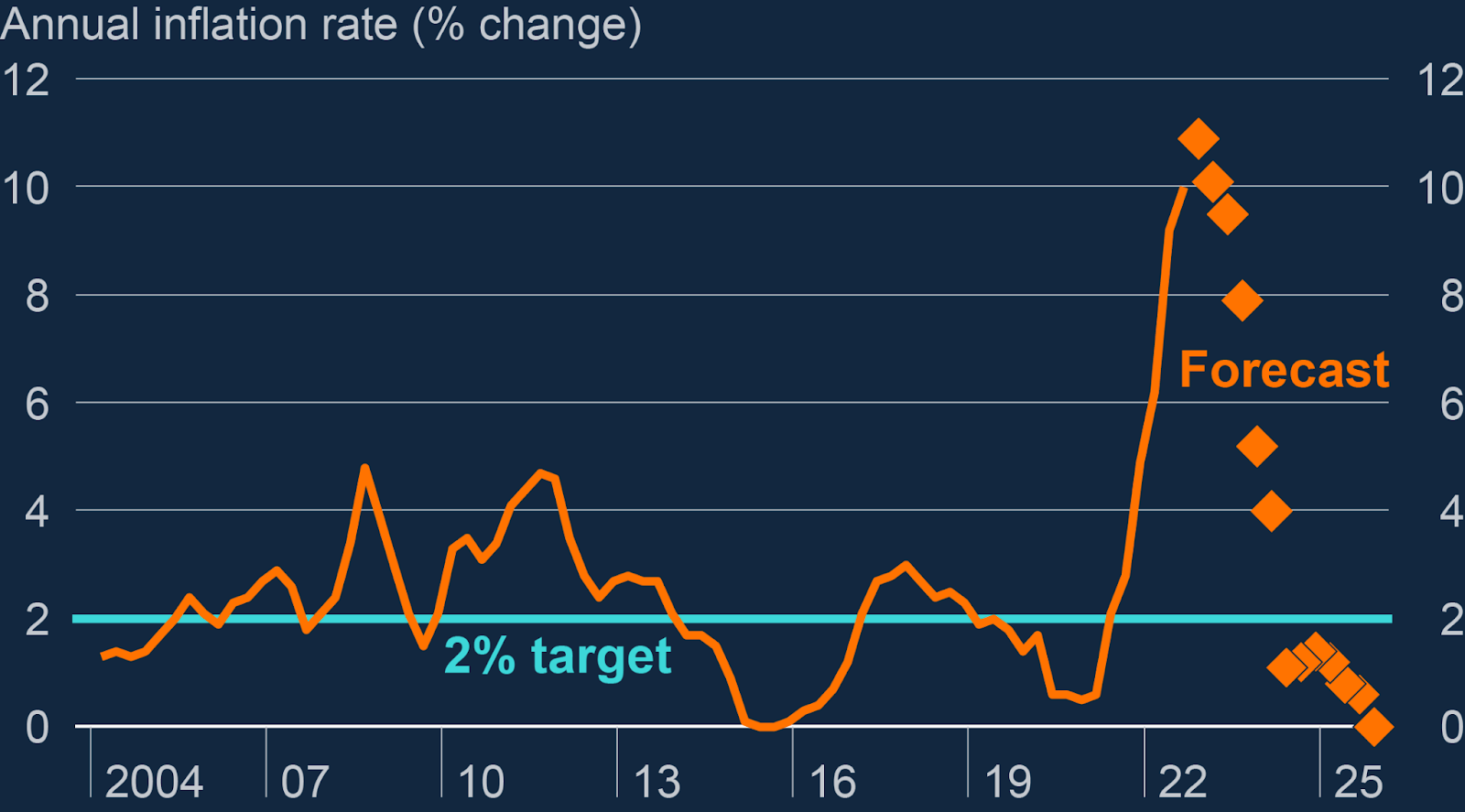

Cast your mind back to June 2021. Markets were flush with cash. Tech stocks reigned supreme as staid assets, such as bonds, barely yielded a penny. On the horizon was a smidgen of inflation. A mild overshoot was a natural homeostasis from the pent-up demand accrued by pandemic savers, spent on cathartic retail therapy. Supply chains couldn’t keep up with the insatiable desire for goods. Labour markets, gripped by “the Great Resignation,” couldn’t hire fast enough. Central Banks dismissed rising prices as a mere fillip. “Inflation is transitory,” was the maxim that rang from St. Louis to Threadneedle Street.

One contrarian warned against the central bank groupthink — Andy Haldane. In June 2021, the departing chief economist at the Bank of England said he expected inflation to be close to 4%, double the BoE’s target, by Christmas. Even he undershot, with the rate reaching 5.4%. That was his parting message, as he left to become Chief Executive of the Royal Society of Arts.

Fast forward to January 2023 and inflation is as entrenched as ever. The UK economy is trapped in a cycle of sclerosis and instability. While Haldane could not have predicted the Ukraine war, unshackled from the BOE monetary committee, he has recently cast an eye on the UK’s structural issues that underpinned his pessimism — and continue to do so. Despite the Bank of England saying inflation will start coming down in the middle of 2023, could they be wrong again? Could inflation be here for longer than central bankers are telling us? Haldane suspects this might the case.

