- Comprehensive assessment carried out after banks classified as significant

- Asset quality review and stress test conducted for each bank

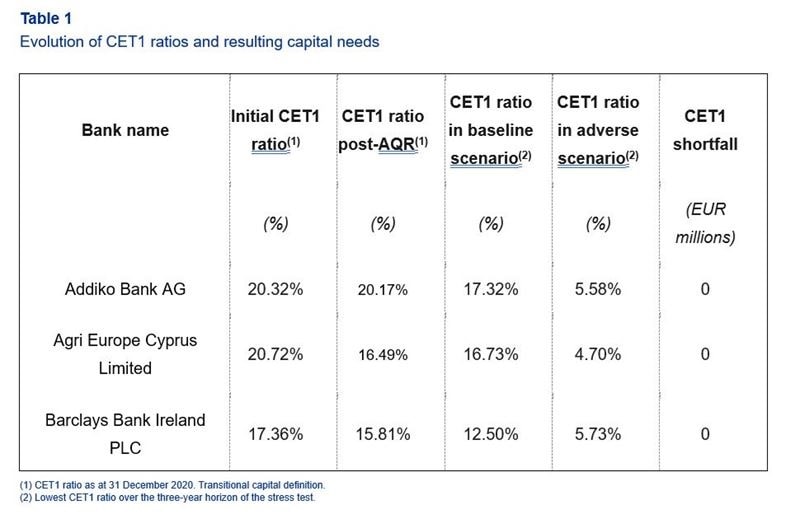

- No capital shortfalls identified after adjustments

The European Central Bank (ECB) has today published the results of its comprehensive assessment of Addiko Bank AG, Agri Europe Cyprus Ltd and Barclays Bank Ireland PLC. The three banks were classified as significant and are therefore supervised by the ECB. As per current practice, all banks that become subject to ECB supervision undergo a comprehensive assessment, which includes an asset quality review (AQR) and a stress test.[1]

The results of the comprehensive assessment show no capital shortfall for Addiko Bank AG or Barclays Bank Ireland PLC, although Agri Europe Cyprus falls below the 5.5% Common Equity Tier 1 capital ratio threshold under the adverse scenario of the stress test, which is a key measure of a bank’s financial soundness. The exercise concludes, however, that Agri Europe Cyprus faces no capital shortfall after adjustments, since its CET1 ratio increased significantly as of 2021, due to the bank’s decision to retain earnings from 2020 to 2021 during the first quarter of 2022. This significantly improved Agri’s capital position as of year-end 2021, which is reflected in the final results of the exercise.

The ECB expects all banks to follow up on the outcome of the exercise and address the shortcomings found in the comprehensive assessment.

The AQR is a prudential rather than an accounting exercise. It provides the ECB with a point-in-time assessment of the carrying values of a bank’s assets on a particular date (31 December 2020 in the case of these three banks). It also determines whether a bank needs to strengthen its capital base. The ECB used the latest version of the AQR methodology to carry out the review.

In addition, the ECB conducted a stress test exercise based on the same methodology and scenarios as the stress tests carried out by the ECB and European Banking Authority in 2021. The stress test looked at how banks’ capital positions would evolve under a baseline and an adverse scenario from end-2020 to end-2023. The adverse scenario included a prolonged economic contraction due to the coronavirus pandemic and a “lower for longer” interest rate environment, which reflects a worsening of economic prospects in a global decline of long-term risk-free rates from an already historically low level.

The threshold ratios applied for identifying capital shortfalls were maintained at the same levels as in previous exercises: a CET1 ratio of 8% for the AQR and the baseline scenario, and a CET1 ratio of 5.5% for the adverse scenario.

All three banks consented to the disclosure of the results.

Detailed results and information on the outcome of this exercise can be found on the ECB’s banking supervision website.

[1] Banks that undergo comprehensive assessments as of 2022 will only be subject to an AQR and be considered for inclusion in the regular EBA/SSM stress tests or SSM supervisory stress tests.