Armenia borrows from two of the world’s largest multilateral lenders at noticeably different rates for the same sovereign credit. Understanding why the International Monetary Fund (IMF) and World Bank price their loans differently, and why Armenia’s blended borrowing cost remains lower, offers useful insight into multilateral lending.

IMF credit currently carries a basic rate of roughly 3.4 percent. New US dollar loans from the World Bank’s market-rate arm, the International Bank for Reconstruction and Development (IBRD), currently price between 4.6 and 5.3 percent depending on maturity. Neither figure is an error, nor does it signal any change in how creditors view Armenia. The two institutions simply use different pricing methodologies. This difference, along with Armenia’s lower blended portfolio cost, offers a clear view into how multilateral credit is priced.

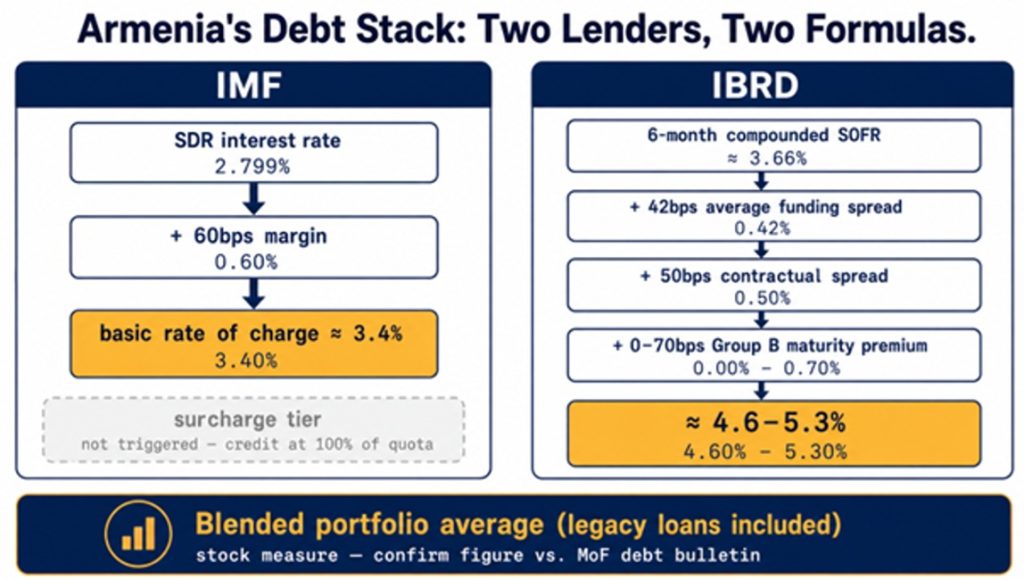

The IMF’s Pricing Formula: SDR Basket Rate Plus 60 Basis Points

IMF lending from its General Resources Account is priced off the SDR interest rate. The SDR, Special Drawing Right, is the Fund’s composite unit of account, valued against a basket of five currencies: the US dollar, euro, Chinese renminbi, Japanese yen and British pound sterling. Every week the IMF recalculates that rate as a weighted average of three-month government instrument yields across the five basket currencies, subject to a floor of 0.05 percent. For the week of 6 – 12 July 2026, the SDR interest rate stood at roughly 2.815 percent.

On top sits a fixed margin of 60 basis points. The IMF’s Executive Board cut that margin from 100 basis points in a reform package effective November 2024, part of a set of changes the Fund said would lower members’ borrowing costs by about $1.2 billion a year while continuing to “provide incentives for prudent and temporary borrowing.” Add the margin to the SDR rate and Armenia’s basic rate of charge lands at approximately 3.4 percent.

Precautionary Facility: Armenia’s $175 Million IMF Arrangement

Two caveats sharpen this lending picture. First, heavy borrowers pay more: level-based surcharges of 200 basis points apply only to credit above 300 percent of a member’s quota, with a 75-basis-point time-based surcharge for prolonged use. Armenia is nowhere near either trigger. Its current arrangement, a three-year SDR 128.8 million (about $180 million) Stand-By Arrangement approved in December 2025, equals exactly 100 percent of quota.

