Currency markets aren’t usually too fond of political instability. One might’ve expected that a fifth election in three years in Israel would elicit some jitters in markets. Yet since the re-election of Benjamin Netanyahu, the New Israeli Shekel (NIS) has risen 4% against the US Dollar. That’s not linked to the election result, despite Netanyahu’s mercurial stewardship of the economy of the “startup nation.” Nor was it connected to the Bank of Israel’s 0.5% base rate rise, bringing rates up to 3.25%.

US inflation data came in lower than expected, with the Federal Reserve indicating some dovishness on the extent of rate rises, allowing most currencies to gain ground on the greenback. To understand the long-run strength of NIS, one must look at the unique economy Netanyahu helped cultivate, and a serendipitous discovery in the brief period he was out of power.

Techno Protectionism

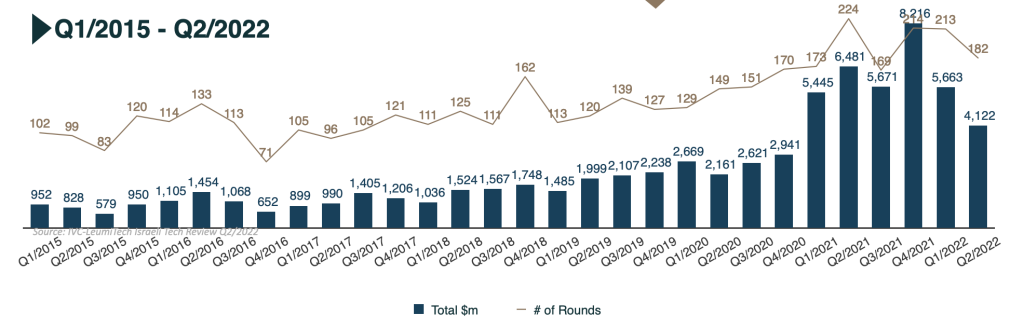

High levels of military spending often leads to an explosion of venture capital and innovation. The ARPA research unit run by the US Government from the 1950s onwards built the foundation for technologies such as the internet and GPS, leading to the eventual establishment of Silicon Valley as a tech hub. So even as Israel’s military spending as a percentage of GDP fell from around 30% in 1972, to just over 6% at the dawn of the millennium, the seeds of technological know-how had moved from the state into commercial cybersecurity. That was just the beginning.

