The last week of Trans-Atlantic relations unfolded like a fiscal quarter, complete with threats, reversals, and sudden relief rallies. Europe and the U.S. actually prepared for war, and it’s not an overstatement to say that the once vaunted North Atlantic Treaty Alliance (NATO) will never be the same. $1.2 trillion was wiped away from the S&P alone, and as usual when his policies adversely impact his billionaire friends, Trump chickened out, proving correct the wisdom of the TACO (Trump Always Chickens Out) trade.

A Lesson in The Roy Kohn School

Hopefully, Europe will take away a lesson from this week: soft power, i.e. diplomacy, dialogue, and reasoning, means nothing to this White House. MAGA sneers at rational argument and the idea of mutually beneficial relations, preferring White House Deputy Chief of Staff for Policy Stephen Miller’s strategy of brute force.

Trump’s strategy, taught to him by his mentor Roy Kohn, is, in a nutshell, hit back ten times harder, never back down, and never admit defeat. The implications of this frightening episode seem to have taken root in Europe.

An anonymous European official who attended Trump’s meandering speech at the World Economic Forum told Politico, “The takeaway for Europe is that standing up to him can work. There is relief, of course, that he’s taking military force off the table, but there is also an awareness that he could reverse himself. Trump’s promises and statements are unreliable but his scorn for Europe is consistent. We will have to continue to show resolve and more independence because we can no longer cling to this illusion that America is still what we thought it was.”

Speak Softly and Carry A Big Bazooka

Top intellectuals and strategists in America were already pleading for Europe to activate the “trade bazooka” and impose costs on Trump and his allies, no matter the damage to European interests, but among Europeans, there was much hand-wringing and indecision.

