PDD Holdings, the company behind popular Chinese e-commerce platform Pinduoduo, has caught the eye of investors hunting for bargains following a 17% year-to-date decline in its Nasdaq-listed shares. Going by analysts’ overwhelmingly bullish outlook on the company, the stock could offer an attractive return to investors who are willing to look past the recent sell-off. According to Bloomberg, 53 of 56 analysts covering the stock have assigned it a “buy” rating, while the remaining three a “hold” rating. There are literally no bears when it comes to PDD– at least not on Wall Street.

It’s not difficult to understand why a section of investors are decidedly bullish on PDD. Investors often gravitate towards companies that demonstrate the ability to grow and expand their business without sacrificing profits. This is precisely what PDD has been able to achieve in the past few years, driving its share price higher by 67% over the past year compared with the S&P500’s 30% gain over the same period.

International Expansion Driving Growth

PDD profitably operates Pinduoduo, an online marketplace selling non-branded products at cheap prices in China. Launched in 2015, Pinduoduo has become a big hit with cost-conscious Chinese shoppers. The platform’s growth and success has transformed PDD into one of the leading e-commerce companies in China, alongside market leaders like Alibaba and JD. Importantly, this strong growth in market share has also translated into strong financial performance.

PDD’s revenues have grown in leaps and bounds in recent years, accelerating from $9.11bn in 2020, to $14.78bn in 2021, $18.92bn in 2022 and $34.88bn last year. Over this period, the company has pulled itself out of losses, recording net income of $8.45bn last year, a remarkable improvement from $4.57bn in 2022, and $1.22bn in 2021 – compared with losses of around $1bn in 2020.

Part of the reason for PDD’s strong financial results, particularly in 2023 when net income almost doubled from the previous year, is the company’s ongoing overseas expansion, which started in earnest in the final quarter of 2022.

Replicating the same business model of cheap, unbranded goods that has helped it corner the Chinese ecommerce market, PDD ventured into international markets in September 2022 with the launch of the Temu app. The weight of evidence seems to suggest that the app has been an instant success with bargain hunting online shoppers looking for low prices.

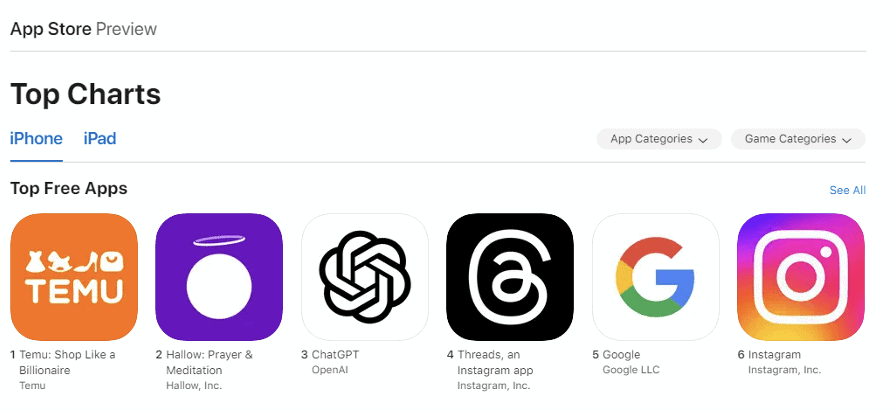

Currently available in more than 50 countries, including the US and several European nations, Temu has emerged as a significant challenger to many e-commerce incumbents. In the US, for example, it was the most highly downloaded app on Apple’s App store in 2023, ahead of OpenAI’s ChatGPT and Meta’s Instagram.

Temu was the most downloaded app in the Apple App Store in 2024 in the US.

Since its U.S. launch in September 2022, Temu has expanded to 47 countries, and as of October 2023, its app was downloaded 223 million times, with 120 million monthly active users and 43% of those coming from the U.S., according to analysts from Morgan Stanley.

“Temu is probably the most important thing to happen to global e-commerce in quite a long time,” notes Robin Zhu, senior analyst focusing on Chinese Internet companies at Bernstein Research.

Confronting Risks

While the weight of evidence seems to suggest that PDD’s low-price retail business model is popular with online shoppers outside of China, the company’s management has been somewhat reluctant to provide essential information about the app.

“PDD is known to be minimally communicative as far as business is concerned,” says Zhu, noting that the company is “secretive by culture” during earnings calls and other interactions with investors. As a result, PDD has not provided investors with sufficient tools to assess how different business segments are doing. This includes the highly watched international expansion driven by its Temu app.