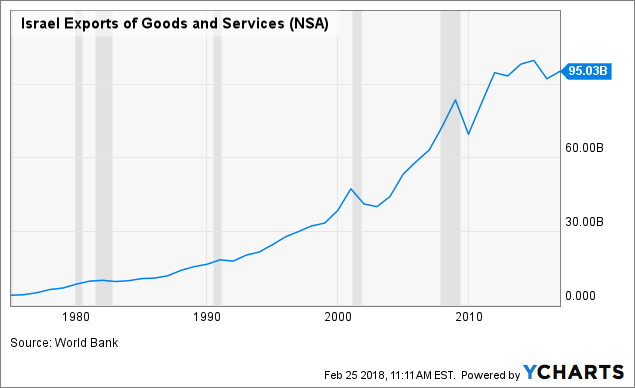

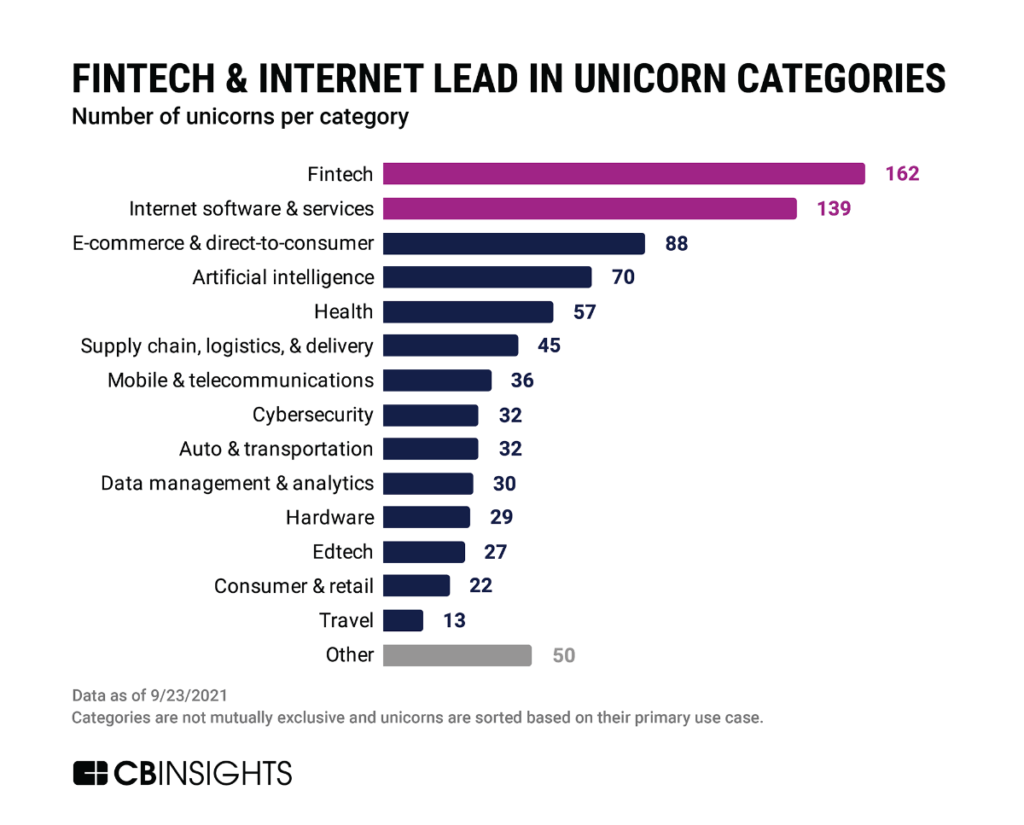

Even as early as the “dotcom bubble,” Israeli life sciences and deeptech businesses were being funded. Throughout the 2000s, Israeli tech funding, and thus exports, increased exponentially. By the time internet penetration had reached a critical mass in the decade after, Israel boasted unicorns from Fintech to AI, with a host of companies listed on the NYSE, NASDAQ, and its own TASE stock exchange. Monday.com, Fivver, Payoneer, and Wix make up some of the most famous names, with 93 companies listed on US exchanges alone.

Tech-driven trade surplus on current account drove the NIS to new heights. Yet newfound wealth so often increases the propensity for consumers to buy imported goods. So perhaps Israel’s economic idiosyncrasy is the juxtaposition of neoliberal tech enablement with protectionist agricultural policy. The OECD criticised Israel’s tariffs on wheat, fats and oils, walnuts, prunes, maize, citrus juices, beef and sheep meat, and various dairy products. With large parts of the agricultural sector undergirded by a network of “Kibbutzim,” former communes that are now mostly privatised, state incentives and tariffs have kept consumer prices high long before inflationary forces swept the rest of the world. But on the demand side, high prices in both real estate and consumer goods are met with inflows of new, affluent Jewish immigrants, with a state incentive to do so. Israel’s unique blend of techno-protectionism is primed for long-term currency growth, driven by inflows and high internal volumes.

Startup Nation faces its toughest test

Israel’s unfettered growth has yet to face a macro test as tough as this, though. Its capital markets had less exposure to the shock of Lehman Brothers, with a short-lived recession “more moderate than in other developed countries,” according to the Bank of Israel. While the pandemic brought tourism to a standstill, global monetary expansion saw a record amount of venture capital deployed into Israel’s tech sector. Still, with significant dry powder to deploy, deal activity remains on the pre-pandemic trendline, though unemployment via restructuring may become a drag on currency growth.

Serendipity

Yet aside from the backdrop of rising rates and valuation corrections, the woes of other economies are being primarily driven by the energy shock of the Ukraine war. The rise in gas prices has been the pivotal driver of supply-side consumer price rises. Yet Israel’s inflation has peaked 5.1%, just under half of the annual rate in the UK, for example. While this could be attributed to a base effect of existing high prices, Israel’s increasing energy independence — and Europe’s newfound need for its own – is keeping energy prices tame.