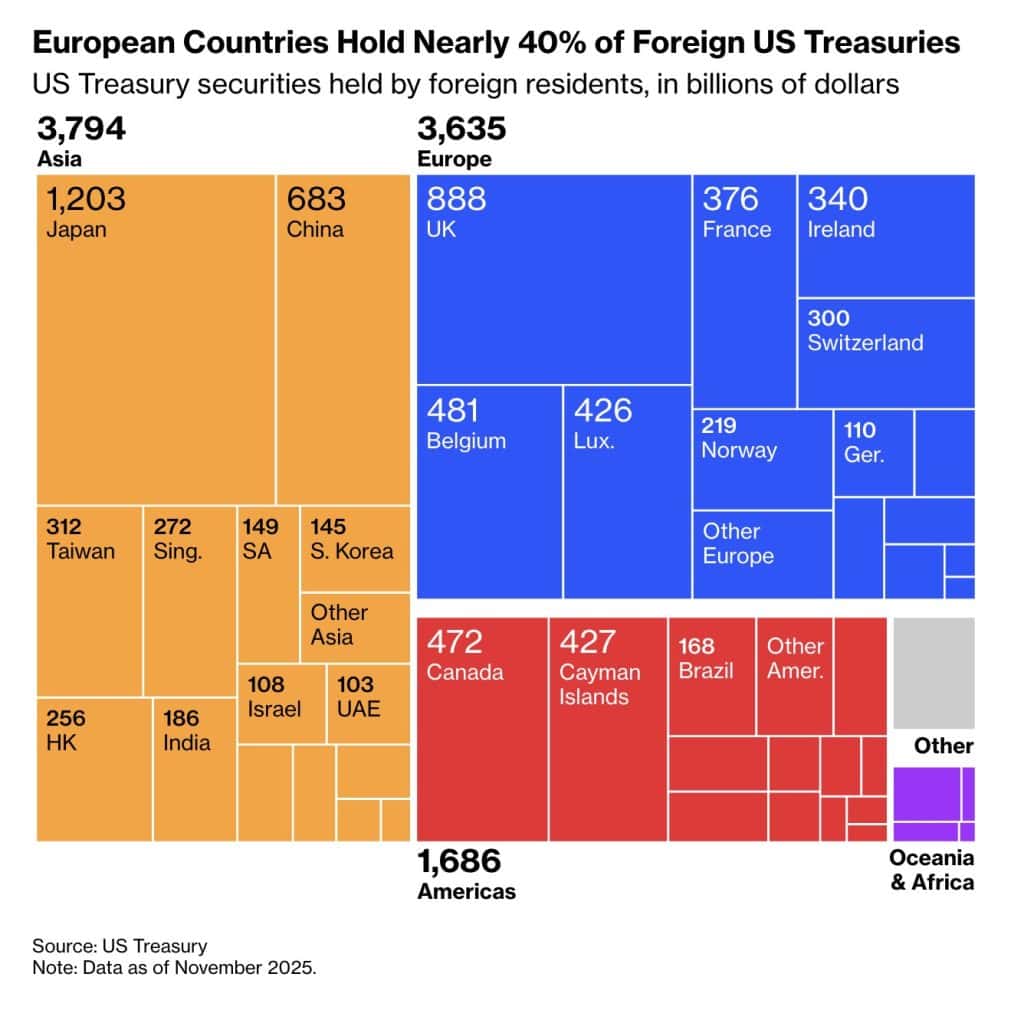

On Monday, January 19, the Financial Times cast doubt on whether European governments could leverage the $12.6 trillion pile of U.S. assets, including $8 trillion of U.S. Treasuries and equities, to compel the American President to back down from his latest tariff threat against America’s European allies and his stated intentions to gain control of Greenland, a member of NATO.

The very next day, a Danish pension fund dumped $100 million in U.S. treasuries, suggesting private holders of US debt may not need much prodding.

In Davos, Ursula von der Leyen, President of the European Commission, stated that the result of employing the trade bazooka would amount to, “Plunging us into a dangerous downward spiral would only aid the very adversaries we are both so committed to keeping out of our strategic landscape.”

The unnamed adversaries would seem to mean Russia and China, which potentially misreads the actual state of affairs when it comes to Trump who has done little to counter Putin’s goals and sent out American soldiers to kneel disgracefully on the tarmac, rolling out a red carpet for the Russian despot.

However, von der Leyen was correct that for Europe, retaliation against the U.S. would carry heavy costs. Not only would effective retaliation require large, coordinated, and persistent divestment of American assets across multiple sovereign states, it would require central banks to harm and destabilize their own reserves. Pension and insurance regulators would be obliged to take on intentional losses.

Complicating matters, the losses to the U.S. would likely be temporary as U.S. banks, pensions, insurance companies, and crypto firms would buy up the assets while losses to Europe would be permanent. It would be like a standoff with the U.S. holding a gun and Europeans holding a knife.

Unfortunately, Trump and his advisers know this asymmetry in market power only too well. He promised “big retaliation” if Europeans sell U.S. assets, saying, “We have all the cards.”

However, that doesn’t seem to have stopped more EU pension funds from liquidating their holdings of T-bills. Sweden’s largest pension fund dropped $8 billion in U.S. bonds. The Dutch pension fund ABPS has sold $10 billion over the past six months, one third of its holdings.

Treasury Secretary Downplays Concerns

On Wednesday, speaking from the World Economic Forum, U.S. Treasury Secretary Scott Bessent dismissed concerns that the announced sale of T-bills, saying Denmark and its investments were “irrelevant,” adding, “I’m not concerned at all.”

AkademikerPension, the Danish pension operator, has justified the sale due to “poor government finances,” a sort of tongue-in-cheek Scandinavian burn. The fund’s investment director, Anders Schelde, didn’t ignore the geopolitical rift, adding in a written statement, “Thus, it is not directly related to the ongoing rift between the U.S. and Europe, but of course that didn’t make it more difficult to take the decision.”

Bessent pointed to Denmark’s decreasing holdings of T-bills in past years, saying, “They’ve been selling Treasuries. They have for years.”

In the last five years, the Danish government has indeed reduced its exposure to U.S. government debt from $18 billion to just under $10 billion.

Bessent attributed the market chatter to one single analyst at Deutsche Bank AG, George Saravelos, the global head of FX, and blamed the “fake news media” for blowing the situation out of proportion.

Saravelos wrote, “In an environment where the geoeconomic stability of the Western Alliance is being disrupted existentially, it is not clear why Europeans would be as willing to play this part. Developments over the last few days have potential to further encourage dollar rebalancing.”

Bessent assured his audience that, “The CEO of Deutsche Bank called to say that Deutsche Bank does not stand by that analyst’s report.”

Regardless, the FT noted, “Saravelos is far from the only one to make this argument, and the instinct is understandable.”

The Globalist Elite Gathering

At the World Economic Forum, European leaders are reportedly seeking to cool tensions in NATO. In Davos, Trump ruled out using force to annex Greenland, referring to it as “Iceland” several times, although he repeatedly stated that future U.S. control of Greenland/Iceland was nonnegotiable.

The American President insisted that “Canada should be grateful,” with implied threats to the Canadian Prime Minister Mark Carney who received a standing ovation yesterday with his speech declaring that the previous global order was “not coming back.”