“As a business unit within PDD Holdings, Temu doesn’t disclose its financials separately,” notes a statement from the company. This essentially means that investors have no real insight into the precise impact of PDD’s international expansion on the company’s performance. It doesn’t also help that control over Temu is shrouded in mystery. According to PDD, “the primary operating entity” for the Temu app is a wholly owned Ireland-based entity called WhaleCo, which primarily supports the legal and accounting functions for the app.

Moreover, PDD operates on an asset-light business model, which presents its own unique set of risks. Unlike its competitors, which includes the likes of Alibaba and JD, PDD does not own and manage its own fulfillment centers. It also doesn’t control exclusive distribution networks, instead choosing to outsource these functions.

As of now, PDD boasts a market capitalisation of $159.56 billion, compared to Alibaba’s $179.19 billion and JD’s $41.36 billion. However, despite PDD’s rich valuation, there’s a stark contrast in the workforce: Alibaba employs around 220,000 people, JD around 450,000, while PDD operates with a lean team of just 13,000. This extensive reliance on outsourcing is atypical of an ecommerce company of its scale and could potentially affect key performance indicators such as user experience and customer satisfaction, thereby posing risks for investors.

Looking Beyond Profits

The strategic move by PDD to outsource fulfillment and logistics has indeed positioned it favorably against competitors with lower profit margins. Yet, the absence of a Chief Financial Officer (CFO) since its initial public offering raises concerns about its corporate governance practices. The role of a CFO is often seen as critical for ensuring financial transparency and fulfilling fiduciary responsibilities, which are key to investor confidence.

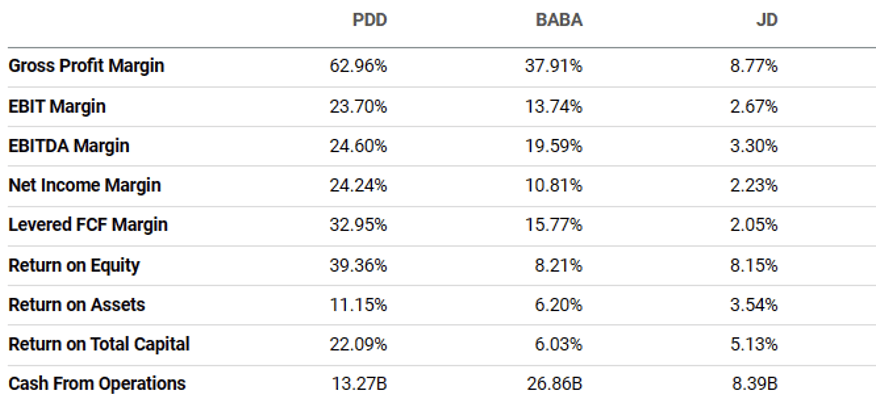

PDD has highest margins compared with Chinese ecommerce peers; source: Seeking Alpha

The lack of detailed disclosures, particularly concerning the contribution of the international business to overall sales, further compounds these concerns. Effective governance structures are essential for any public company, not only to maintain regulatory compliance but also to foster trust among stakeholders.

The decision to operate without a CFO may be viewed as a deviation from conventional corporate governance norms, which could potentially impact investor perceptions and the company’s long-term sustainability. Common reasons for corporate governance failure include inadequate oversight and accountability mechanisms, which a CFO could help to mitigate. Therefore, while PDD’s operational strategies may be yielding financial benefits, its governance approach, particularly the absence of a CFO, could be a point of contention for investors concerned with governance and transparency.

Investing in a stock like PDD, which is US-listed but Chinese, involves navigating a complex landscape where geopolitics play a significant role. The tensions between China and the US can indeed impact such companies, as seen in past instances where the Chinese government has intervened in the affairs of tech giants like Alibaba. This intervention is often viewed as a mechanism to maintain control over companies that accumulate substantial influence, which can be perceived as a threat to the established political order.

For investors, these dynamics underscore the importance of due diligence and a nuanced understanding of the geopolitical context. While PDD’s performance may be strong, and analysts’ outlooks optimistic, the potential for sudden policy shifts or international disputes could pose risks to the company’s stability and stock value.

Therefore, it’s crucial for investors to weigh these risks against the potential rewards and not to invest based solely on prevailing market sentiments. A balanced approach, considering both the bullish trends and the underlying geopolitical risks, is essential for making informed investment decisions about PDD.

Author: Acutel

We are global investors who invest in good companies at fair valuation and speculate on all else subject to the risk exposure we can afford.

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organisations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.