In June 2022, Egypt, which has liquefaction facilities, received record gas imports from Israel, with a view to exporting to the EU. In October, Israel and Lebanon signed a US-mediated agreement on their long-disputed maritime border last month. The deal stipulated where each country can conduct energy exploration. Israel can also reportedly claim a percentage of Lebanon’s future profits from any gas found in the area. Despite Netanyahu promising to jettison the deal, it is unlikely he will do so. This leaves a strong domestic inflation dampener and another profitable export channel. This will boost the NIS in the medium term, despite its commitment to mitigating — and exposure to – climate change.

Political ramifications

While the political and economic realities of Israel may seem divorced from each other, there are some material impacts of the most right-wing government in Israel’s history. First, the increase in votes for Haredi and Kahanist religious factions has left Aryeh Deri of Shas, and Bezalel Smotrich of Religious Zionism in contention, alongside other veterans from Netanyahu’s Likud party. Each has been scant on policy details, with some rhetoric surrounding reducing taxes and increasing police spending. Indeed, an inflammation of violence is possible with an explosion recently in Jerusalem, but Israel’s GDP expanded at the fastest rate during the Second Intifada (2001-2005).

Currency Markets

Markets do not always reflect the real economy. Hedging by companies and institutional investors adds to speculative forces that determine price. The foreign exchange market is by far the largest market in Israel in terms of turnover, dwarfing the fixed income and equity markets, and has been free of controls for over two decades. Daily turnover in the onshore shekel foreign exchange market is around US$5.5 billion, compared with US$0.3 billion in the equity market and US$0.9 billion in the fixed income market. Given the importance of the USD/NIS market, in terms of both volume and real exports, this can materially make monetary policy harder to manage.

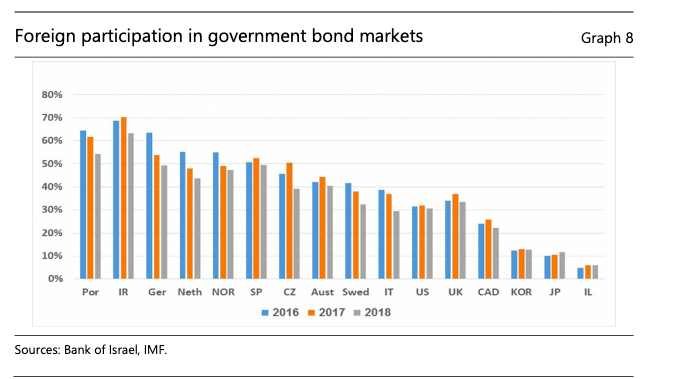

In June 2016, the Bank of Israel enacted a reporting requirement on financial transactions in the shekel foreign exchange and interest rate markets. The information, provided daily by market participants, enhances the Bank of Israel‘s ability to monitor and analyse the behaviour of different market segments. In addition, the foreign investors’ holdings of Government bonds is significantly lower than in other countries, with many preferring real assets.

This visibility and sovereignty mean the “pass-through” from FX markets to the real economy is stronger in goods than services, benefitting the tech sector. This bodes well for financial stability and fiscal sustainability in the future.

Outlook

Israel’s strength cannot be immune to macro currents. Its startups are no longer in the era of cheap money, so revenue growth and funding largesse at generous multiples will be curtailed. Yet the fecundity of startups it is incubating cannot be ignored. The combination of a healthy balance of payments and nascent energy security stand the New Israeli Shekel in good stead to weather the storm. But the adjacent tremors in the housing market, with a reduction in supply and rising rents driving more inflation, it’s possible the Bank of Israel will need to overshoot its target. The question then, is whether central banks will have to halt the export-led steam train propelling the NIS?

Author: Tal Feingold

#Israel #NIS #MiddleEast #BankOfIsrael #TelAviv #Jerusalem