Regardless, markets fell on Tuesday, along with the dollar. The Trump administration’s defacto crisis manager, Bessent attributed the fall to a bond selloff in Japan. Then, on Wednesday, the European Parliament suspended approval of a key U.S. trade deal.

Bernd Lange, chair of the European Parliament’s International Trade Committee, said it was “left with no alternative but to suspend work on the two Turnberry legislative proposals until the US decides to re-engage on a path of cooperation rather than confrontation, and before any further steps are taken.”

Nevertheless, markets seemed pleased that Trump committed (for what it’s worth) to acquiring Greenland without kinetic actions, and the Dow Jones, the S&P 500, and the Nasdaq all rose by ~1% on Wednesday. Bessent, again, had an alternative explanation, again connected to Japan, saying, “I’ve been in touch with my economic counterparts in Japan and I am sure that they will begin saying the things that will calm the market down.”

Play It Again, European Leaders: Appeasement

Sounding more like a mafia capo than a treasury secretary, Bessent warned the Europeans, “sit back, take a deep breath, do not retaliate, do not retaliate.” Mostly the heads of state have fallen in line, with the exception of the French President Emmanuel Macron, who suggested the bloc “should not be hesitant” to employ the much-touted “trade bazooka.”

Macron seemed to play a different tune in texts directly with Trump, which Trump leaked ostensibly to emphasize the French President’s chummy / groveling tone, contrasting with his public bluster.

After Trump’s hour-long harangue against NATO, European leaders, and various other enemies, he sat down with Mark Rutte for under an hour and afterward Trump pulled a 180 turn. Even more bizarre, Trump undermined his own full-throated rationale for ownership of Greenland, which was so urgent and unequivocal but then suddenly abandoned.

Trump TACO

Dave Keating, the Brussels correspondent for France24, explained, “Trump has majorly chickened out here. Trump has backed away from these tariffs, and he’s trying to sell this to his supporters as having reached a new deal with new concessions, but the fact of the matter is there really are no substantive concessions that Mark Rutte could have given him. There were no Danish government representatives there at that meeting as far as we know, so what may have happened here is that Mark Rutte explained to Trump the existing rights that the U.S. has in Greenland under its treaty with Denmark which is basically to deploy an unlimited number of troops and establish an unlimited number of bases. These are the rights that the US has always had. That is the argument that Denmark and others have been stressing to Trump and his officials over the past weeks. It may be that Mar, Rutte sold this to Trump as something new or Trump understands that it’s not new, but he’s going to try to sell it to his supporters as something new, so that it looks like he didn’t chickened out here.”

Trump’s supporters generally accept whatever Trump does, so that shouldn’t be a problem. On his personal social network, Trump proclaimed the “framework of a future deal with respect to Greenland and, in fact, the entire Arctic Region,” to much ado, although it was unclear whether the deal expanded beyond Greenland or if Trump was merely waxing grandiloquent to sell this as something new.

Anders Vistisen, a Danish member of the European Parliament, told CBC News Network, that Trump “could not deliver on why he should have Greenland and what he needs it for… All that’s left is false rhetoric and basically a lot of lies about the Arctic area and Greenland.”

Learn from The Chinese

This will happen again. Trump will grandstand and bully and attempt to intimidate America’s NATO allies. Europe might take a page from China’s strategy to inflict the maximum pain on Trump’s base, which was echoed by Canada to great effect. China quietly discontinued its purchase of U.S. soy, choosing to buy from Brazil and Trump was forced to put together a $12 billion bailout for thousands of starving farmers loudly bemoaned their (predictable) plight on social media, sending shockwaves through MAGA-land.

Canada stopped buying whiskey made in Appalachia and at least 5 major producers went bankrupt in 2025 alone, closing distilleries. The economic pain imposed on the MAGA faithful carries real political consequences, compounded by their bewilderment when Trump did not step in to rescue them until it was too late.

The lesson for Europe is not that retaliation is impossible, but that blunt instruments wielded without asymmetry are self-defeating. Trump will repeat this cycle, provocation, intimidation, retreat dressed up as victory, and Europe’s choice is whether to respond with symbolic outrage or with targeted, quiet pressure that hits political constituencies rather than balance sheets. The markets may have shrugged this episode off, but the strategic damage to trust, alliance cohesion, and the illusion of shared values is real, cumulative, and unlikely to reverse.

Author: Tim Tolka, Senior Reporter

#Crypto #Blockchain #DigitalAssets #DeFi

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organizations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

Trump’s Powell Investigation Backfires Fast

Trump Wants Venezuela’s Oil. The Problem Is It May Cost $110 Billion Just to Start