Second, Yerevan is not actually drawing the money. The IMF’s board completed the first review in June 2026, bringing available access to about $50 million. Yet the authorities continue to treat the arrangement as precautionary: an insurance line maintained for a modest commitment fee, not a loan being serviced at 3.4 percent.

World Bank IBRD Pricing: SOFR Plus Spreads Up to 162 Basis Points

IBRD lending uses a completely different pricing structure. For US dollar loans, the base rate is SOFR, the Secured Overnight Financing Rate that replaced LIBOR. The New York Fed publishes SOFR daily based on Treasury repurchase agreements. As of early July 2026, overnight SOFR was around 3.53 percent. The World Bank compounds this rate over six-month periods.

On top of SOFR, the Bank adds a spread designed to pass through its own funding costs to borrowers. This spread consists of three components: an average funding spread (currently 42 basis points for dollar loans), a fixed contractual lending spread of 50 basis points, and a maturity premium that increases with loan duration. Armenia falls into Pricing Group B. For this group, total spreads currently range from 92 basis points for shorter loans to 162 basis points for loans with 18 to 20-year maturities.

As a result, a new US dollar IBRD loan to Armenia typically prices between 4.6 percent and 5.3 percent, before a 0.25 percent front-end fee and a 0.25 percent commitment fee on undisbursed amounts.

This lending pipeline is already active. The Bank’s board approved a $200 million Economic Transformation Development Policy Operation for Armenia in March 2026, with the OPEC Fund adding parallel financing to bring the package near $290 million, and the five-year Country Partnership Framework endorsed in January 2025 envisages around $1 billion of IBRD financing. “We support the country’s efforts to build a more open, competitive, and sustainable economy,” said Fabrizio Zarcone, the World Bank’s country manager for Armenia.

Why Armenia’s Blended Borrowing Cost Is Lower Than Both Headline Rates

Both rates represent marginal costs, or the price of the next dollar borrowed. Armenia’s outstanding external loan book tells a third story, because it is a stock: the weighted average of every loan still on the books, including credits contracted years ago on concessional or near-concessional terms, when global reference rates sat far lower. Estimates prepared for this piece put that blended average across Armenia’s external multilateral borrowing at approximately 3.2 percent, below the IMF’s fresh-lending rate and well below new IBRD pricing. The direction, if not yet the decimal, is officially confirmed: Finance Minister Vahe Hovhannisyan told parliament in June 2026 that the weighted average interest rate on government loans “decreased by 0.3 percentage points” in 2025. For contrast, dram-denominated government bonds placed in 2025 carried a 9.2 percent average yield, nearly triple the cost of Armenia’s multilateral money.

The mechanics matter more than the decimal. A blended average is backward-looking; marginal rates are forward-looking. As older, cheaper loans amortise and are refinanced with SOFR-linked IBRD credit, the portfolio average will drift toward the marginal price, even if Armenia’s creditworthiness never moves. Conflating the two measures is one of the most common errors in sovereign-debt commentary, and Armenia’s numbers show why: the same country is simultaneously a sub-3.5 percent borrower on its stock and a 5 percent borrower at the margin.

What Armenia’s 47.2 Percent Debt Ratio Enables and What the Spread Signals Next

Armenia enters this repricing cycle from a position of relative strength. Central government debt stood at 47.2 percent of GDP in 2025, the economy grew 7.2 percent that year, and the finance ministry has set a target of pushing the debt ratio below 45 percent. All while the IMF projects growth near 5.3 percent for 2026. Cheap legacy funding is part of what makes that arithmetic work: every point of interest saved on the external stack is fiscal space the budget does not have to find.

For institutional readers, the takeaway travels well beyond Yerevan. The SDR-plus-margin and SOFR-plus-spread formulas apply uniformly across borrowers; only the vintage mix of each country’s portfolio is unique. A sovereign can look cheap on its blended average and expensive at the margin at the same time, and the gap between those two numbers is, in effect, a countdown.

For Armenia this countdown is comfortable, but it is running. Each legacy loan that matures is replaced by new borrowing at higher rates. That convergence, not either headline rate on its own, is the number sovereign-risk desks should watch.

Author: Richardson Chinonyerem

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organisations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

IMF Staff Concludes Visit to Georgia | Disruption Banking

Is The International Monetary Fund (IMF) Losing Credibility? | Disruption Banking