Ten years ago, a Gulf bank acquiring a tier two international financial institution might have sounded like a pipe dream of one of its Sheikhs. Buying a football club is one thing, buying a structurally important bank with a presence in emerging markets only trumped by HSBC is another. Yet, First Abu Dhabi Bank (FAB) announced that it had explored acquiring London-based lender Standard Chartered, before cancelling the deal due to regulatory hurdles.

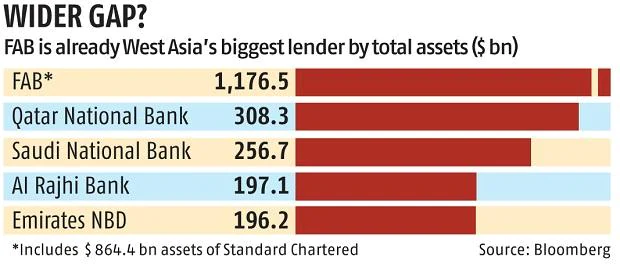

This move comes at a time when FAB is bolstering its investment banking division amid a commodity boom that has compounded the wealth of the Abu Dhabi Sovereign Wealth Fund, which owns 50% of the bank. FAB has amassed about $312 billion in assets at the end of September — that compares with Standard Chartered’s $864 billion. The commodities run has emboldened regional rivals Qatar and Saudi Arabia too. No longer content with domestic lending, each state is now looking to exercise its global ambitions in the banking arena too.

Broad Horizons

Start with the United Arab Emirates. The botched Standard Chartered deal shows its strength — and also the limits of its incursions into Western finance. Its external presence has yet to spread far and wide, despite its market cap of $51.9 billion. About 75% of FAB’s revenue comes from the UAE, although the bank has a presence in 19 countries outside of its home market, according to a November investor presentation. Standard Chartered is worth $24.75 billion, so any acquisition would have had to come out of the Emirati Royal Family’s estimated $300 billion personal wealth, or a consortium of other strategic investors.

While finances contributed to the collapse of the deal, the regulatory challenges were a larger factor. Standard Chartered is classified as a Global Systemically Important Bank — unlike FAB — and therefore the Abu Dhabi lender would’ve needed to go through a particularly rigorous approval process, including seeking the green light from multiple regulators, to push a deal over the line. Still, the ambition reflects a desire to go beyond the Middle East. Last year, it withdrew a billion-dollar bid for investment bank EFG-Hermes after facing lengthy regulatory delays in Egypt. Transparency and compliance are barriers that may be insurmountable, but the ambition and deep pockets of the UAE will eventually find it a palatable acquisition target.

Qatar’s Messi approach

The biggest banking casualty of rising interest rates is Credit Suisse. The Swiss lender took on excessive risk in the Greensill and Archegos scandals, with some analysts sighting struggles in the credit default swaps on its balance sheet. That hasn’t stopped the Qatar Investment Authority and the Saudi National Bank from loading up as the embattled bank spins off its investment banking unit. After the share sales, SNB, QIA and Olayan, a wealthy Saudi family, will own between 20 and 25 per cent of Credit Suisse stock. Still, there doesn’t look to be a drive for a full acquisition — SNB is keeping its stake in the bank at less than 10 per cent to avoid complications with the Swiss regulator, according to people with knowledge of the plans.

Yet it remains to be seen why the two nations would increase their stake in a failing lender for anything other than strategic reasons. Like Abu Dhabi, the state national banks are partly funded and controlled by the sovereign wealth funds, but there doesn’t seem to be much desire for a banking acquisition. That’s because Qatar gobbled up Societe Generale’s Egyptian business for $2 billion in 2013, and a 23.5 per cent stake in pan-African lender Ecobank International in 2014, while snagging Turkey’s Finansbank in 2016. Yet while UAE and Qatar maintain a rivalry, the Credit Suisse deal and a recent Ronaldo vs Messi showcase in Dohar indicate a detente between Saudi Arabia and Qatar, as they seek to embed their influence beyond the Middle East.

Life after Oil

One thing is clear: while the Gulf has been buoyed by its natural resources, it knows it cannot rest on its laurels. Oil will be phased out within the next 20 years, depending on the trajectory that you believe in; gas may last longer, particularly in emerging markets where LNG can be an alternative to coal. The Gulf knows the green transition is both inevitable and potentially lucrative. The likes of Aramco are betting on clean energy accordingly.

Alongside this sits the other two pillars of the Gulf’s “life after oil” strategy: sport and banking. Sport is starting to be more than “sportswashing” vanity projects too. Manchester City, for example, acquired by Abu Dhabi in 2008, has reached £613 million annual revenue in 2022, and a profit of £41.7 million, up from £ 2.4 million in the previous year. The Saudi Royal family may follow a similar path with Newcastle performing well too.

Still, it seems that banking is the greatest prize. For sovereign wealth funds, becoming LPs in funds and deals helps generates returns; buying banks wields influence. This is not without challenges. We don’t know if the global financial systems will acquiesce to a Gulf-owned major bank, but we should expect to see ever more ambitious acquisition targets over the coming years.

Author: Tal Feingold

#UAE #Gulf #Dubai #AbuDhabi #SaudiArabia #Qatar #FAB