. Failure on any leg, however, could see the stock re-rate sharply toward the bearish targets amid high multiples and post-lockup supply. The September 2 earnings will offer the first major data point in what is shaping up as one of Wall Street’s most polarized debates.

Author: Richardson Chinonyerem

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organisations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice. Price targets, fair-value estimates, and revenue projections are analyst and bank estimates, not guarantees of future performance.

See Also:

SpaceX IPO at $1.77 Trillion: Most Important Since Aramco, or Most Overvalued? | Disruption Banking