Labour Markets

Many inflationary issues come from labour markets, according to Haldane. The BOE forecast inflation would return to target by the beginning of 2025, as wholesale energy prices, alongside the Government’s support on energy bills, recalibrates consumer prices. Yet agreeing with his predecessor, Huw Pill, Haldane’s replacement, said: “The distinctive context that prevails in the UK – of higher natural gas prices with a tight labour market, adverse labour supply developments and goods market bottlenecks – creates the potential for inflation to prove more persistent.” Regarding the labour supply, Haldane echoed this sentiment in June. “The solution to the growth conundrum and the solution to the cost of living crisis both lie squarely on the supply side of the economy.”

Haldane and his successor are referring to the UK’s shrinking labour force, borne out of an ageing population and government restrictions on blue-collar migration. The UK is almost unique in seeing employment still lower than pre-pandemic levels, with the third worst recovery in the developed world, according to The Institute of Employment Studies. 600,000 more people are “economically inactive” than in 2019. Breaking down these numbers, 200,000 is due to ill health, with 30,000 from Long Covid. Moreover, there are half a million fewer non-UK born workers than there would have been on the pre-2016 trend. This shrinkage represents a feedback loop that ageing populations have on both economic activity and the increasing burden on the healthcare system, Covid notwithstanding.

Spending on healthcare systems in the UK, at least by G7 comparisons, sits towards the bottom of the pack, Haldane chimed.

The question is then, can increased healthcare spending improve workforce participation — and thus reduce inflation? Sunak’s 1.25% National Insurance rise to pay for health spending was reversed by Kwarteng, which was upheld by Sunak as he became PM. Sunak is locked into an industrial relations stalemate with striking nurses, and other public sector workers, on the issue of wages. Sunak’s reluctance to meet this demand is perhaps less out of fear of causing a wage-price spiral, than budget balancing after the market reaction to the borrowing of the Truss’ minibudget. Yet Haldane clearly believes that this is not the time for public spending to be culled. “If the labour supply has gone, we need the productivity engine to fire. The growth arithmetic really is that simple,” he said. This is a reductionist view, although containing some truths.

Productivity Growth

Traditionally, there are four ways to fire productivity growth — capital investment, investment in infrastructure, investment in education, and investing in healthcare. Start with capital investment. Sunak’s tax “superdeduction” has generally failed to spark enough capital investment to replace the labour deficit. Automation is a powerful deflationary force. Yet precision robotics is yet to solve the decline of Britain’s industrial labour force. ChatGPT and other forms of generative AI, however, set an accelerated course to first improve service sector productivity, before causing mass unemployment (perhaps including the author of this article.) This exemplifies the delicate relationship between capital machinery and labour.

Closely intertwined is education. A tight labour market is not just about supply of labour, but rather skills mismatches arising from an unequal, byzantine education system, and a lack of business investment in upskilling. Making maths compulsory until the age of 18, as Sunak wants to do, won’t solve this, although greater focus on digital skills and vocational education might. The unusual combination of high vacancies and low unemployment also indicates a jobs-skills mismatch. Fixing this mismatch would be an important factor in getting inflation under control.

The final piece of the puzzle is investment in infrastructure, which is part of the “Levelling Up” agenda, whose commission Haldane chairs. Rebalancing regional disparities won’t be solved by HS2, which is due for completion between 2029-2033. Investing in deprived, deindustrialised communities can help reduce London-centrism in the economy. Yet the number of new jobs advertising fully remote work has dropped to just 7%, a third lower than at the beginning of this year, a study has found. Remote work is a key driver in the decentralisation of economic activity. Moreover, it is likely that the Levelling Up agenda will be shelved as other priorities take precedence. That being said, ONS statistics show the largest wage rises are happening in areas outside of London, with my home town of Bury in 7th, showing some rebalancing taking place.

Haldane is certainly right about one thing. The key to the UK’s inflation woes beyond energy is in labour. In the public sector, “price” is winning the wage-price spiral, as strikes rage on. In the private sector, services are laying off staff, as agriculture and hospitality struggle to fill vacancies. Only migration, automation, and spending can therefore fight the demographic tide. Perhaps this is why Haldane left the BOE — he sees monetary policy as a blunt tool to solve structural issues in the economy.

Investing in Times of Stagflation

For investors and banks, this complex interaction of factors make it difficult to predict the UK’s trajectory. Such predictions involve policy calculations as much as bets on interest rates. Both political leaders accept the reality that the debt must be reduced, while tacitly accepting that achieving growth while doing that is a difficult task.

Yet the realpolitik on the ground tells a different story. Workers demand more from their government and employers as inflation outpaces wage growth — and will continue to do so. The Bank of England also faces a policy trade off. Raising rates may not bring inflation down, but it will certainly further harm an asymmetrical labour market, in addition to equity and debt markets. Haldane seems to agree. We are seeing developed economies are reaching the limits of economic growth. Perhaps the UK is one of them.

Author: Tal Feingold

#Inflation #UKEconomy #InterestRates #BOE