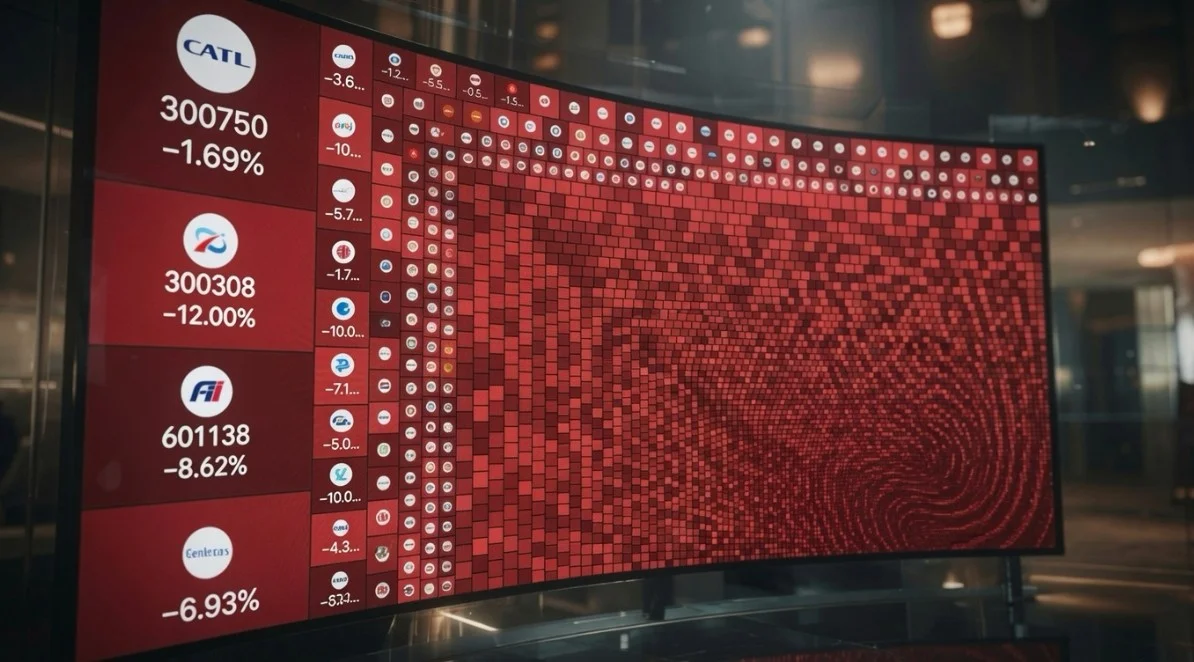

The dramatic red heatmap told the story in vivid color. Dozens of Chinese stocks plunged into deep losses, with many names showing declines of 5 percent to 12 percent or more in a single session. On July 17, trader Ted Pillows highlighted the scale with a stark figure of 4.3 trillion yuan in market value erased, capturing a moment of genuine shock across social media and trading platforms.

This type of viral post is not new. Just days earlier on July 10, a nearly identical red heatmap spread rapidly with claims of 2.3 trillion yuan wiped out in roughly two hours. The Disruption Banking analysis at the time provided important context. While the selling pressure was real and concentrated in technology, semiconductor, and high growth sectors, the headline trillion-yuan figures exaggerated the actual market wide impact.

The Broader Asian Tech Sell-Off on July 17

The pressure on Chinese equities occurred amid a wider regional tech correction. South Korea’s KOSPI tumbled more than 6 percent, with SK Hynix dropping over 11 percent. Japan’s Nikkei fell around 3.4 percent, and Taiwan’s TAIEX declined over 3 percent. Heavyweight chipmakers and semiconductor supply chain names led the declines across the region.

In mainland China, the Shanghai Composite fell around 3 percent while the Shenzhen Component dropped more than 5 percent. Both saw meaningful drops, though the Hang Seng in Hong Kong was relatively more resilient with little net change. Overall, MSCI Asia Pacific tech gauges faced broad pressure.

What Is Really Happening Beneath the Headlines

Several factors are contributing to the renewed weakness in Asian tech stocks.

Valuation and profit taking concerns stand out after explosive gains fueled by AI infrastructure demand. Investors are questioning whether lofty valuations can be sustained. Strong earnings have sometimes been met with sell the news reactions.

Capacity and spending jitters are also playing a role. Reports of potential overcapacity in AI computing, rising chip costs, and massive new capital expenditure plans have raised questions about near-term pricing power and returns on capital.

Broader sentiment has amplified the moves. US semiconductor weakness, analyst commentary, and macroeconomic crosscurrents including interest rate expectations have added to the volatility in Asia’s chip heavy indices.

Implications and Outlook

This marks a notable reversal for markets like South Korea, where the KOSPI had been one of the year’s top performers thanks to memory chip demand for AI servers. Similar dynamics have played out in Taiwan and Japan, key links in the global semiconductor supply chain.

For investors, the moves highlight the sector’s heightened sensitivity to sentiment shifts. While long term AI fundamentals remain robust for many companies, near term volatility could impact IPO pipelines, M&A activity, and lending exposure to high-growth tech firms. Foreign investor flows, already showing rotation out of crowded AI winners, will be closely watched.

Analysts caution that this may represent a healthy correction rather than the end of the AI cycle. Volatility is likely to persist as markets digest earnings, capex plans, and demand signals.

The red screens are impossible to ignore in the moment. But as the earlier Disruption Banking piece illustrated, separating the dramatic visuals from the full market picture is essential for a balanced view. See also the latest analysis on the regional tech sell off here: Is the AI Boom Over for KOSPI and Asian Tech Stocks?

Author: Andy Samu