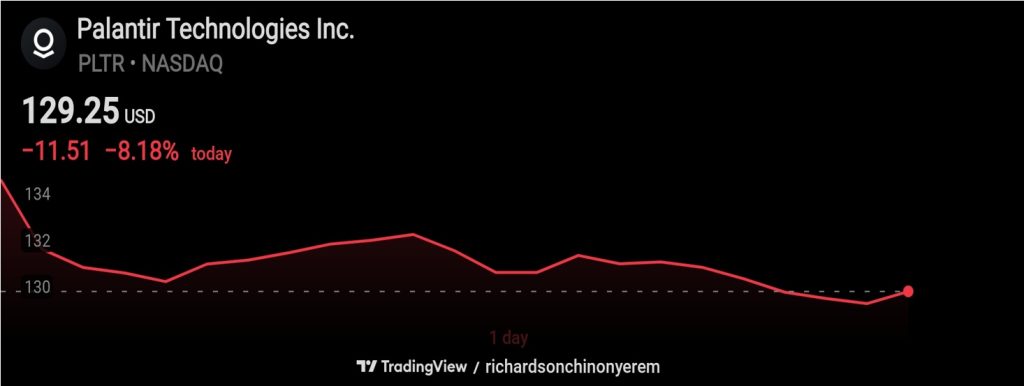

Palantir Technologies (NASDAQ: PLTR) is having a terrifying April 9. While the broader tech sector clawed back gains, PLTR fell more than 8% (TradingView) at the time of writing, hitting $129.25 per share. The stock is now down over 28% year-to-date (YTD) and approximately 38% below its 52-week high of roughly $207 set in November 2025.

Market analysts point to two catalysts driving today’s sell-off: a renewed attack from “Big Short” investor Michael Burry, and a product launch from Anthropic that strikes at Palantir’s commercial heartland.

For context, this is not new territory. DisruptionBanking saw this risk early. In December 2023, we asked whether Palantir’s AI hype was outrunning reality. Then, earlier this year, we noted the stock had already dropped from nearly $170 to around $135 over the prior month despite strong growth. That earlier skepticism now looks justified.

Palantir’s story has remained impressive. Its share price had simply become too dependent on perfection

Burry Renews Criticism — Citing Anthropic’s Rapid ARR Growth

On Wednesday, April 8, Burry took to X to declare that Anthropic is “eating Palantir’s lunch.” While the X post in question seems to have been taken down, Burry cited Ramp data showing Anthropic’s annual recurring revenue (ARR) surged from $9 billion to $30 billion, capturing roughly 73% of all incremental enterprise AI spending, per a report.

His argument was that Palantir is stuck doing “low-margin and small” government work, while Anthropic is offering businesses an easier, cheaper, and more intuitive path to AI.

Burry’s fund, Scion Asset Management, disclosed a short position in PLTR last year. Since his initial warnings in late 2025, the stock is down 26%. His timing, so far, looks prescient.

Anthropic’s New Managed Agents Platform Directly Challenges Palantir AIP

On April 8, Anthropic launched Claude Managed Agents, a cloud platform letting enterprises build and deploy AI agents without touching infrastructure.

Early adopters include Notion, Rakuten, Asana, and Sentry. Pricing starts at $0.08 per session hour, and Anthropic claims it cuts agent deployment time from months to days. That is a direct challenge to Palantir’s Artificial Intelligence Platform (AIP), which has been the company’s primary commercial growth engine since 2023.

Anthropic is now targeting the same enterprise buyer, faster, cheaper, and without a stretched valuation to protect.

Palantir Still Trades at 109x Forward Earnings Despite the Pullback

Even after recent pullbacks, Palantir trades at roughly 109 times forward earnings, against a sector median near 21 times, according to Motley Fool. The trailing price-to-earnings ratio sits around 200.

The bull case is not without substance: Palantir reported Q4 2025 revenue of $1.41 billion, up 70% year-on-year (YoY), marking ten straight quarters of accelerating growth. It closed 180 deals in Q4 alone, and Mizuho reaffirmed an Outperform rating citing strong enterprise demand.

One analyst projects a $225 price target by early 2027, implying 50% upside. But that math only works if revenue growth stays elevated. In 2026, the comparisons get much harder.

UK Political Pressure Mounts on Palantir’s NHS Contract

On top of valuation pressure, Palantir faces a political storm in Britain. Its £330 million NHS Federated Data Platform contract is under threat, with British MPs urging ministers to explore a break clause available in early 2027. NHS staff are boycotting the platform outright.

The British Medical Association has called on doctors to limit engagement. Amnesty International is running an active campaign to remove the company from NHS infrastructure.

With over £670 million in total UK public sector contracts at stake, this is a structural risk to Palantir’s international revenue base.

What’s Next for PLTR?

The defense side of the Palantir story remains intact. The Pentagon classified Maven AI as a Program of Record on March 9, 2026, guaranteeing long-term budgetary support. Palantir holds $7.2 billion in cash and carries no debt.

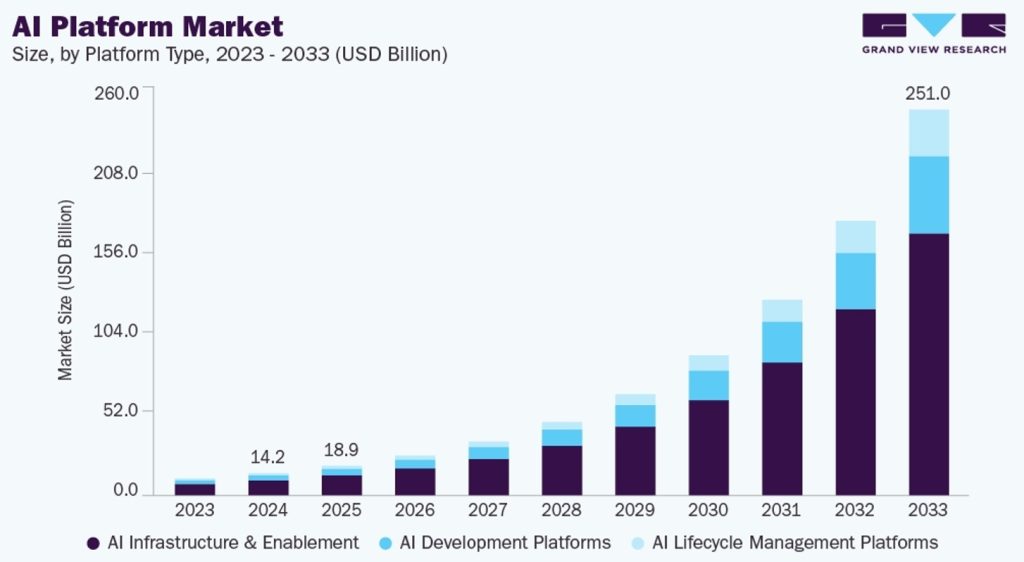

Grand View Research projects the AI platform market to grow 38% annually, reaching $251 billion by 2033. In classified and sovereign AI, Anthropic cannot easily follow.

But in commercial enterprise AI, the market that drove PLTR’s stock up 1,000% since 2023, Anthropic just raised the competitive stakes significantly. Burry’s short thesis has always been about valuation and disruption risk. Today, both hit at once.

At 109 times forward earnings, Palantir can’t afford to lose the enterprise race. Right now, that race just got a lot tighter.

Author: Richardson Chinonyerem

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organizations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

Why Chevron (CVX) Collapsed More Than 6% Today | Disruption Banking

Is Palantir Too Big To Fail? | Disruption Banking

Palantir: Is The AI Hype Outpacing Reality? | Disruption Banking